1/ Investments in PPE (property, plant and equipment) appearing on balance sheets no longer drive profits as much as they once did. Businesses invest more in intangible assets like software that are expensed, which lowers GAAP "earnings." Determining what creates value is hard.

2/ Michael Mauboussin has pointed me toward this paper:

"Should Intangible Investments Be Reported Separately or Commingled with Operating Expenses?" papers.ssrn.com/sol3/papers.cf…

"Intangible investments are outlays that lack physical substance but produce future benefits..."

"Should Intangible Investments Be Reported Separately or Commingled with Operating Expenses?" papers.ssrn.com/sol3/papers.cf…

"Intangible investments are outlays that lack physical substance but produce future benefits..."

3/ Investors who limit their analysis to GAAP and/or who invest based on P/E multiples are huge sources of outperformance for anyone who understands how intangibles drive business value today. The speed GAAP moves makes a slug crossing a driveway look like Formula 1 racing speed.

4/ I should arguably be happy that most people don't understand how important intangible assets are to valuation today. After all, as Charlie Munger says: “For a security to be mispriced, someone else must be a damn fool. It may be bad for the world, but not bad for [Tren]."

5/ More people understanding this fundamental shift to intangible assets creating value is important enough for the world that I can't be silent. Dysfunctional decision making based on a broken GAAP system harms everyone. Less decision making foolishness is needed in this world!

6/ Why do so many people ignore the value of intangible assets? Because determining their value is hard. Humans are imitating and status seeking creatures by nature, but they are also lazy. The creative gymnastics people will do to avoid doing any work are impressive to watch!

