J Auto Trading Strategies, LLC

Think It 》Trade It 》Automate It

JATS: https://t.co/OFhHcSykxq

NT Vendor Affiliate

Disclosure: https://t.co/ZNROC7VB7x

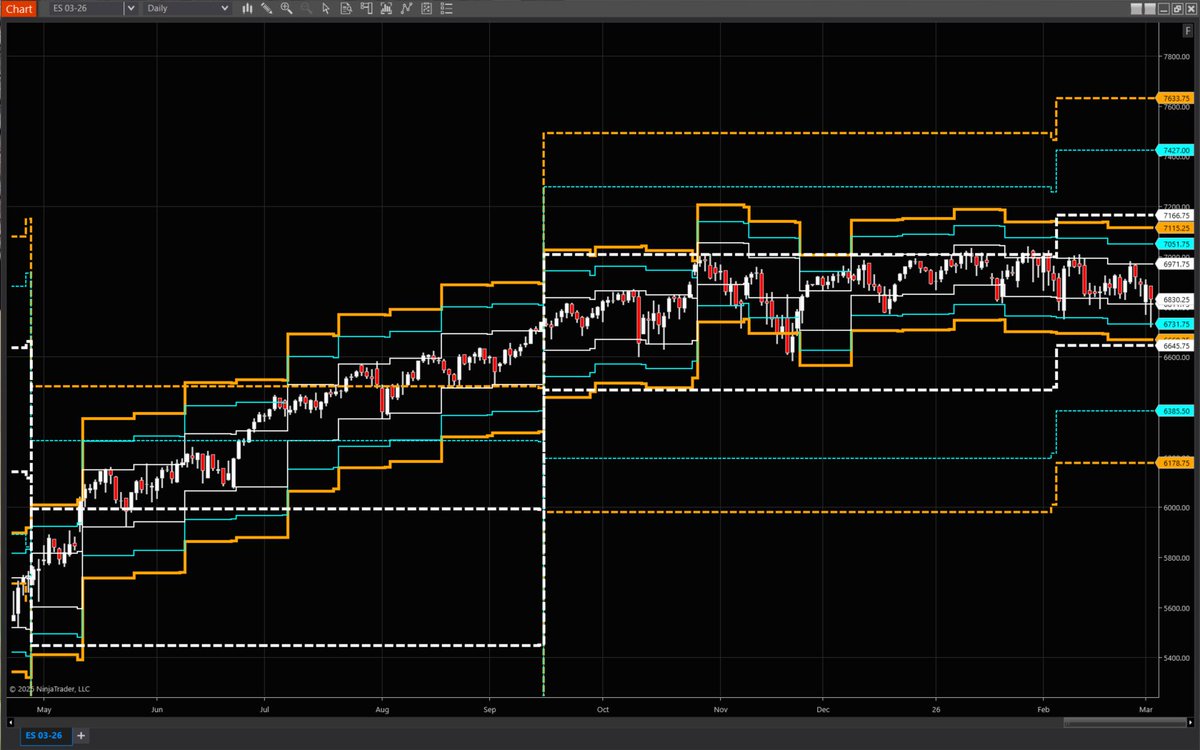

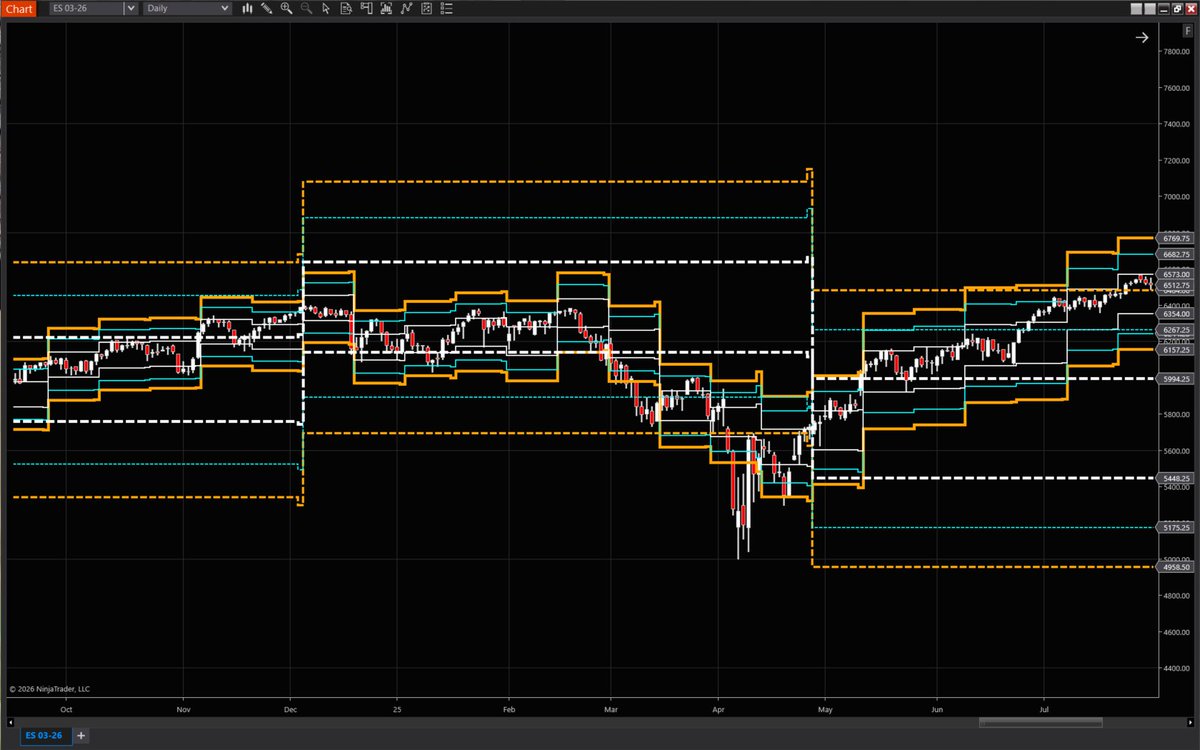

@zerohedge Example of them going short below the 100 Day distribution. Clear as a bell. Crystal clear.

@zerohedge Example of them going short below the 100 Day distribution. Clear as a bell. Crystal clear.

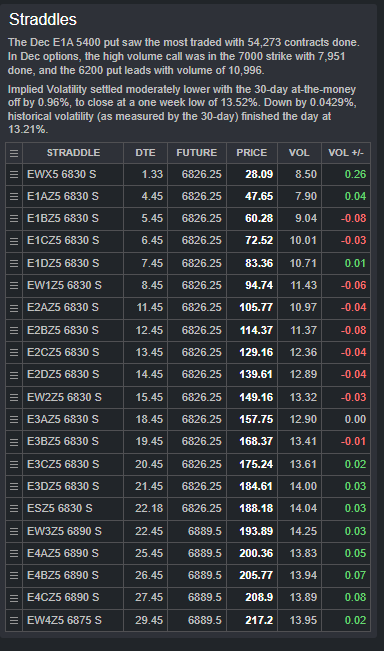

Navigating Year-End Volatility: S&P 500 (ES) Futures Outlook to 7,000 -- November 27, 2025 -- 22 DTE

Navigating Year-End Volatility: S&P 500 (ES) Futures Outlook to 7,000 -- November 27, 2025 -- 22 DTE

