The wait is over! 🎉

Before moving on to code ARCH models...👨💻

I will share the notebook in #Python for ARIMA models! 📓

🚨 Check the end of the thread, there's a present! 🎁

#TimeSeries #DataScience #MachineLearning

Before moving on to code ARCH models...👨💻

I will share the notebook in #Python for ARIMA models! 📓

🚨 Check the end of the thread, there's a present! 🎁

#TimeSeries #DataScience #MachineLearning

First, the steps covered:

1️⃣ Import data (in this case Google stock price) 📚

2️⃣ Format data 🔨

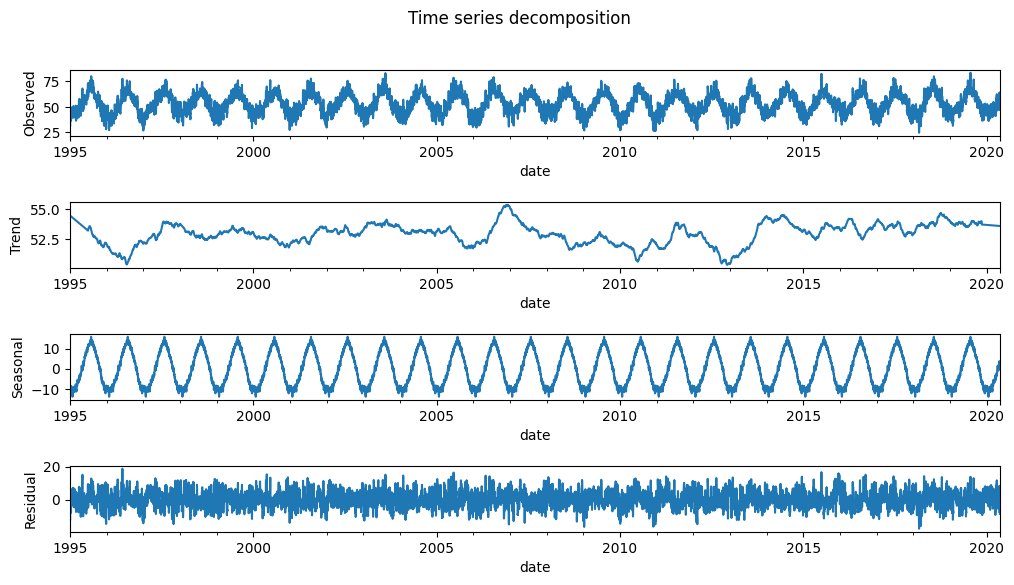

3️⃣ Visualise prices and returns 🔍

4️⃣ Estimate parameters p, d and q 🔬

1️⃣ Import data (in this case Google stock price) 📚

2️⃣ Format data 🔨

3️⃣ Visualise prices and returns 🔍

4️⃣ Estimate parameters p, d and q 🔬

5️⃣ Build the initial model 🛠️

6️⃣ Find the optimal model 🌟

7️⃣ Forecast! 🔮

6️⃣ Find the optimal model 🌟

7️⃣ Forecast! 🔮

Here it is! The notebook in #Kaggle so you can build your ARIMA model! 📓

👇👇👇

kaggle.com/code/davidandr…

👇👇👇

kaggle.com/code/davidandr…

There is a SECOND NOTEBOOK for ARIMA, this time for the auto-ARIMA model.

🚨 Do this:

• 🔔Follow me

• 💬comment

• 🔁retweet

and I will send it to you!! 🚨

🚨 Do this:

• 🔔Follow me

• 💬comment

• 🔁retweet

and I will send it to you!! 🚨

• • •

Missing some Tweet in this thread? You can try to

force a refresh