Fourth edition of our Macroeconomics of COVID in India series with @tulsipriya_rk

#EconTwitter

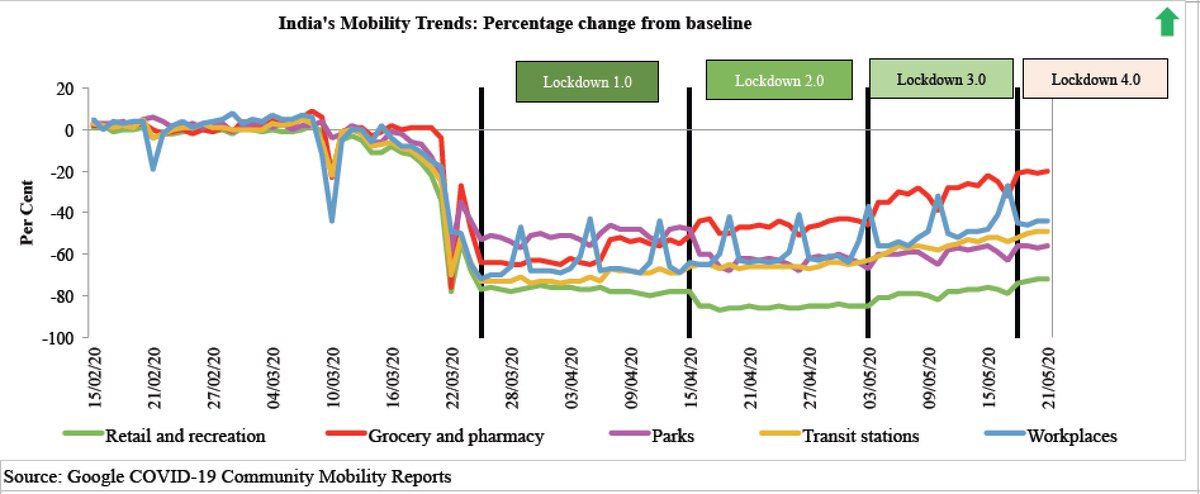

Having entered the ‘Unlock’ phase from June 1 with gradual resumption of services and businesses, some early signs of economic revival are visible in the first three weeks of June.

#EconTwitter

Having entered the ‘Unlock’ phase from June 1 with gradual resumption of services and businesses, some early signs of economic revival are visible in the first three weeks of June.

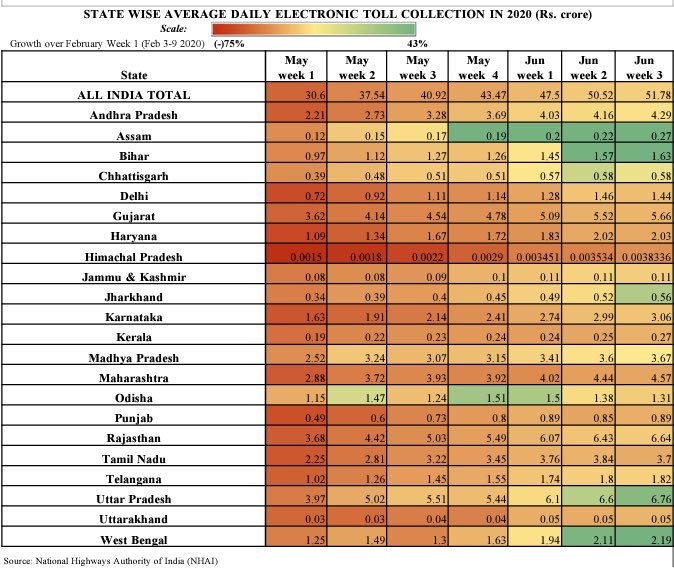

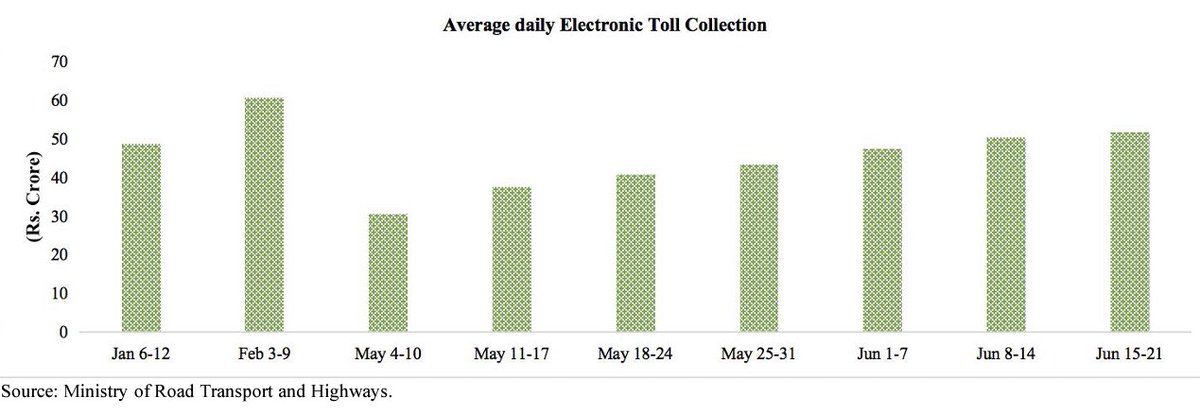

2/n Compared to pre-COVID scenario, electronic toll collections have shown marked improvement WoW mid-May onwards across all states. Assam, Bihar, West Bengal, Uttar Pradesh and Jharkhand reported greatest pick up in third week of June compared to Feb levels. @tulsipriya_rk