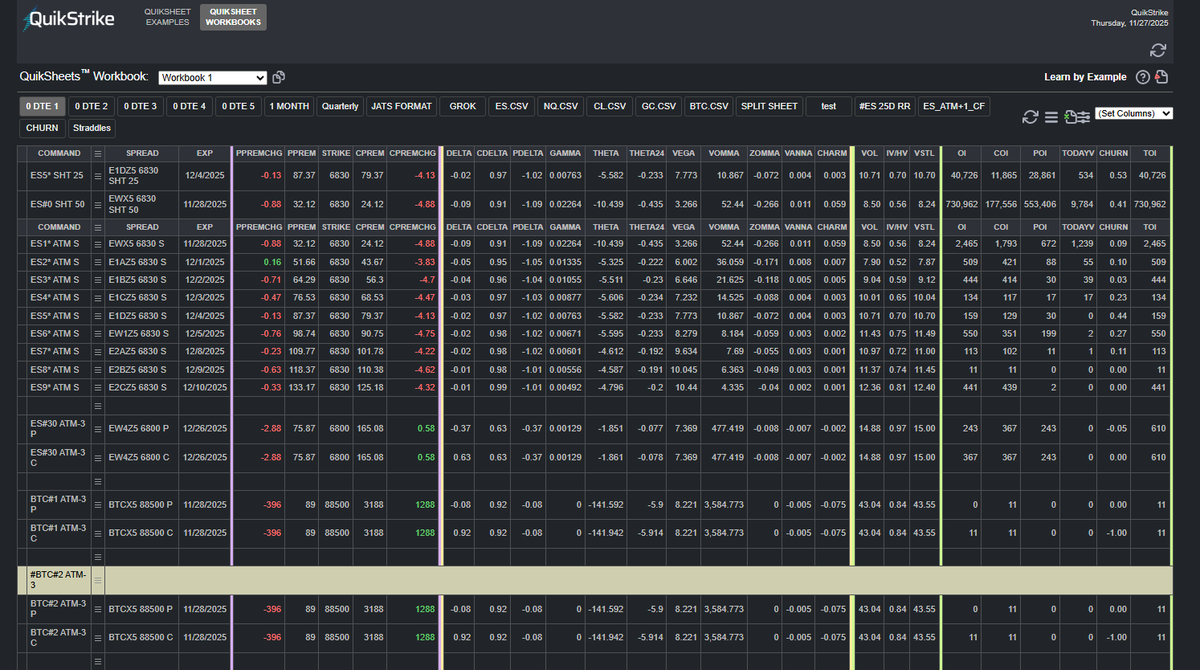

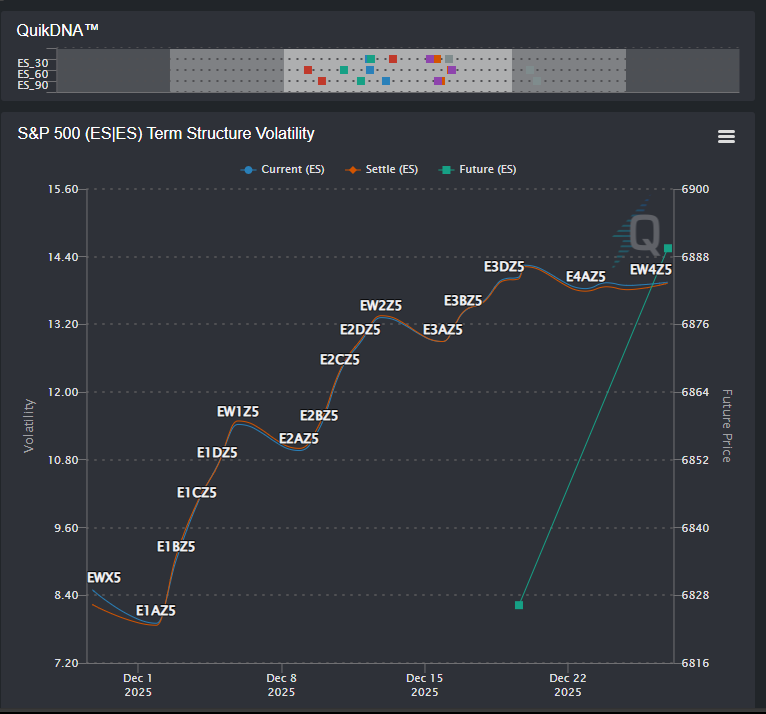

This means Central Banks are going to sell their equities and park cash at fed along with everybody else.

This means Central Banks are going to sell their equities and park cash at fed along with everybody else.