FX: 🇨🇳🇯🇵🇺🇸 Cross Asset Tie-Ins (thread)

Meltdowns in #SPX #NASDAQ $LUNA $UST #BTC & some commods (metals)

&

Buying in 🇺🇸Treasuries (“USTs” from here forward, not ref to Luna $UST) & JPY, as 🇺🇸CPI again↑

👆Each of above have their own story- but just to show charts on CNY JPY👇

Meltdowns in #SPX #NASDAQ $LUNA $UST #BTC & some commods (metals)

&

Buying in 🇺🇸Treasuries (“USTs” from here forward, not ref to Luna $UST) & JPY, as 🇺🇸CPI again↑

👆Each of above have their own story- but just to show charts on CNY JPY👇

1/

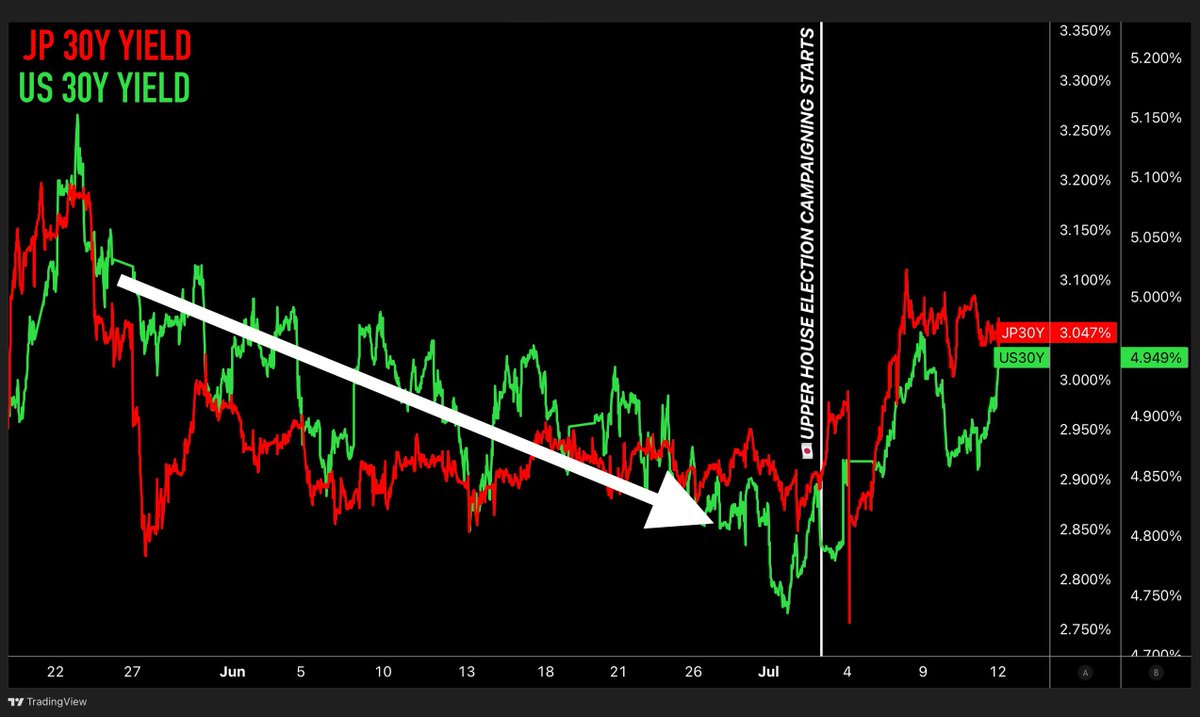