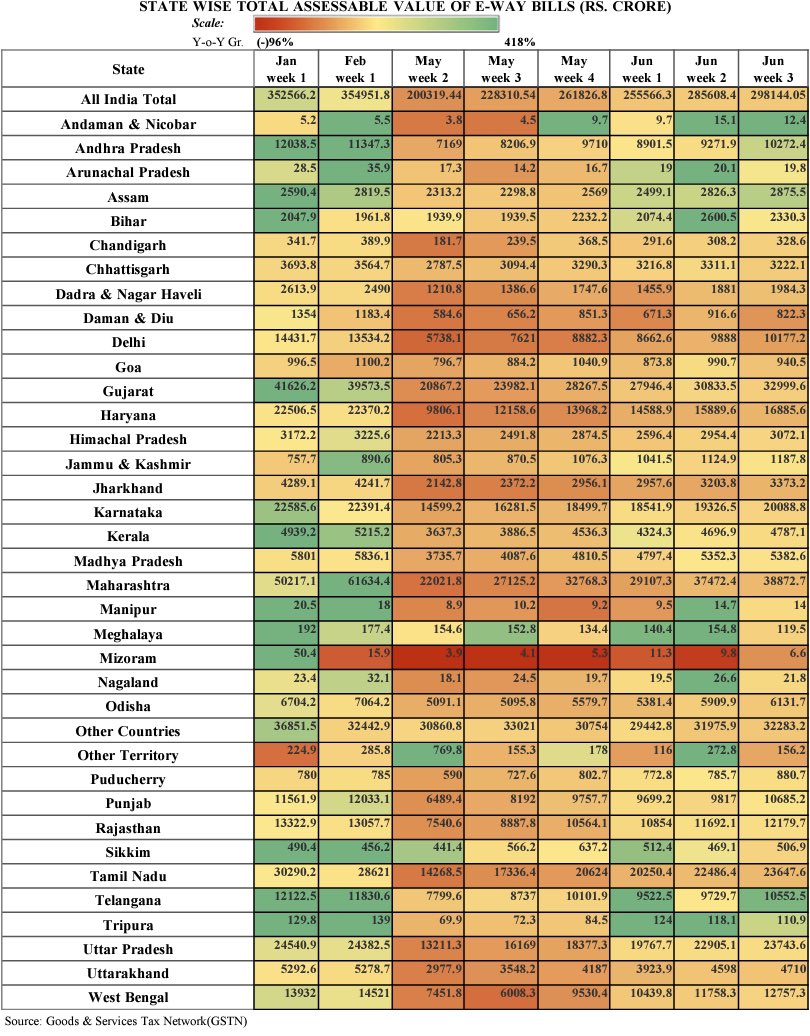

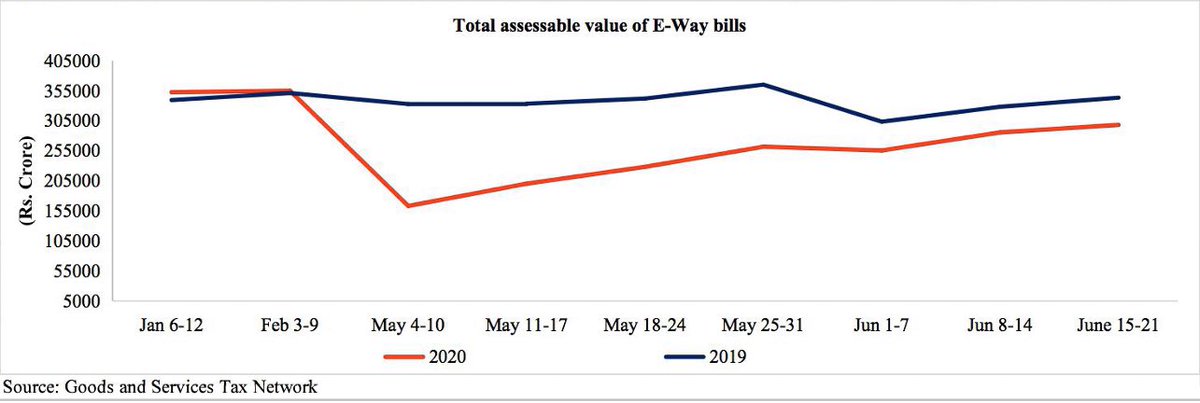

3/n Moderate improvement in value of E Way bills from May to June relative to previous year across all states including COVID-19 hotspots. Andaman, Telangana, Andhra Pradesh, Assam and Tripura witnessed improvement in the third week of June. @tulsipriya_rk

