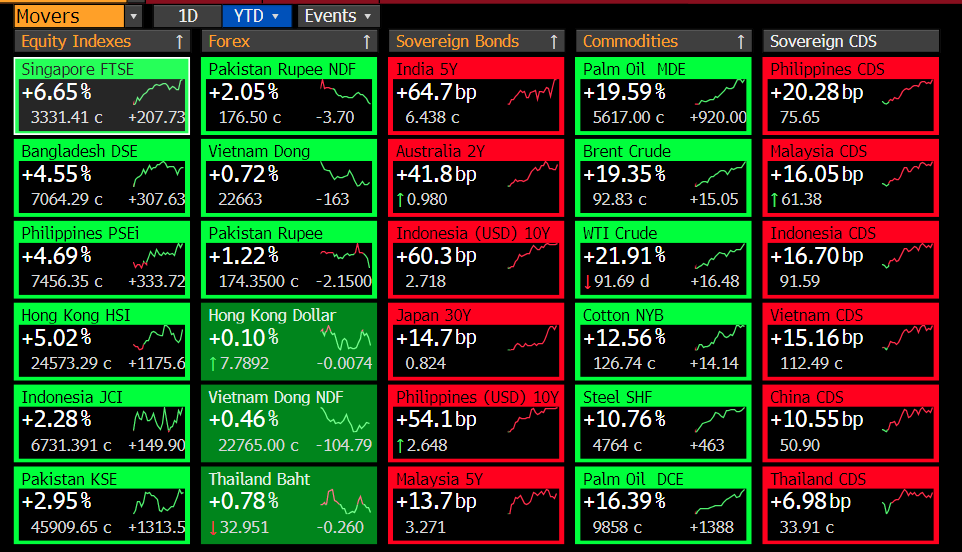

Good morning. Gloomy day in Hong Kong & gloomier in global markets:

SPX Futures -5%; US 30yr at 1%; Brent at 36USD & crude 32.9; EUR 1.138;

Nikkei opened -3.15%.

Urgh....

SPX Futures -5%; US 30yr at 1%; Brent at 36USD & crude 32.9; EUR 1.138;

Nikkei opened -3.15%.

Urgh....

I smell extreme global growth fear & price wear in the oil market.

Futures falling very hard. Buckle up. This is going to be a crazy week. Mayhem in markets.

Futures falling very hard. Buckle up. This is going to be a crazy week. Mayhem in markets.

Not helping Japan Q4 GDP WORSE than expected at -7.1% sa qoq annualized.

Btw, I was just there. Services are going to be hit hard by this virus if u thought Q4 2020 was bad. Watch out. And Japan isn't alone. Italy, South Korea, etc

Btw, I was just there. Services are going to be hit hard by this virus if u thought Q4 2020 was bad. Watch out. And Japan isn't alone. Italy, South Korea, etc

SPX futures 2819!!!

I have warned you: EQUITIES NOT DIVORCED FROM EARNINGS!!!

Markets re-pricing in future earnings very fast. Unless actions are taken on the existing debt load, watch out for those that have very bad balance sheets w/ earnings falling.

Markets re-pricing in future earnings very fast. Unless actions are taken on the existing debt load, watch out for those that have very bad balance sheets w/ earnings falling.

Also something else I have warned you & the World Bank latest book: We are facing a very cold winter & we have burned all the wood.

Burned!!! Look at rates globally. Look at the debt stock globally. CBs have been easing when nominal growth positive (ECB, BOJ etc). So now what?

Burned!!! Look at rates globally. Look at the debt stock globally. CBs have been easing when nominal growth positive (ECB, BOJ etc). So now what?

Guys, look at the year-to-date performance of assets:

Commodities - CRUSHED (well oil & gas)

US 5y -126.8bps

SPX -8% ytd (but futures falling so will be pretty intense tonight)

Commodities - CRUSHED (well oil & gas)

US 5y -126.8bps

SPX -8% ytd (but futures falling so will be pretty intense tonight)

Brent at 36/barrel. Someone on TV just asked a guest regarding WINNERS and said China could be the winner of this price fall given that it imports so could be a windfall for the consumers.

Nope, nope, nope!! Imagine the scenario in which Brent is at 36!!! Imagine! Demand shock!

Nope, nope, nope!! Imagine the scenario in which Brent is at 36!!! Imagine! Demand shock!

Look, I get people now going on TV, writing reports about how China is on the way to recovering where people are just beginning to be hit & they think China will be a shelter from the storm.

