1/ $MSTR has amassed exactly $2B loss (net of fees and interests, mark-to-market) on its $4B #BTC "investment" (see below). That's 50% loss per my math.

No, $MSTRQ doesn't have a long-term time horizon

No, $MSTRQ doesn't have a long-term time horizon

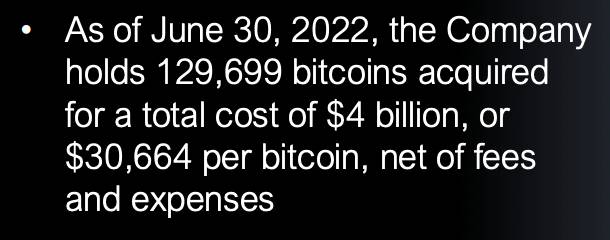

2/ On slide #13, $MSTR says they've bought ~130k #BTC for $4B or $30,664/BTC.

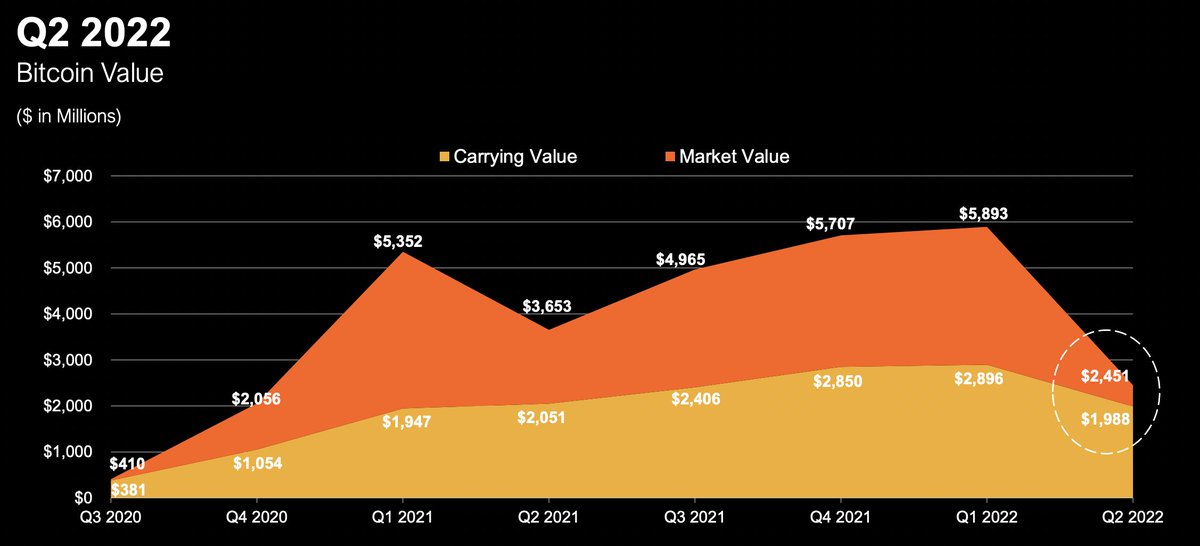

On slide #19, they say the carrying value is $1.988B ($15.327/BTC) and market value is $2.451B ($18.897/BTC) for a $2B loss.

On slide #19, they say the carrying value is $1.988B ($15.327/BTC) and market value is $2.451B ($18.897/BTC) for a $2B loss.

3/ The underlying biz just breaks even.

Shareholders are already underwater, in other words, they are buying negative equity for their good dollars. #BTC needs to appreciate just so that their "investment" will be worth zero.

Shareholders are already underwater, in other words, they are buying negative equity for their good dollars. #BTC needs to appreciate just so that their "investment" will be worth zero.

4/ It's like teaching kids negative numbers: if there are a negative 187 million people on the bus, how many people have to hop on so that no one would be on that bus?

(apologies, not mark-to-market but as per 6/30)

Why own $MSTR instead of buying #BTC directly and enjoying every single % of appreciation (if any)?

Under ~$21.5k/BTC $MSTR won't be able to service its debt (when due). If #BTC drops 15%, $MSTR is BK while w/ direct #BTC you'd still have 85%.

Under ~$21.5k/BTC $MSTR won't be able to service its debt (when due). If #BTC drops 15%, $MSTR is BK while w/ direct #BTC you'd still have 85%.

https://twitter.com/ChrisBloomstran/status/1555013739317022720?s=20&t=4NpLw2MLR26Zaoln7U48yA

• • •

Missing some Tweet in this thread? You can try to

force a refresh