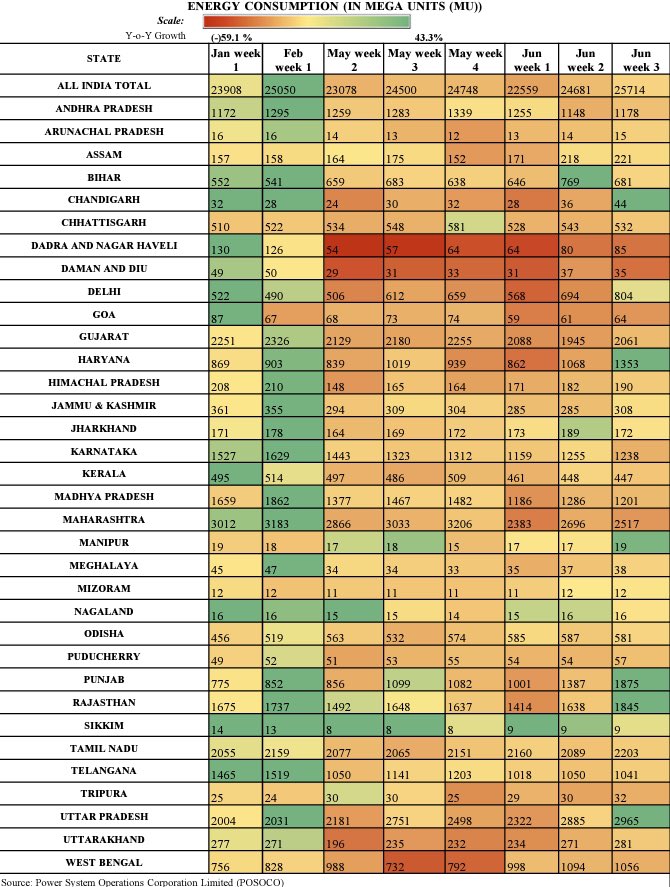

4/n Pickup in power consumption from May to June relative to previous year across all states. Chandigarh, Haryana, Manipur, Punjab, Rajasthan and UP witnessed greatest improvement in the third week of June. However, hotspots- MH and KA showed YoY declines.@tulsipriya_rk

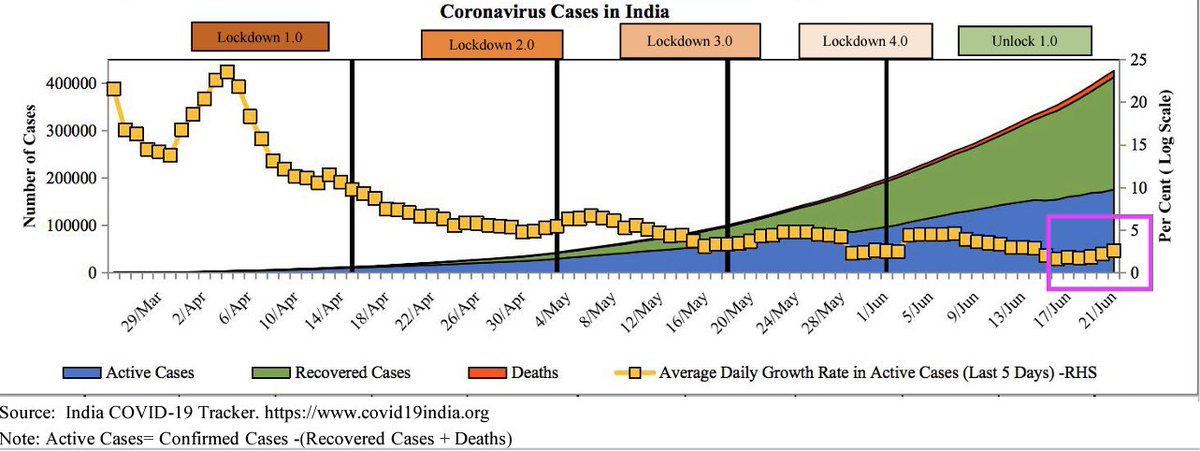

5/n Active cases growth rose to 2.61 per cent in wk ending 21st June, recovery rate also persistently increased, at 56.3 per cent on 22nd June. Deaths sharply rose by 2004 cases on 16th Jun amid major data adjustments for Delhi and MH. @tulsipriya_rk