No, it has high debt, supply shocks (maybe recovering but still not 100%) & DEMAND shock

No, it has high debt, supply shocks (maybe recovering but still not 100%) & DEMAND shock

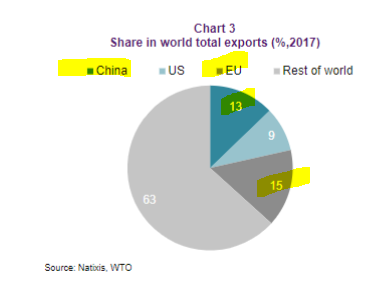

And who's the BIGGEST trader of them all? First the European Union & then China. They have the biggest global market share of exports of manufactured goods. We don't just have a supply shock (biggest is in China, although recovering), but a demand shock, who's gonna feel it MOST?

Look at China Jan + Feb exports - down -17.2% & we got Jan good data to help abysmal Feb data. That trend isn't going to be reversed w/ the on-going supply shock in China (Asia + world) & the massive demand shock we are just beginning to fell. Imagine the world where oil at 35.7

Btw, for those that spend time doing this % of GDP calculation of Tokyo Olympics 2020 potentially being cancelled.

Forget it. Don't waste ur time. Imagine the circumstance in which that is cancelled.

Do u know when it was last canceled? WW1 & WWII (1916, 1940 & 1944).

Yep. Yes

Forget it. Don't waste ur time. Imagine the circumstance in which that is cancelled.

Do u know when it was last canceled? WW1 & WWII (1916, 1940 & 1944).

Yep. Yes

Warned you on 20 February 2020 (and even earlier but I didn't want to scroll through all my tweets):

Can equities be divorced from earnings? 🙅🏻♀️🙅🏻♀️🙅🏻♀️ Remember, FOMO should not be an investment thesis & life philosophy as it is MORE VIOLENT in reverse .

Can equities be divorced from earnings? 🙅🏻♀️🙅🏻♀️🙅🏻♀️ Remember, FOMO should not be an investment thesis & life philosophy as it is MORE VIOLENT in reverse .

https://twitter.com/Trinhnomics/status/1230334549294321665?s=20

HSI -4%; Onshore China -2%; KOSPI -4%; Nikkei -5.6% (got a stronger JPY problem on top of everything else).

😬

😬

Nikkei -6% & that means BOJ buying ETFs have been in vain b/c markets just sell into it.

Central bank buying equities not helpful!

Central bank buying equities not helpful!

Trump aids drafting economic measures to combat virus fallout, this include expansion of paid sick leave.

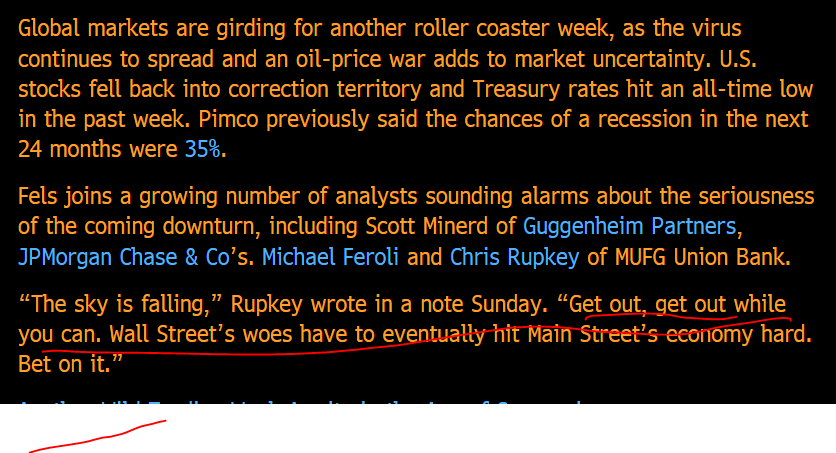

PIMCO chief economist warning: WORST IS YET TO COME (share his sentiment and if u have been following, u would see why I say this).

The risk is that we underestimate it. When China reported is WORST than ever PMIs, esp services, markets ignored & RALLIED on hopism. Hope!!

The risk is that we underestimate it. When China reported is WORST than ever PMIs, esp services, markets ignored & RALLIED on hopism. Hope!!

The ability to react:

No matter how non-sensible Japanese policy has been (VAT hike & BOJ buying ETFs), Japan is 1 country so easy to change course.

No matter how much u think Trump is mishandling, the US is a presidential system & can move quickly.

But Europe? 27 members!!!

No matter how non-sensible Japanese policy has been (VAT hike & BOJ buying ETFs), Japan is 1 country so easy to change course.

No matter how much u think Trump is mishandling, the US is a presidential system & can move quickly.

But Europe? 27 members!!!