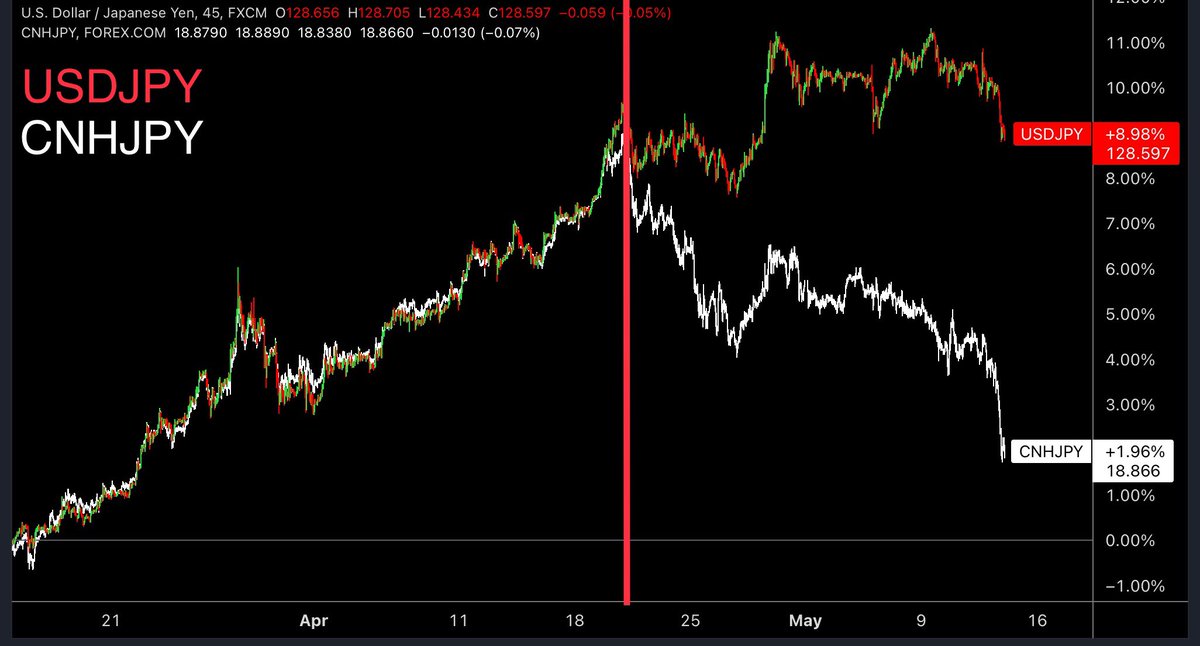

First just note April 20th (marked as red line on charts below). This date/event was the last time 🇯🇵JGBs were (perceived by some to be) “freely” traded- as in, no pre announce by BOJ to cap yields

Post 4/20 BOJ cap yields “forever”

& this is when things changed cross asset👇

First just note April 20th (marked as red line on charts below). This date/event was the last time 🇯🇵JGBs were (perceived by some to be) “freely” traded- as in, no pre announce by BOJ to cap yields

Post 4/20 BOJ cap yields “forever”