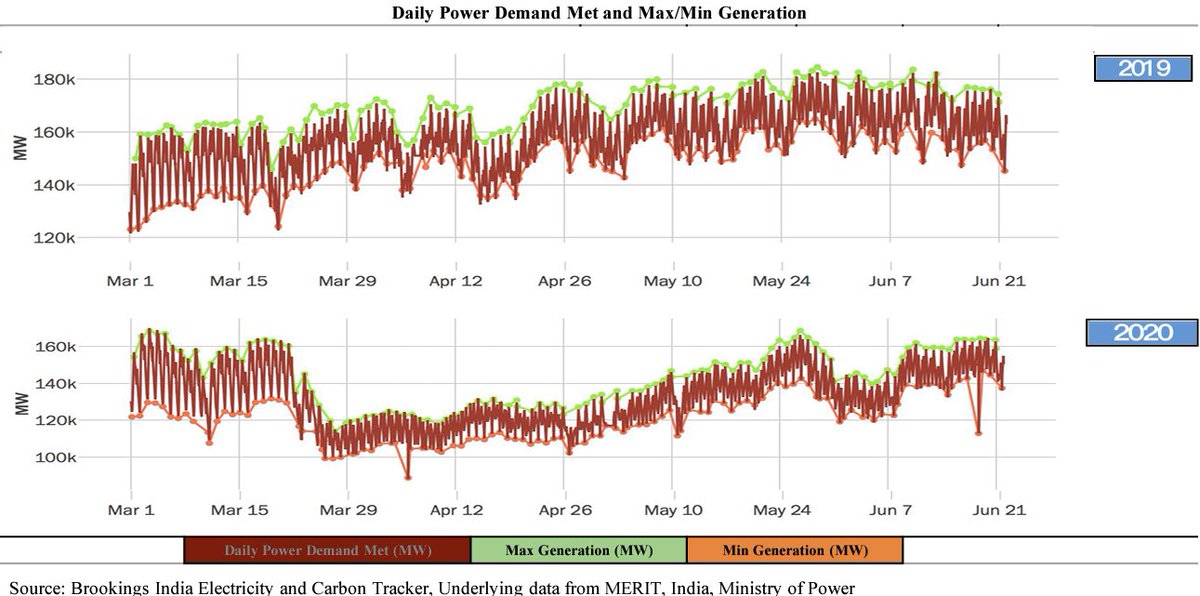

6/n Electricity generation continued to gain pace for second consecutive week increasing by 5.7 percent (WoW basis) amid boost in demand due to soaring temperature in north and gradual resumption of industrial activity. @tulsipriya_rk

7/n Value of E- way bills grew by 4.4% (WoW basis) compared to previous week growth of 11.8 %. June is experiencing good recovery as value of E-Way bills in the first three weeks have reached ~84% percent of Feb levels. @tulsipriya_rk

8/n Average daily toll collections continued to pick up reaching Rs.51.2 crore in 3rd week of June @tulsipriya_rk

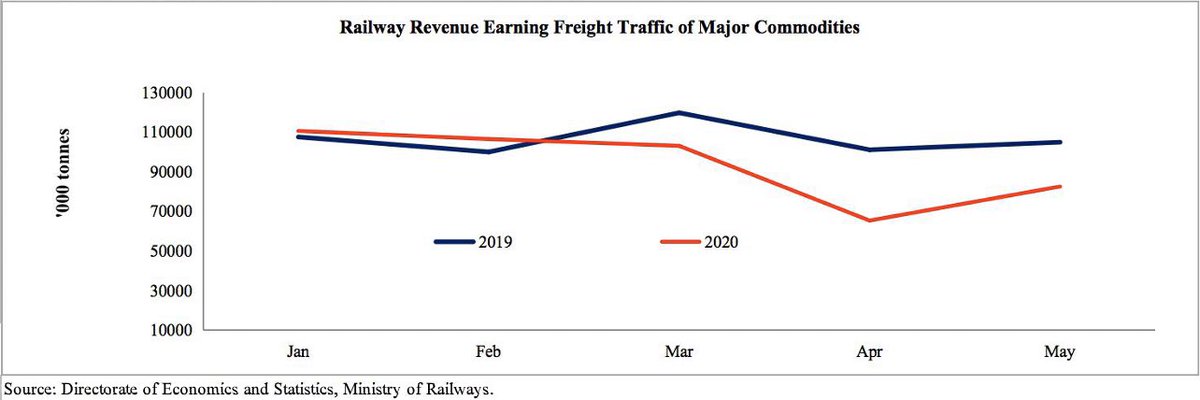

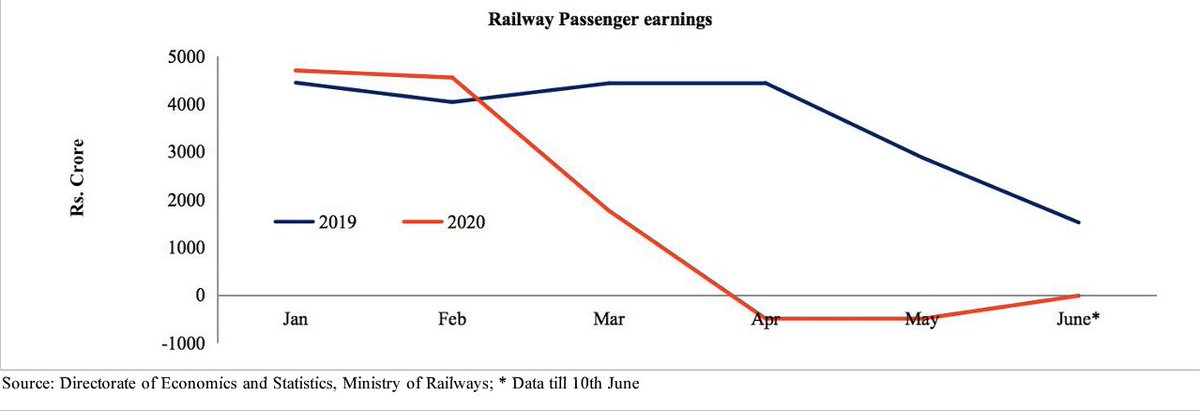

9/n Railway freight traffic improved by 26% in May (8.26 crore tonnes) over April (6.54 crore tonnes). Passenger earnings experienced some recovery in first ten days of June, though continuing to remain in negative territory. @tulsipriya_rk

10/n Household demand for MGNREGA work in June reached 3.9 crore, 54.5 percent higher than full month demand of previous year. 94.4 crore person days have been generated so far in FY 2020-21 (till June 23).