The Euro zone has: Austria , Belgium, Cyprus, Estonia, Finland, France, Germany, Greece, Ireland, Italy, Latvia, Lithuania, Luxembourg, Malta, The Netherlands, Portugal, Slovakia, Slovenia and Spain

1 central bank, many diff economies, & plenty of opinions for fiscal.

1 central bank, many diff economies, & plenty of opinions for fiscal.

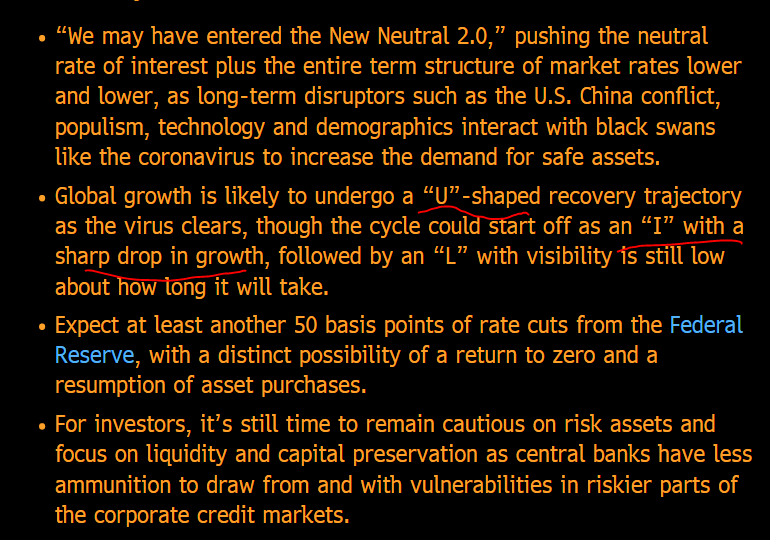

More from Fels (chief eco at PIMCO - bond fund) in terms of alphabet soup of recovery: ILU

I-shaped drop of supply & demand

L-shaped for a while

and then U-shaped recovery.

What's the diff b/n V-shaped vs U-shaped? V-shaped is those people that think SHORT & QUICK RECESSION 🤗

I-shaped drop of supply & demand

L-shaped for a while

and then U-shaped recovery.

What's the diff b/n V-shaped vs U-shaped? V-shaped is those people that think SHORT & QUICK RECESSION 🤗

Ovs there's nothing SHORT & QUICK about this as we're 9 March & China recovery is not 100% yet & we're already talking about the world being infected by the virus coming from China & so we got DEMAND SHOCKS GLOBALLY. U-shaped? GDP shrinks many quarter & don't come out for a while

So u're like, well, what else is there???

Best case scenario = V-shaped (not happening

Next best case = U-shaped (recession for a while - think 1973-1975 USA)

Next best case = W-shaped (recession, recover & slip back into a recession - think USA early 1980s).

Obvs worst case is

Best case scenario = V-shaped (not happening

Next best case = U-shaped (recession for a while - think 1973-1975 USA)

Next best case = W-shaped (recession, recover & slip back into a recession - think USA early 1980s).

Obvs worst case is

L-shaped is the worst case - u don't recover (think Japan after the 1980s bubble).

So there u go. So when u get reports that say V-shaped, u can be like, hmm, I know what u mean, & think U-shaped, W-shaped & even L-shaped.

😬

So there u go. So when u get reports that say V-shaped, u can be like, hmm, I know what u mean, & think U-shaped, W-shaped & even L-shaped.

😬

Remember that during trade-war, my thread was not consensus & 1 year later it became the consensus view.

This is not a V-shaped recovery guys. Think for a second. Services income losses NOT RECOVERABLE. Debt not erased. So what?

No pent-up demand for services after this is over

This is not a V-shaped recovery guys. Think for a second. Services income losses NOT RECOVERABLE. Debt not erased. So what?

No pent-up demand for services after this is over

In fact, we may have people exercising RESTRAINT when they don't need to (like myself) just because it doesn't feel right to conspicuously consume when others are suffering etc.

So, people that say pent-up demand don't understand human psychology & services. Only 24 hrs a day!!!

So, people that say pent-up demand don't understand human psychology & services. Only 24 hrs a day!!!

No one is going to take that cruise ship they didn't take in Q1 & early Q2! Or haircut they didn't take or Southeast Asia extravaganza.

They will just at best case scenario resume the services they did in the subsequent quarters. Income losses incurred & so will feel pinched!

They will just at best case scenario resume the services they did in the subsequent quarters. Income losses incurred & so will feel pinched!

• • •

Missing some Tweet in this thread? You can try to

force a refresh