& this is when things changed cross asset👇

https://twitter.com/acrossthespread/status/1516674025128611841

2/

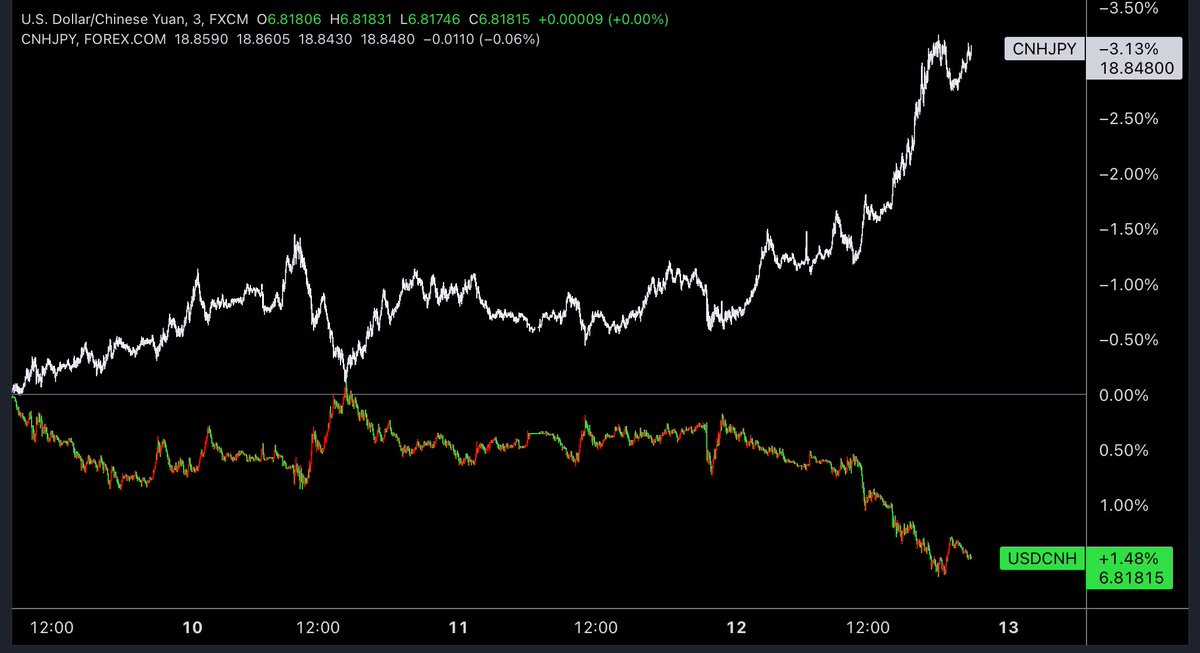

By removing day to day “will/won’t they” uncertainty BOJ (knowingly/not) shifted relentless & historic 🇯🇵¥ selling → 🇨🇳yuan selling

& yuan selling since 4/20 has been alarmingly sudden & sharp, w/ global cross asset market impact

By removing day to day “will/won’t they” uncertainty BOJ (knowingly/not) shifted relentless & historic 🇯🇵¥ selling → 🇨🇳yuan selling

& yuan selling since 4/20 has been alarmingly sudden & sharp, w/ global cross asset market impact

3/Stocks

See 3 charts👇 #NASDAQ futures vs USDCNH (inverse, so “USDCNH ↓” = yuan ↓)

NDX sell off started long before any CNY stability disrupt, so NDX / risk asset selling happens for various reasons simultaneous & interchangeable

Since 4/20 its been yuan led, near tick-tick

See 3 charts👇 #NASDAQ futures vs USDCNH (inverse, so “USDCNH ↓” = yuan ↓)

NDX sell off started long before any CNY stability disrupt, so NDX / risk asset selling happens for various reasons simultaneous & interchangeable

Since 4/20 its been yuan led, near tick-tick

4/ Crypto

Luna UST story is wild & incredibly significant in itself. & yes idiosyncratic flows occurring.

But a -$40bn vanish doesn’t happen in vacuum, I don’t care what asset it is, it has impact/being impacted

Just to point again to 🇨🇳yuan

BTCUSD & CNHJPY👇(only 1 bottoming)

Luna UST story is wild & incredibly significant in itself. & yes idiosyncratic flows occurring.

But a -$40bn vanish doesn’t happen in vacuum, I don’t care what asset it is, it has impact/being impacted

Just to point again to 🇨🇳yuan

BTCUSD & CNHJPY👇(only 1 bottoming)