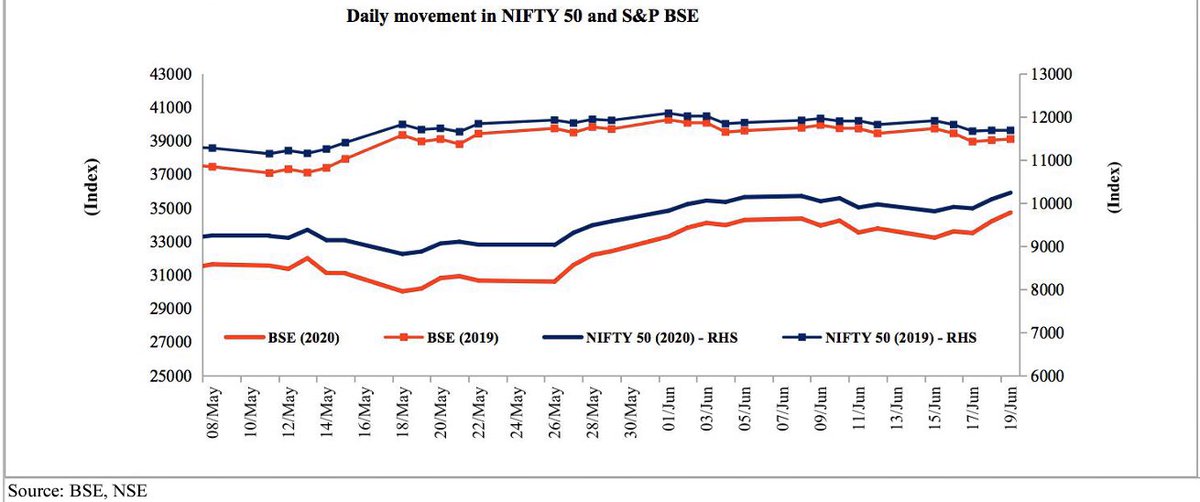

11/n Nifty 50 and Sensex regained losses of 2nd week of June by increasing 2.7% and 2.8% respectively in 3rd week of June, possibly backed by sharp pickup in equities of Reliance Ind. after its declaration of becoming net debt free @tulsipriya_rk

