Charles W. Eliot University Professor and President Emeritus at Harvard. Secretary of the Treasury for President Clinton and Director of NEC for President Obama

Apr 17, 2025 • 4 tweets • 1 min read

Any self-respecting Treasury Secretary would resign rather have the Department be complicit in the weaponization of the IRS against a political adversary of the President. Harvard will endure and it is far, far from perfect, but if this directive is not withdrawn, the Administration will have taken another substantial step away from the rule of law and democracy.

.@SecScottBessent is derelict with respect to what may be his most important duty—maintaining law-based rights respecting our tax collection system. DOGE violating privacy rules, evisceration of enforcement capacity, politicization of leadership and now political intrusion into a specific taxpayer’s status.

Apr 9, 2025 • 4 tweets • 1 min read

Developments in the last 24 hours suggest we may be headed for serious financial crisis wholly induced by US government tariff policy.

Long-term interest rates are gapping up, even as the stock market moves sharply downwards. This highly unusual pattern suggests a generalized aversion to US assets in global financial markets. We are being treated by global financial markets like a problematic emerging market.

Mar 22, 2025 • 4 tweets • 1 min read

I am profoundly saddened and alarmed by @Columbia University and @PaulWeissLLP law firm's capitulation to the increasingly dictatorial Trump administration.

I cannot judge, because I do not have many of the relevant facts, the wisdom or necessity of the steps taken.

But this kind of bending of the knee by major institutions, if continued, threatens American democracy.

Mar 4, 2025 • 8 tweets • 2 min read

Harvard continues its failure to effectively address antisemitism.

Despite President Garber’s clear and strong personal moral commitment, he has lacked the will and/or leverage to effect the necessary large scale change, and the Corporation has been ineffectual.

Harvard’s CMES, where Harvard task force head Derek Penslar has remained a faculty affiliate, hosted a panel on “Israel’s war on Lebanon” that very likely was antisemitic, according to the IHRA definition the University recently adopted under legal duress.

Feb 2, 2025 • 4 tweets • 1 min read

.@realDonaldTrump's tariffs are a bully strategy. Bullying doesn’t win over time on the playground or in the international arena. This self-inflicted supply shock is a strategic gift to Xi Jinping. 1/4

Just when inflation is sensitive, it will risk price increases for oil, food, and cars and may lead the @federalreserve needing to raise interest rates. 2/4

Feb 1, 2025 • 8 tweets • 2 min read

Aside from the general issues about Trump‘s tariff and his economic nationalism strategy, today’s actions against Canada and Mexico are inexplicable and dangerous. 1/8

First, the tariffs will raise prices on automobiles, gasoline, and all kinds of things that people buy. 2/8

Apr 1, 2024 • 7 tweets • 2 min read

I was very disappointed that the Harvard Law Student Government endorsed divesting in Israel. This following on what the Harvard Graduate Student Union did some time ago illustrates that there is a pervasive prejudice problem on the Harvard campus.

I continue to believe that BDS advocacy, if heeded, would represent anti-semitism in effect, if not intent.

Feb 27, 2024 • 9 tweets • 3 min read

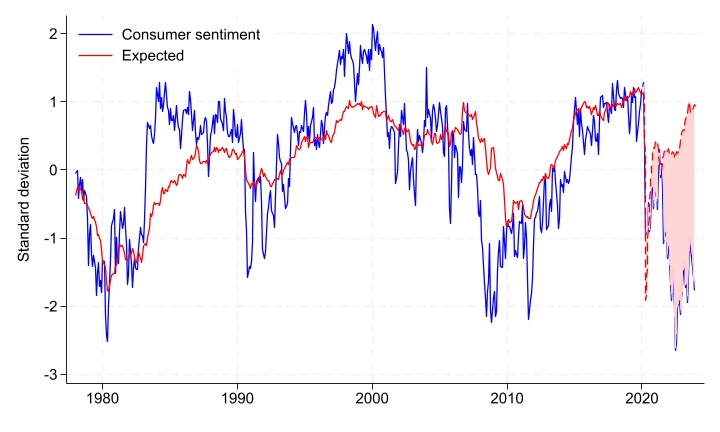

In new NBER paper with @MA_Bolhuis, @juddcramer and Oskar Shulz, we argue that the unprecedented increase in borrowing costs is crucial to explaining the low consumer sentiment of the last two years. 1/N nber.org/papers/w32163

With higher rates, mortgage payments, car payments, and other credit payments required to finance everyday purchases have risen as well. It is not surprising that this would affect how consumers feel about the economy. 2/N

Oct 9, 2023 • 7 tweets • 2 min read

In nearly 50 years of @Harvard affiliation, I have never been as disillusioned and alienated as I am today.