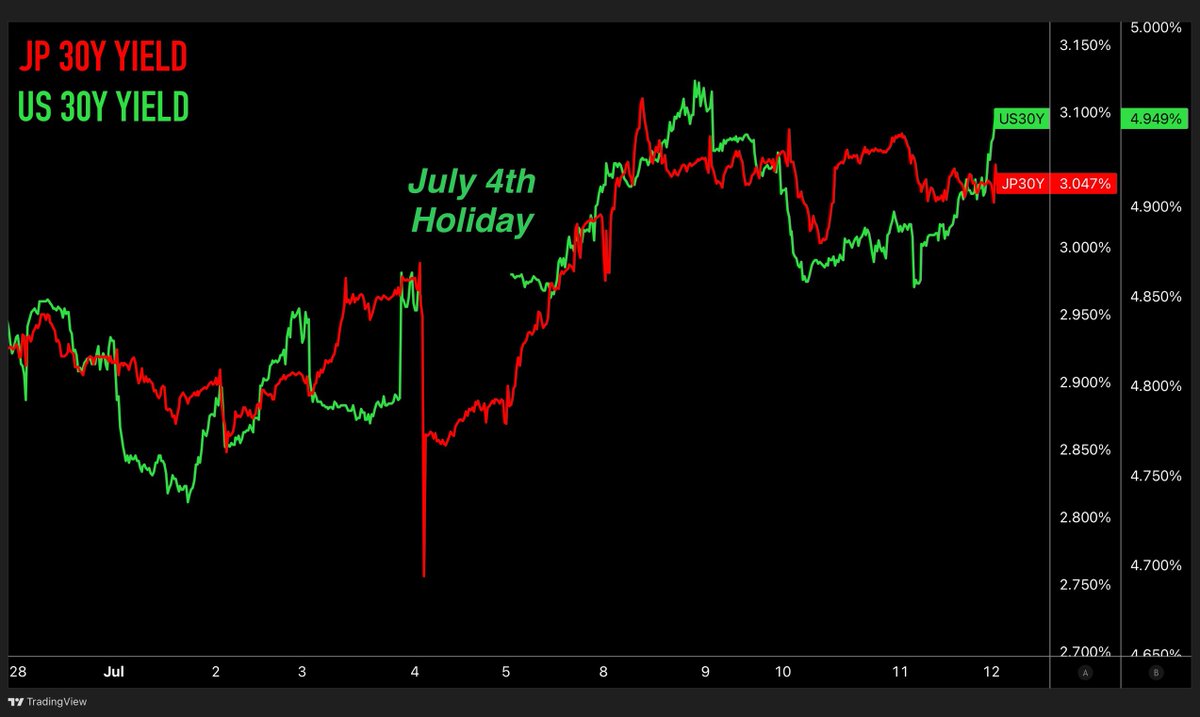

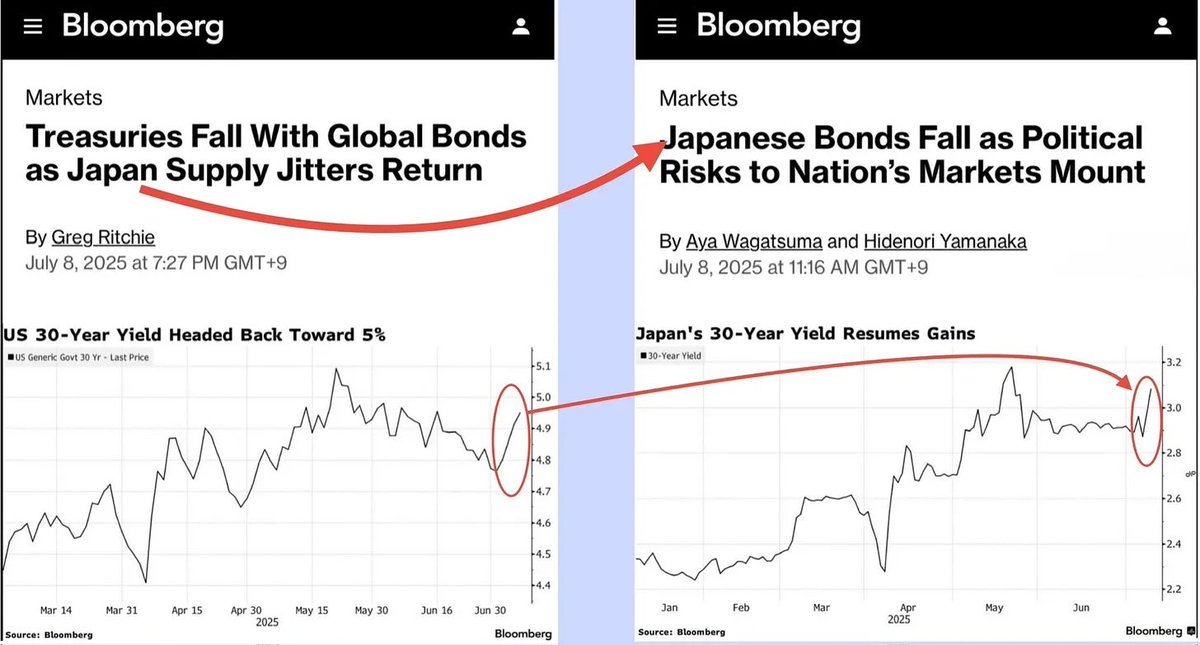

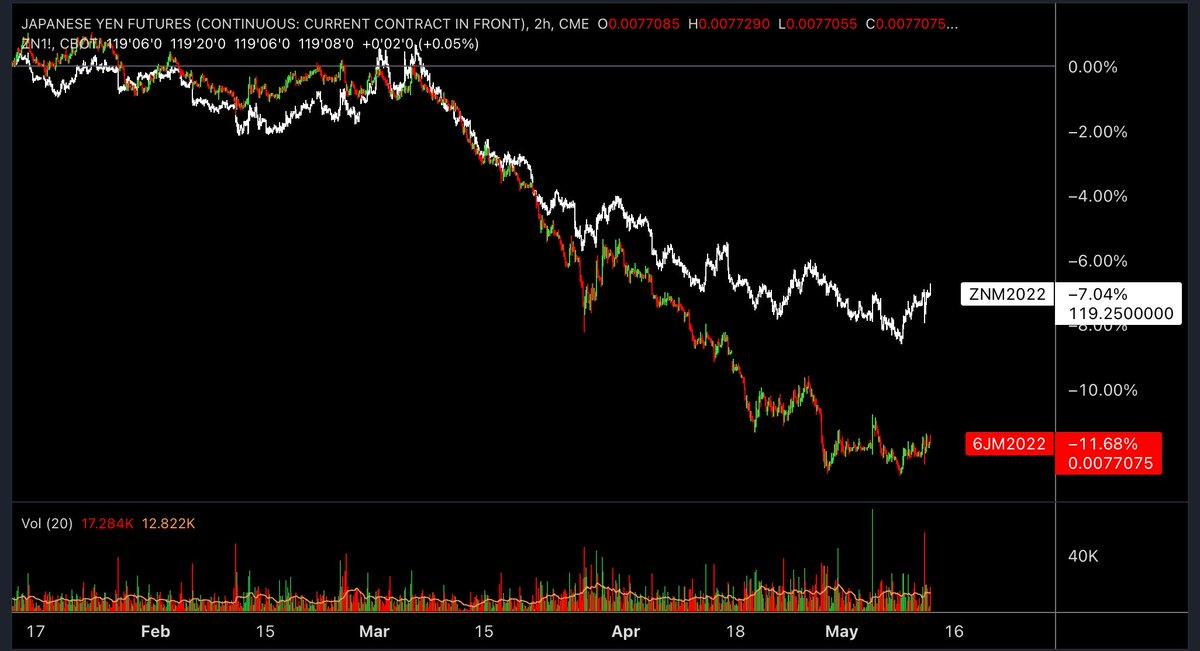

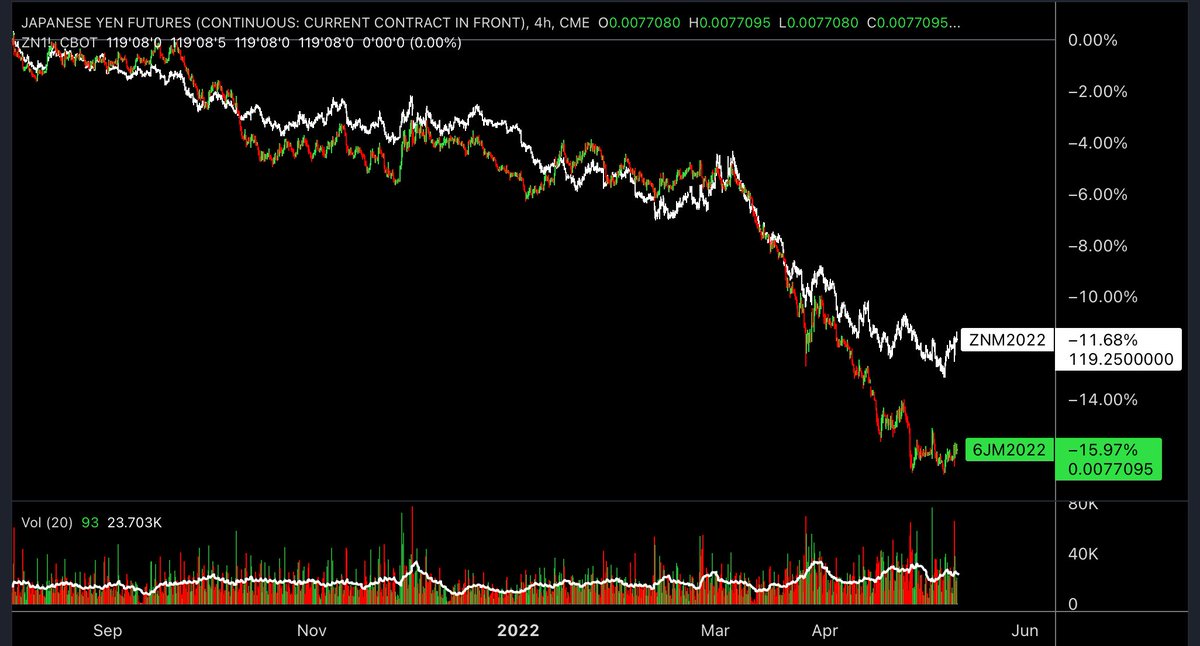

5/ 🇺🇸Treasuries

10Y UST yields & USDJPY (UST & yen futures) have been directionally lockstep, & still are intraday (chart 3: 🇺🇸CPI release👇)