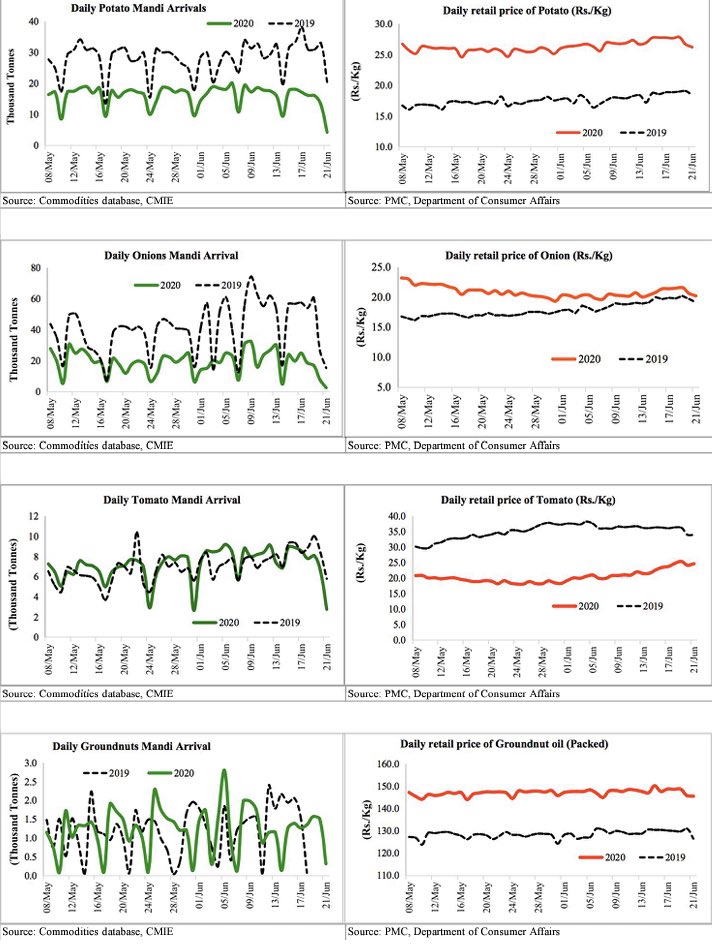

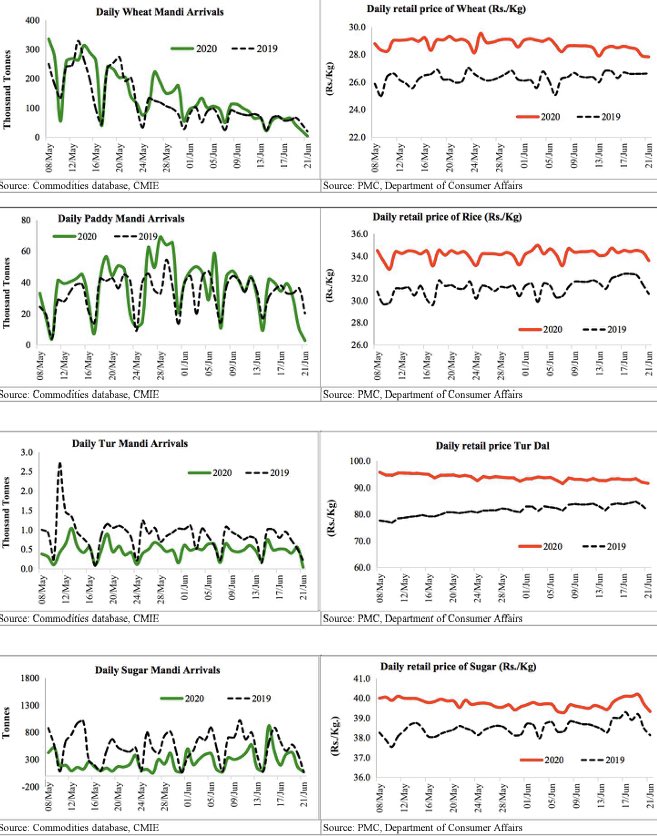

12/n Mandi arrivals for major essential agricultural commodities continued to decline in the week gone by except for sugar and groundnut. Retail prices eased across commodities barring tomato. @tulsipriya_rk

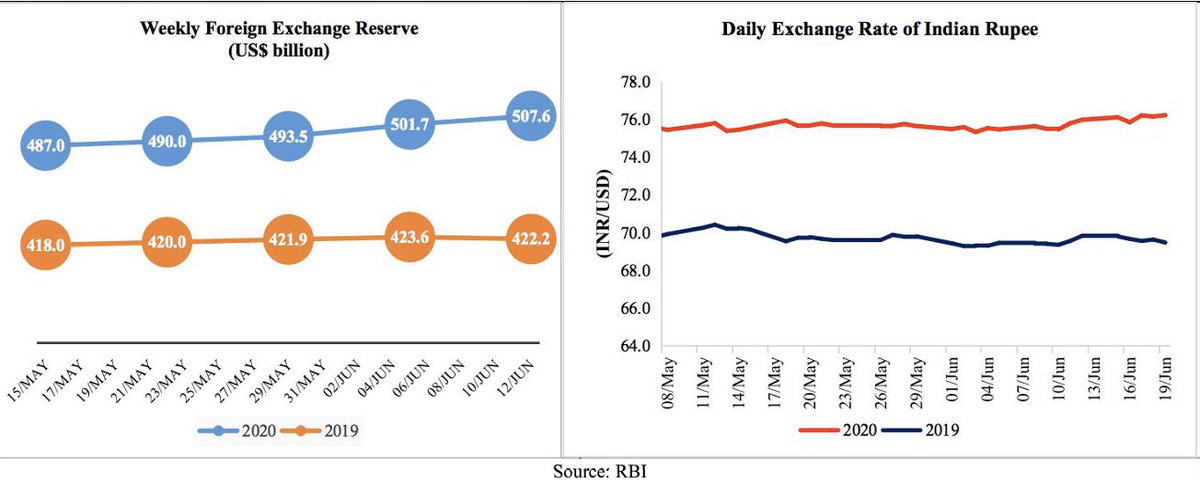

13/n Forex reserves continued to soar Rupee marginally depreciated in the week gone by amid FPI outflows and passive presence of RBI in the forex market. @tulsipriya_rk

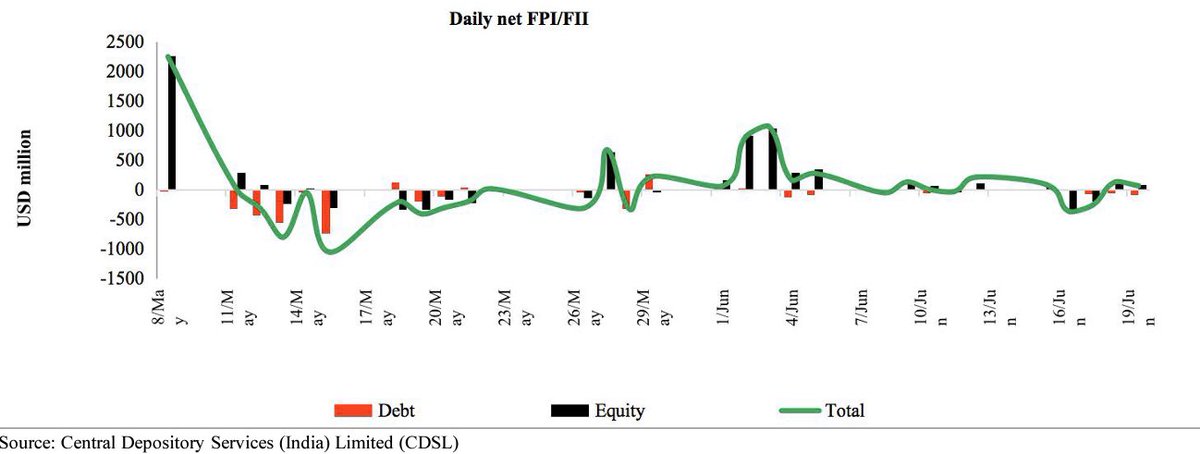

14/n FPI investors pulled out $342 million from the market in 3rd week of June with both debt and equity capital investors remaining net sellers. @tulsipriya_rk