The silence from Harvard’s leadership, so far, coupled with a vocal and widely reported student groups' statement blaming Israel solely, has allowed Harvard to appear at best neutral towards acts of terror against the Jewish state of Israel.

Jun 12, 2023 • 5 tweets • 2 min read

Listen here to 20VC podcast where I talk with @HarryStebbings about how to manage inflation, why we need to change the US tax system and more.

First of all, we need to put it in perspective. A growing company can have a permanently growing debt. A growing economy can have a permanently growing government debt.

Jun 6, 2023 • 12 tweets • 3 min read

While I am glad to see that the “debt limit crisis” is in the rearview mirror, CBO projects budget deficits will exceed 7 percent of GDP and be on an upwards trajectory a decade from now.

youtube.com/live/2jcW_YomN… via @YouTube

For all of the post financial crisis/ pre-pandemic period I feared secular stagnation and opposed fiscal alarmism. But now I am alarmed because we are in new and dangerous territory.

May 15, 2023 • 4 tweets • 2 min read

Very good @WSJ interview with the very wise Bob Rubin on his new book, The Yellow Pad: Making Better Decisions in an Uncertain World, and the challenges facing the United States.

wsj.com/articles/rober… via @WSJ

The fact that the US is the only country where a career like Bob Rubin’s is possible makes me--for all our problems--more optimistic about our prospects than those of any other country.

Apr 30, 2023 • 10 tweets • 2 min read

@JakeSullivan46 is a very thoughtful leader and it's probably the most carefully intellectually developed exposition of the administration's philosophy that we have had to date.

Biden Administration's Industrial Policy bloomberg.com/news/videos/20…

Certainly, he's right that the world has changed. He's right that China represents a new kind of challenge. He's right to emphasize after what we've seen in Europe with oil, other things, the importance of resilience.

Apr 4, 2023 • 4 tweets • 1 min read

Today marks the 75th Anniversary of President Truman’s signing of the Marshall Plan into law. It might well be the greatest act of American foreign policy since World War II. Interesting to reflect on it today.

Could Congress imaginably today commit 2 percent of GDP, or about $500 billion, to a 4-year foreign assistance venture? Would the Marshall Plan have passed in 1948 if it had been focus grouped?

Mar 20, 2023 • 8 tweets • 3 min read

Transferring frozen Russian reserves would be morally right, strategically wise and politically expedient — particularly with a restive U.S. Congress.

washingtonpost.com/opinions/2023/…

There is elegant justice in using Russia's state funds, now lying idle, to counter the cost of Moscow's destruction.

Mar 17, 2023 • 4 tweets • 2 min read

I am not surprised that the group of big banks deposit in #FirstRepublicBank has done little for confidence. The banks committed for only 120 days whereas government money is in for a year, so there is not obvious economic substance.

There is no transparency on what understanding there are, or are not, with the @USTreasury. And it projects more than a whiff of alarm. Policymakers can do better.

Mar 12, 2023 • 6 tweets • 2 min read

There is much fog of war surrounding the #SVB situation. Impossible to assess or prescribe with confidence, based on public information. 1/

I hope and trust that the authorities are on a path to doing what is necessary to restore confidence. Acting decisively and rapidly is both the cheapest for taxpayers and the best for the economy. Failure to act strongly enough would be a Lehman-like error. 2/

Feb 28, 2023 • 5 tweets • 2 min read

New analysis with @asdomash of Phillips curve models first put forward a year ago confirms very substantial grounds for concern that inflation is not yet on a path back to 2 percent cepr.org/voxeu/columns/…

Contrary to what others have claimed, standard models of labor market slack are not overly pessimistic as predictors of inflation, and can readily explain observed ECI wage disinflation in recent months

Feb 26, 2023 • 5 tweets • 2 min read

I told @FareedZakaria@CNN: This has evolved towards a war of attrition. That is going to make what happens to the Russian economy, and even more importantly what happens to the Ukrainian economy, central to how this plays out.

Russian economic sanctions haven’t really bitten that hard because less than half the world has been involved as part of the sanctions. A large part of the worlds' GDP --China, India, Turkey-- have not been part of the sanctions.

Feb 25, 2023 • 5 tweets • 1 min read

Friday’s PCE figures, with both core and headline inflation running at 7 percent last month and big upward revisions for the 4th quarter, are very troubling.

They suggest that the @FederalReserve may have made much less progress in containing underlying inflation than has been generally supposed and make a soft landing look less likely.

Feb 18, 2023 • 4 tweets • 1 min read

1/The Fed's been trying to put the brakes on and it doesn't look like the brakes are getting much traction. And when your brakes don't get much traction, two things happen. You can be moving too fast, that's the inflation pressure.

via @YouTube

2/And you can be setting yourself up for some kind of collision or a crash down the road.

And both of those things, I think, are real risks in this environment.