How #FATCA IGAs relate to legislation in IRC: To be consistent with FATCA law and avoid the 30% US sanction, IGAs must require the FFIs to close the account of "US Persons" who fail to supply required data (without regard to local #GDPR law). Solutions? law.cornell.edu/uscode/text/26…

US #FATCA can accommodate Europe's #GDPR only by by excluding @USCitizenAbroad with @TaxResidency abroad from the definition of "U.S. Person". These two screen shots illustrate the problem ... Some thoughts on how this might this be achieved. law.cornell.edu/uscode/text/26…

As the @DemsAbroadTax statement and @SEATNow_org states/implies this problem can be solved ONLY if the US joins the world in adopting residence as the criterion for @TaxResidency. Citizenship would no longer be relevant for taxation. NOT part of any current legislative proposal.

A second solution would be “A Regulatory Fix For Citizenship Taxation” Which would define “individual” as resident. As published by @TaxNotes

here … taxnotes.com/featured-analy…

here … taxnotes.com/featured-analy…

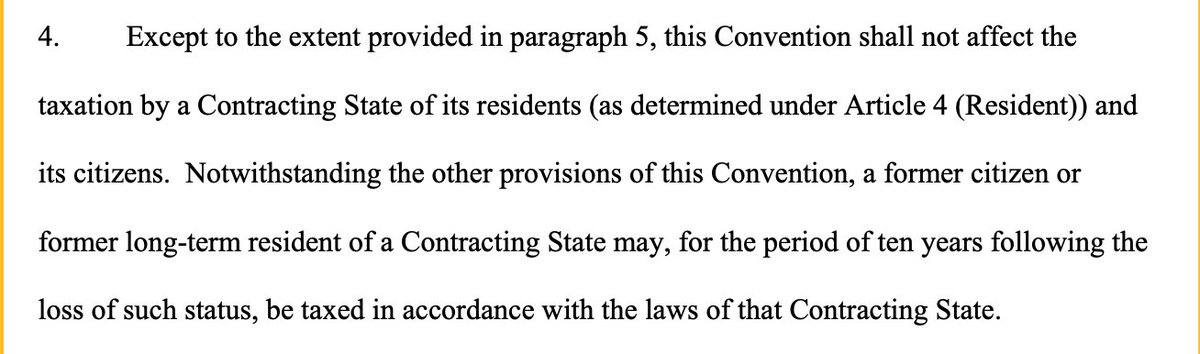

Third solution would be to either (1) suspend the tax treaty #savingclause which would allow #Americansabroad to become treaty nonresidents in an #FBAR and #FATCA world or (2) make an election for @USCitizenAbroad to become treaty nonresident an exception to the "saving clause"

Note par 178 of the Belgium decision. The transference of #FATCA data to the USA based on and only on citizenship/nationality violates the #GDPR. There is no way to reconcile the Belgium and US law. Should the US or Belgium decide what happens in Belgium? drive.google.com/file/d/1bZo-pN…

• • •

Missing some Tweet in this thread? You can try to

force a refresh