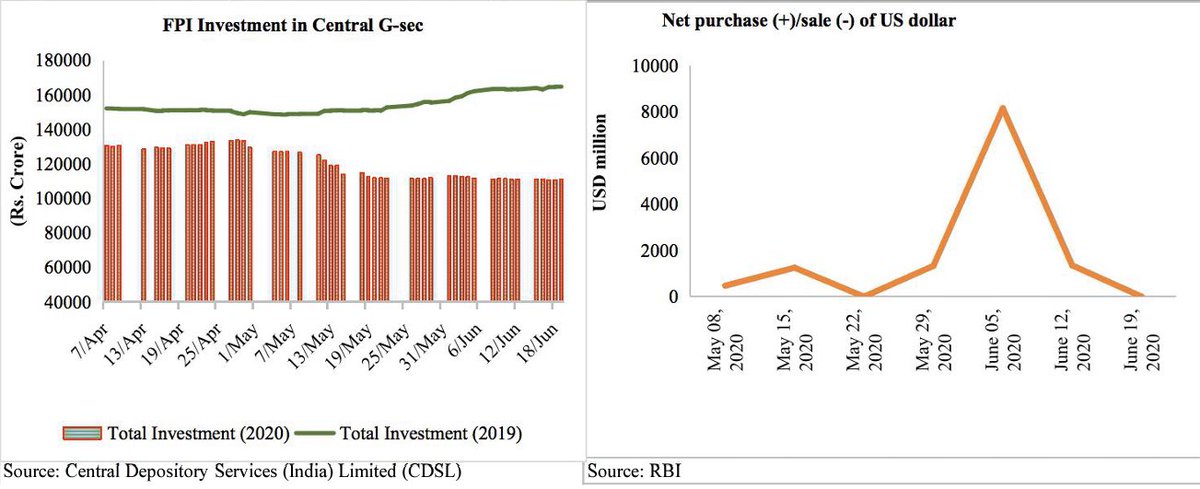

15/n FPI investment in Central G-Secs, at Rs. 1.1 lakh crore, declined by 0.3% in the week ending 19th June. RBI neither purchased nor sold dollars in the week after two consecutive weeks of purchases. @tulsipriya_rk

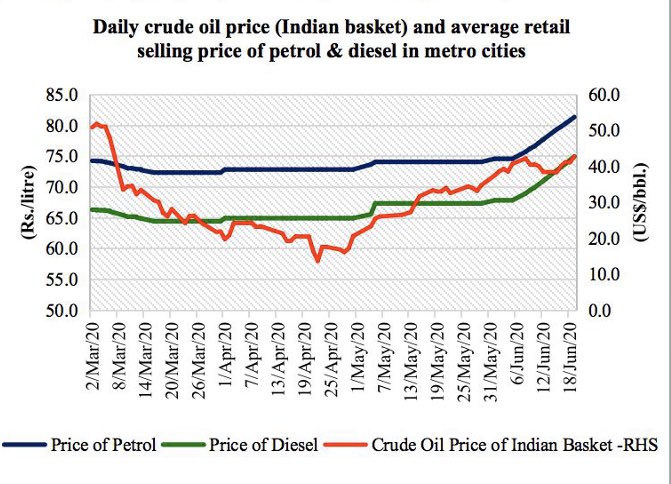

16/n India's crude oil price increased by 11.3% in the week gone by. Prices of petrol and diesel increased further by 4.7% and 5.5% respectively. @tulsipriya_rk

17/n Gold futures price rose further by 1.3% in the week gone by amid rising COVID cases globally.