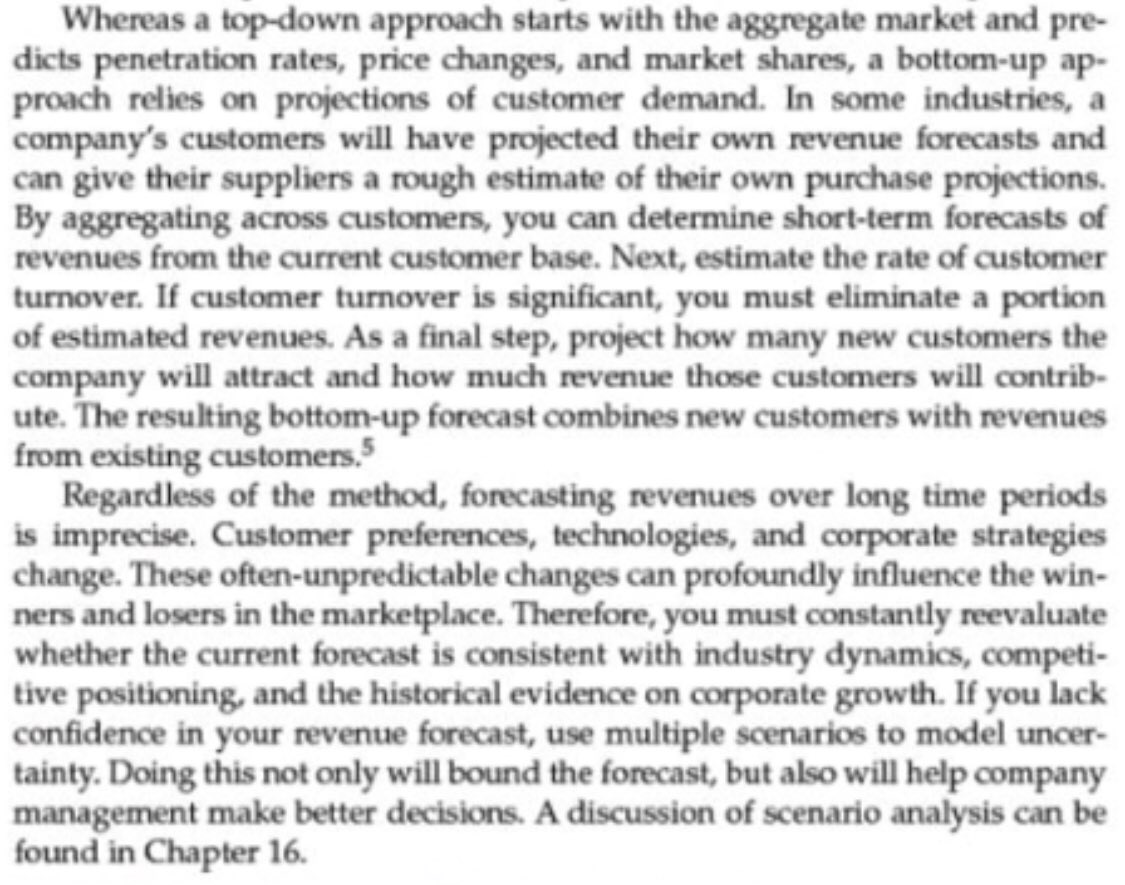

7/ There are two ways to do a valuation: top down and bottoms up. A sound process involves both and a a reconciliation of the two valuations. @d_mccar pointed today at this passage in the revised McKinsey valuation book. The book cites his great unit economics work with @faderp.

8/ If you have been reading my blog and Twitter over the years you know I believe investing advantage exists in bottoms up analysis that is fundamentally a DCF. By doing this unit economics work the value of intangible asset appears in ROIC *if it exists*. 25iq.com/featured-indiv…

9/ Every customer is potentially a future stream of cash. Estimate average value via DCF and then add them up. That’s bottoms up. I don’t strive for false precision (approximately right rather than precisely wrong). To deal with mistakes I apply a margin of safety to the result.

10/ If a business is no longer a true startup and is destroying value on a unit economics basis it wise to turn around and run away like a ferocious tiger is chasing you. If the unit economics business can't be determined put it in your "too hard" or "unpleasantly smelling" pile.

12/ Baruch Lev "I trace the deterioration of the usefulness of financial information [in part] to standard-setters’ failure to adjust asset recognition rules to the fundamental shift in corporate value-creating resources from tangible to intangible assets."tandfonline.com/doi/full/10.10…

13/ Without a bottoms up reconciliation of value done on a unit economics basis with a top down valuation you don't know if R&D spending creates shareholder value or how much it does create value if it does. Some R&D is a destructive bonfire of cash and some isn't. It depends.

14/ Whatever you do, don't forget that the first rule of investing in stocks is: Expected long-term cash flows, discounted by the cost of capital—not reported earnings—determine stock prices. The second rule of investing is: don't forget the first rule. expectationsinvesting.com/about.shtml

15/ John Collison: "Capital obviously has really moved over the past hundred years away from heavy machines that you’ll really hurt your foot if you drop one on them to intellectual capital and intangible capital."

Not GAAP because it came down from a mountain on stone tablets!

Not GAAP because it came down from a mountain on stone tablets!

16/ "These days with technology businesses, what is the capital within the business? One of the assets a business may have is software that has been developed in house by the business. At Google it is the search engine that’s it." John Collison investorfieldguide.com/collison/

16/ Bottoms up valuation!!

"CBCV: Reshaping the Practice of Corporate Valuation Using a Customer-Driven Approach.” msi.org/articles/2019-… "valuing the current and likely future income streams from a company’s market-based assets, in particular its customers."

"CBCV: Reshaping the Practice of Corporate Valuation Using a Customer-Driven Approach.” msi.org/articles/2019-… "valuing the current and likely future income streams from a company’s market-based assets, in particular its customers."

17/ The work of @d_mccar & @faderp is changing marketing, finance, investing and someday, accounting.

My big regret last year was not being at a Michael Mauboussin guest lecture in Dan McCarthy's class. "You have no idea how lucky you are" is how I introduced Mauboussin once.

My big regret last year was not being at a Michael Mauboussin guest lecture in Dan McCarthy's class. "You have no idea how lucky you are" is how I introduced Mauboussin once.

"In his 1986 letter Warren Buffett writes about [owner earnings]. The interesting thing about that definition was splitting out two forms of capex:

1) investment required to keep same competitive position;

versus

2) capex required to expand."

John Collison

1) investment required to keep same competitive position;

versus

2) capex required to expand."

John Collison

18/ "Buffett talks about the textile mill that Berkshire got its start with and it just being such an incredibly terrible business because you’re spending all this capex just to tread water. [With capex] are we maintaining our competitive position or expanding?"

John Collison

John Collison

• • •

Missing some Tweet in this thread? You can try to

force a refresh