Today when Equity Markets have crashed & SIP investors esp. ones who started in last 5 years & are seeing the investments in red are worried. This is an effort to address them through a first-hand story of my SIP in Franklin India Prima Fund. @FTIIndia @Anand_1969 @Sanjay_69 1/21

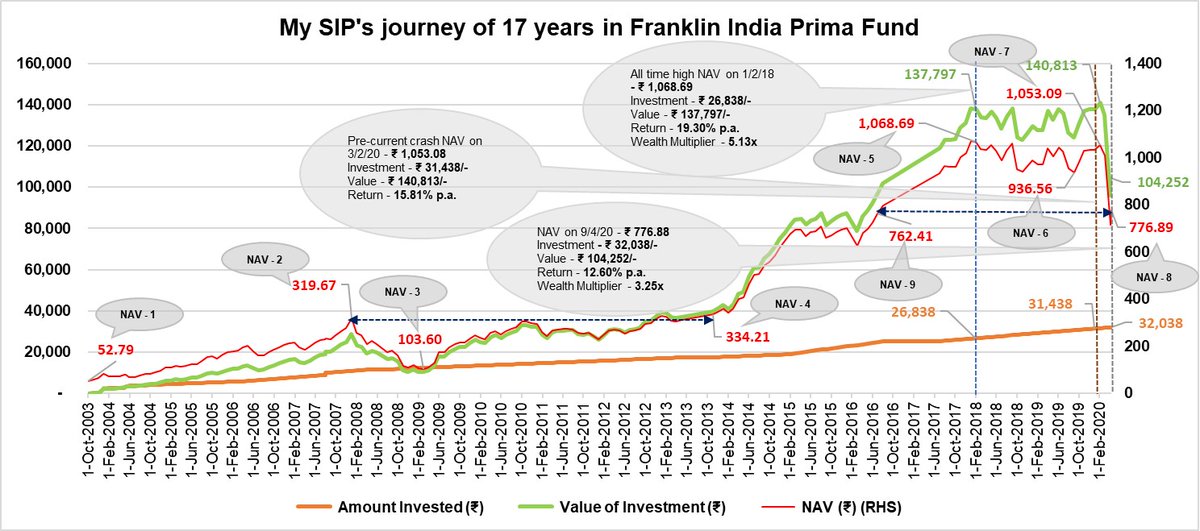

I started this SIP on 1/10/20013 & the investment values are re based to Rs. 100/- as on that date. There have been 198 months since then & I invested on 186 out of these. There were only 3 small lump-sum investments done outside the SIP installments in these 18 years. 2/21

The 1st installment went in at the NAV of ₹ 52.79 (NAV – 1 in the chart) & the market continued to rise continuously for the next 4.5 years with the Fund hitting an all-time high NAV of ₹ 319.66 (NAV – 2) on 31/12/2007 (reference to my transactions only), a rise of 506%. 3/21

Then came the 2008 Lehman Bros. crash & the NAV fell to ₹ 103.59 (NAV - 3) on 27/2/2009, a crash of 68% in 14 months. The markets rose steadily again from this bottom & the fund crossed its pre-crash high on 1/11/2013, a rise of 223% in 4.5 years. 4/21

This still saw the fund give virtually no returns for the period of 6 years (12/07 to 11/13). The markets then saw a sustained bull run, where the fund hit its current all-time high NAV of ₹ 1,068.09 on 1/2/18 (NAV-5), a return of 220% in another 4.5 years. 5/21

Then came the so-called crash in Mid & Small cap stocks in 2018, where the NAV moved down to ₹ 936.56 (NAV-6) on 3/9/19, a fall of 12% (which seems miniscule now) in 18 months. The Fund regained this fall in 9 months, NAV reaching ₹ 1,053.59 (NAV-7) on 3/2/20. 6/21

Suddenly, all hell broke loose with the #COVID19 scare across the globe & every market started crashing. The NAV fell to a low of ₹ 714.88 for SIP instalment of 3/4/20 & has recovered slightly to ₹ 776.88 as of 9/4/20 (NAV-8), a fall of 26% in 2 months. 7/21

The fund is now trading at the NAV that it had seen last on 1/7/16 of ₹ 762.41 (NAV-9). Thus, close to 4.5 years of returns have been wiped out in the current fall. To cut the long story short, how is my investment in the Fund faring? 3 computations shown ahead. 8/21

1st computation shown when the Fund was at the All-time high NAV on 1/2/18 – Amount invested till then: ₹ 26,838/-, Value of investment: ₹ 137,797/-, Return till date: 19.30% p.a., Wealth Multiplier – 5.13x. 9/21

2nd computation shown at the point before the current crash at the NAV of ₹ 1,053.08 on 3/2/20 – Amount invested till then: ₹ 31,438/-, Value of investment: ₹ 140,813/-, Return till date: 15.81% p.a., Wealth Multiplier – 4.48x. 10/21

3rd computation as of 9/4/20 at the NAV of ₹ 776.88 – Amount invested so far: ₹ 32,038/-, Value of investment: ₹ 104,252/-, Return till date: 12.60% p.a., Wealth Multiplier – 3.25x. 11/21

Am I worried when my return has fallen from 19.30% p.a. to 12.60% p.a.? A BIG NO. Why? I don’t think I am going to need this Money for the next 10 years, & I will continue to invest Fund till then. Lower the NAV (like current times), more units I will accumulate. 12/21

The more the units I accumulate, the lower will be my average purchase price in the Fund. Eventually when the markets go up (and they will), the units bought at lower NAV will show the maximum gains. This is where Rupee Cost Averaging works in our favour. 13/21

Once I stop investing, I am not going to need all the money immediately, and I will have to fund my retirement for the next 30 years, assuming I live till 90 and the world does not come to an end before that. 14/21

It could so happen that I may continue to be invested in the Fund for another 25 years from now (taking me to the year 2045), and my total holding to 43 years since I started in 2003. I hope that @FTIIndia continues to manage the Fund properly till then. 15/21

Even if I make 12% p.a. from here over the next 25 years (which is my current return for the last 18 years and computed at a point when the markets have crashed), I believe it will continue to create Wealth for me (not getting into the computation here). 16/21

Moral of the Story: 1) We all have Long-term goals in Life! Equity is Risky, but the Loss of Purchasing Power (read inflation) is a bigger risk. In addition to the regular Inflation (Roti, Kapda, Makan), we also have to account for the Lifestyle Inflation. 17/21

Moral: 2) Equity is the only Asset Class that beats Inflation in the long-run, and you cannot afford to not use Equity for your Long-term goals. 18/21

Moral: 3) In addition to Equity, you need to be diversified across Asset Classes (Asset Allocation), the importance of it will be known post the COVID19 scare. People may lose jobs, or face pay cuts, or the income for self-employed will come down / fluctuate. 19/21

Moral: 4) If you have adequate back-up (emergency funds) available in Debt (MFs, FDs, etc.), only then it will be possible to maintain your current lifestyle over the next few years post these challenging times. 20/21

Moral: 5) This money will only come handy to you if you are around to use it. Please stay at home till the Lockdown is over, please stay safe and please take good care of yourself and your loved ones. #Stayhome #Staysafe #MutualFundsSahiHai. 21/21

Tagging a few of my friends further - @AmitMTrivedi @simpleharish @mohanty_swarup @VinayakSapre1 @BIVALKAR @RanjitDani @MFSahiHai

Read the SIP start date as 1/10/2003 in Tweet 2/21.