But since 4/20, USTs ~bottomed while ¥ hadn’t (yet), & USTs & ¥ began diverge

As per my “straddle” trade:

UST calls & JPY puts

10Y UST yields & USDJPY (UST & yen futures) have been directionally lockstep, & still are intraday (chart 3: 🇺🇸CPI release👇)

But since 4/20, USTs ~bottomed while ¥ hadn’t (yet), & USTs & ¥ began diverge

As per my “straddle” trade:

UST calls & JPY puts

6/ Treasuries cont

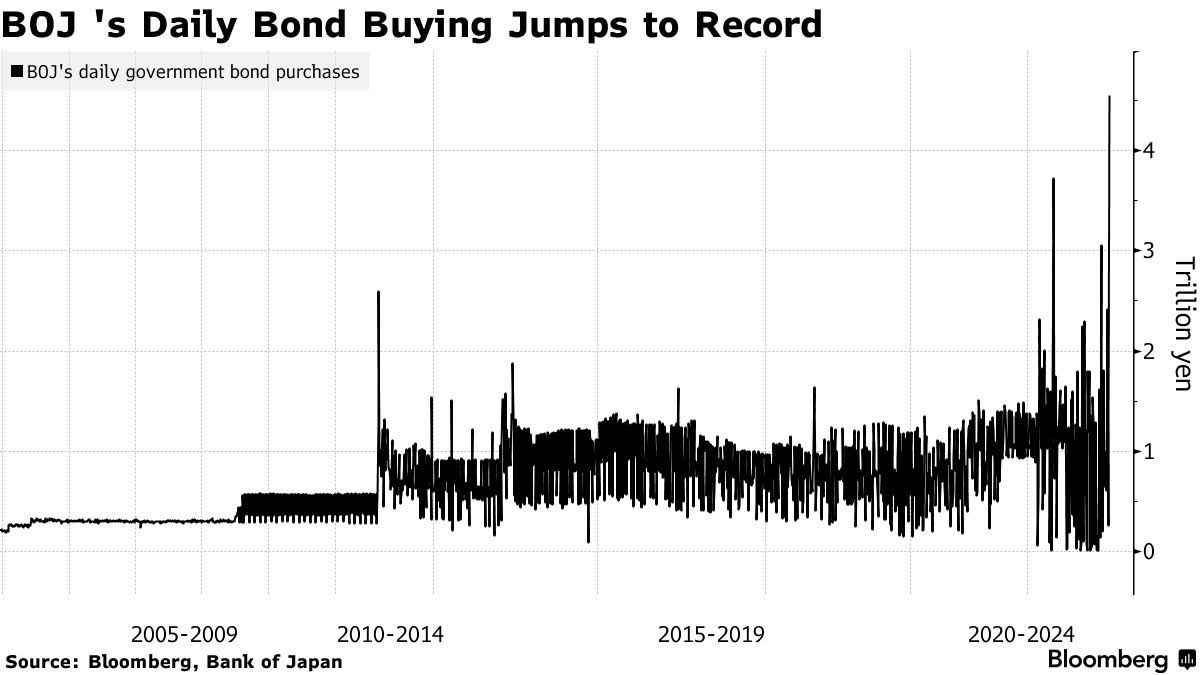

Lot of talk of 🇯🇵 FX hedging costs ↑ is preventing 🇯🇵 from buying USTs

As I’ve been saying- yes prob for some, but def not all (🇯🇵 investor ≠ monolith). 🇯🇵 buying USTs unhedged happens (hence straddle trade)

