Relentlessly curious -- I read a lot -- Big mouth -- Unintentional Bitcoinoclast -- @alphabetasoup_

6 subscribers

Uniformly, re-steepening of the curve out of inversion happens before or during recession, not after.

Uniformly, re-steepening of the curve out of inversion happens before or during recession, not after.

This isn't just a matter of gig workers hidden from unemployed, or marginally attached failing to apply for jobs or respond to surveys. Those things occur but they don't change this story.

This isn't just a matter of gig workers hidden from unemployed, or marginally attached failing to apply for jobs or respond to surveys. Those things occur but they don't change this story.

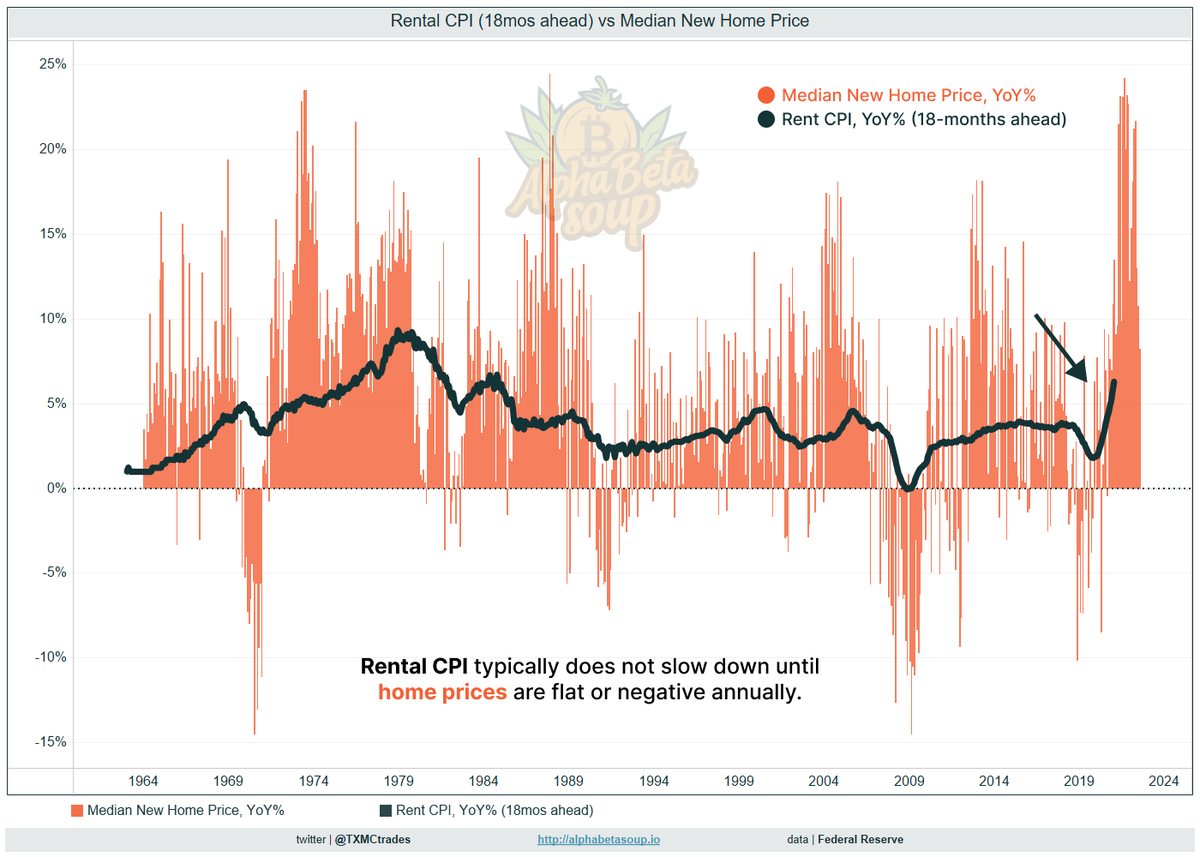

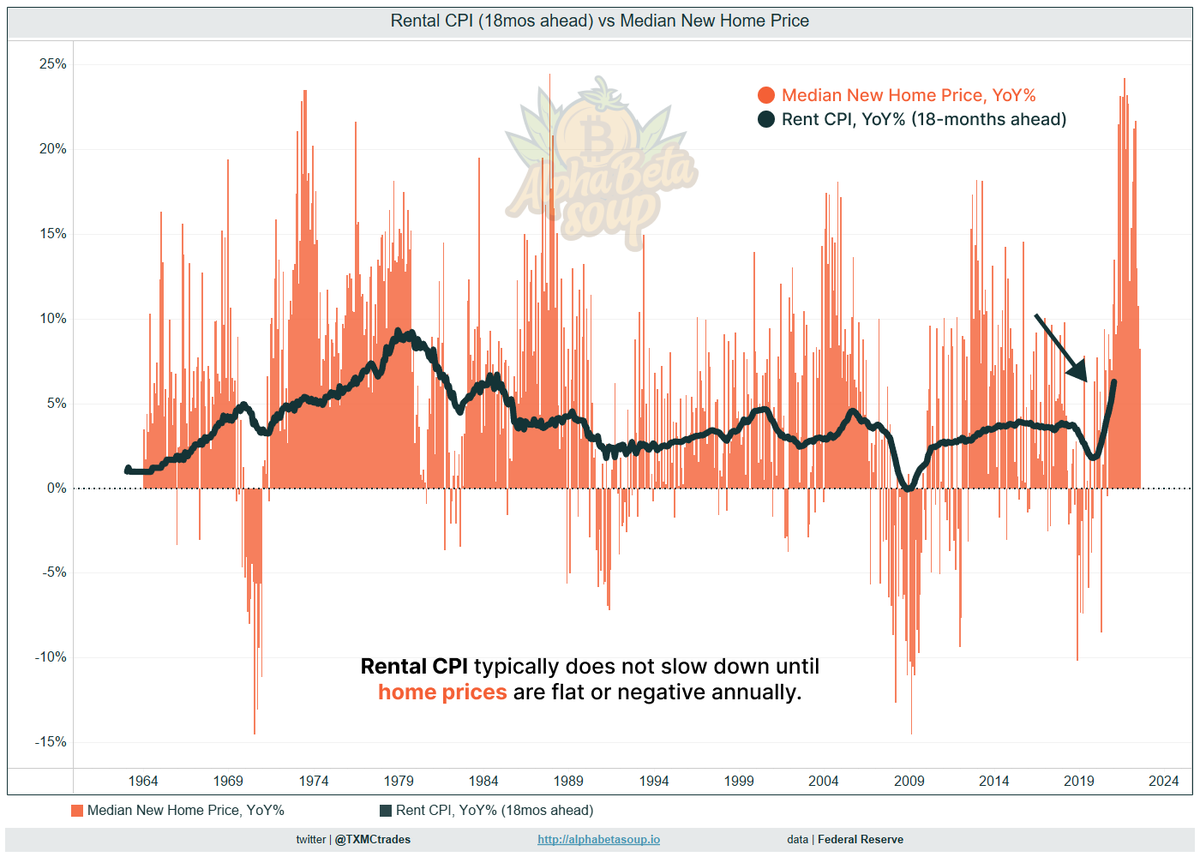

We begin with ⚫️rent CPI (18mos ahead) vs 🟠median new home prices annually.

We begin with ⚫️rent CPI (18mos ahead) vs 🟠median new home prices annually.

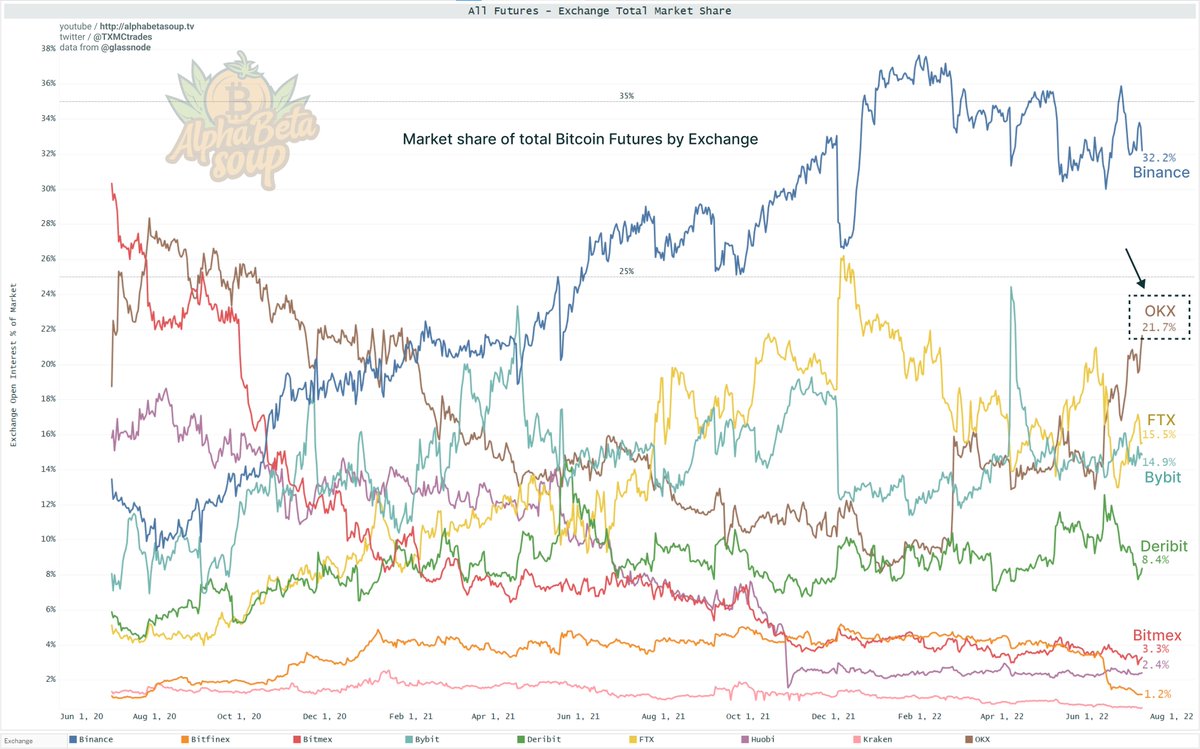

🟤OKX's star has been rising of late.

🟤OKX's star has been rising of late.