YTD: if long 10y UST from 🇯🇵 ❌hedge, PnL = flat

Lot of talk of 🇯🇵 FX hedging costs ↑ is preventing 🇯🇵 from buying USTs

As I’ve been saying- yes prob for some, but def not all (🇯🇵 investor ≠ monolith). 🇯🇵 buying USTs unhedged happens (hence straddle trade)

YTD: if long 10y UST from 🇯🇵 ❌hedge, PnL = flat

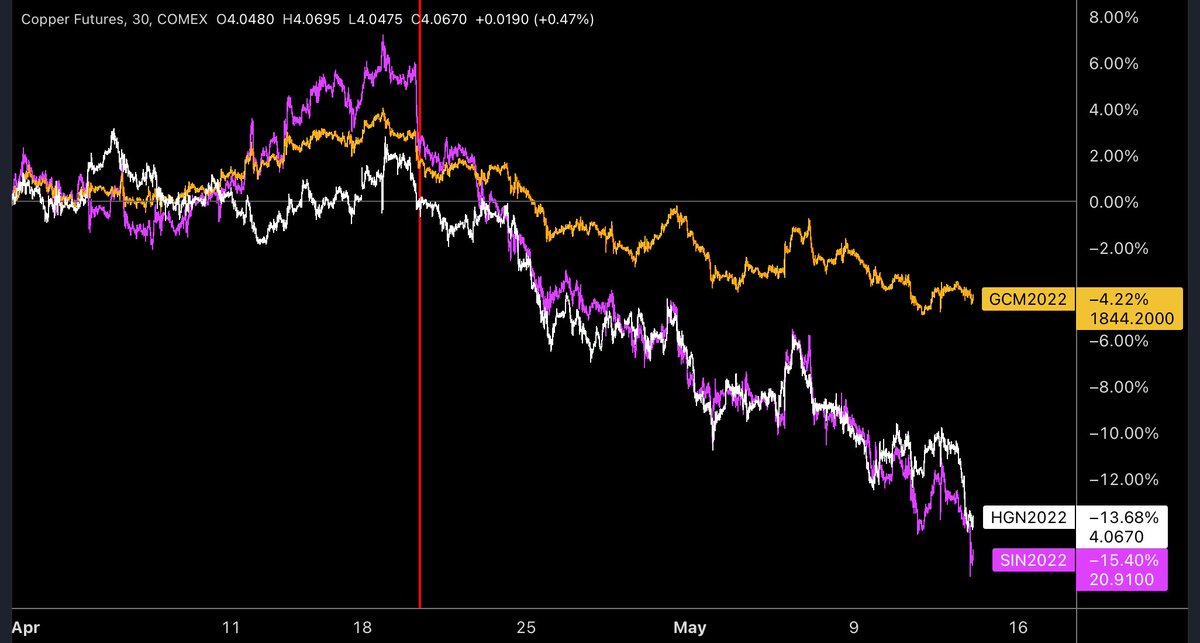

7/ Commods (metals)

Gold, silver, copper (& others) sold off from same starting point: 4/20👇

Cooper especially has been getting slammed as yuan getting killed

Just closed out long puts on HG copper futures as approaching $4 level ← “short yuan” play

Gold, silver, copper (& others) sold off from same starting point: 4/20👇

Cooper especially has been getting slammed as yuan getting killed

Just closed out long puts on HG copper futures as approaching $4 level ← “short yuan” play

https://twitter.com/acrossthespread/status/1523575728218185731?s=21&t=yToMmXW-SZDiRysUZ9z8_w

8/

Crypto comm, stock investors, bond traders, commod specs/producers- each have own very real & legitimate thing happening. Not trying to diminish anyone’s very real issues

But when emotionally invested everything seems to revolve around your thing

Just don’t miss big pic too👇

Crypto comm, stock investors, bond traders, commod specs/producers- each have own very real & legitimate thing happening. Not trying to diminish anyone’s very real issues

But when emotionally invested everything seems to revolve around your thing

Just don’t miss big pic too👇

How timely (& frankly not useful sorry to say)

https://twitter.com/Quicktake/status/1521234748676485120

• • •

Missing some Tweet in this thread? You can try to

force a refresh