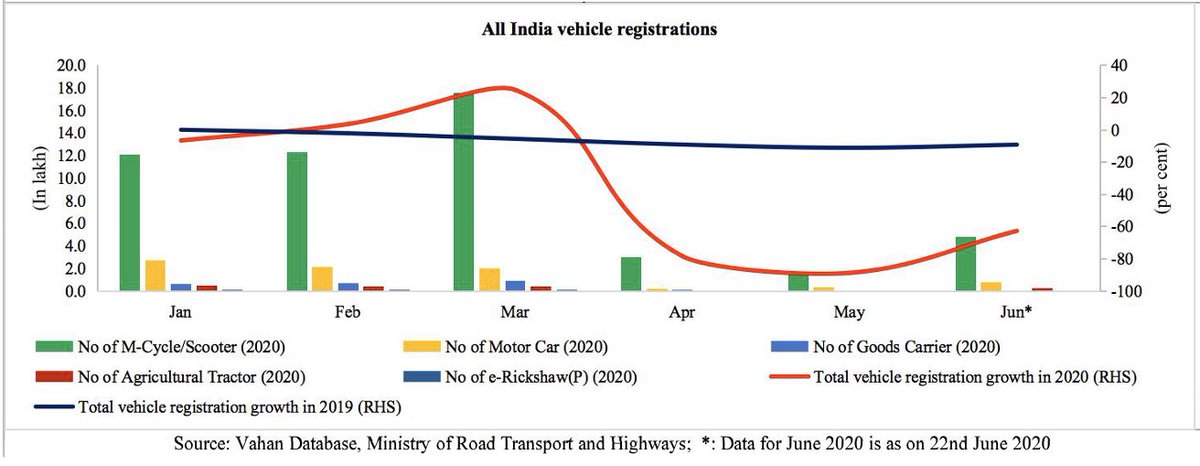

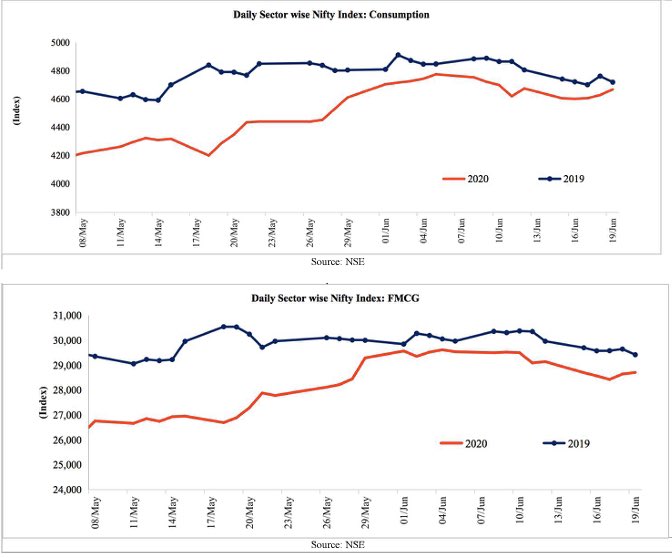

18/n Consumption: Vehicle registrations increased by more than 200% in three weeks of June over May to reach 6.35 lakh,still much lower than pre covid and pre year levels, consumptn and FMCG equities moderated by 0.1% and 1.5% respectively @tulsipriya_rk

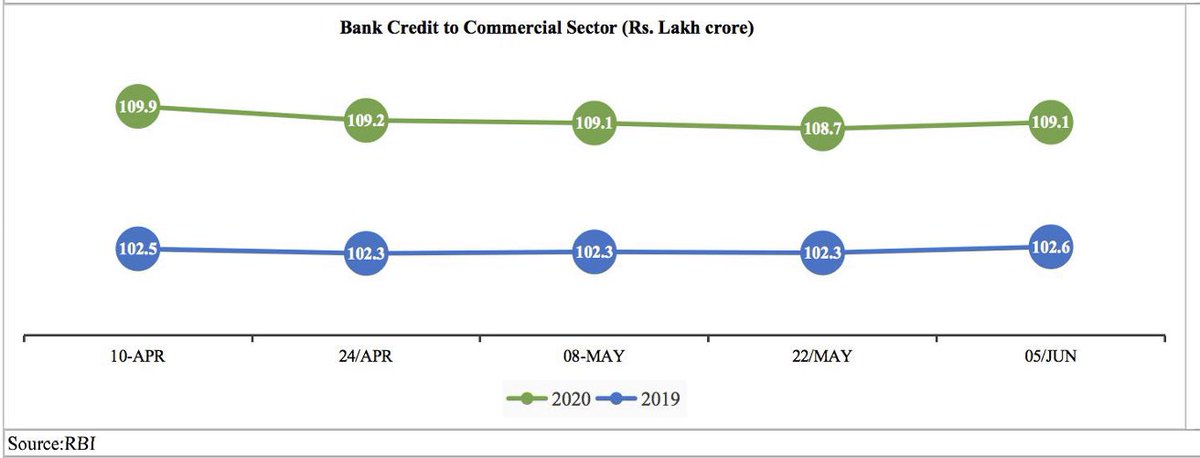

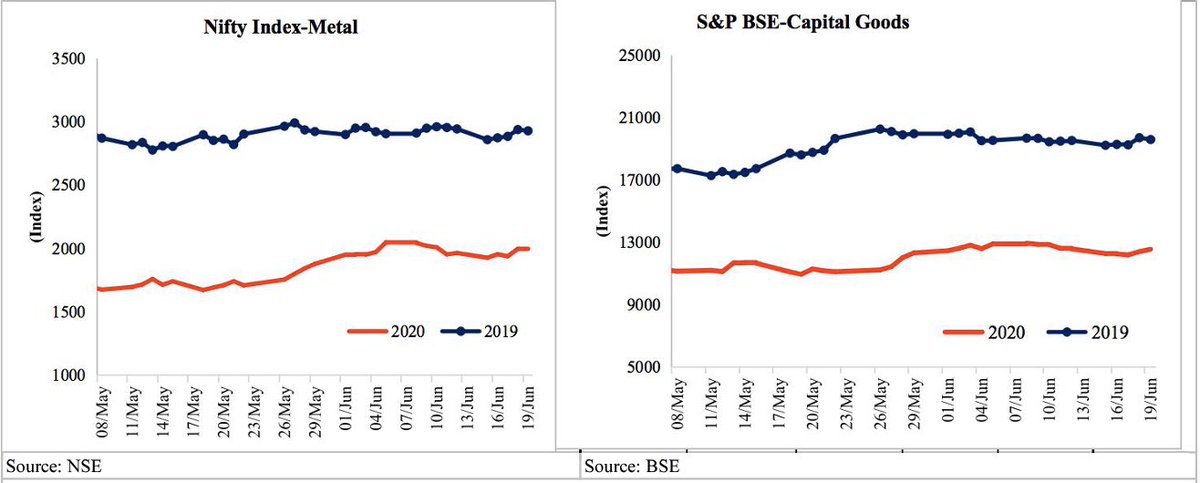

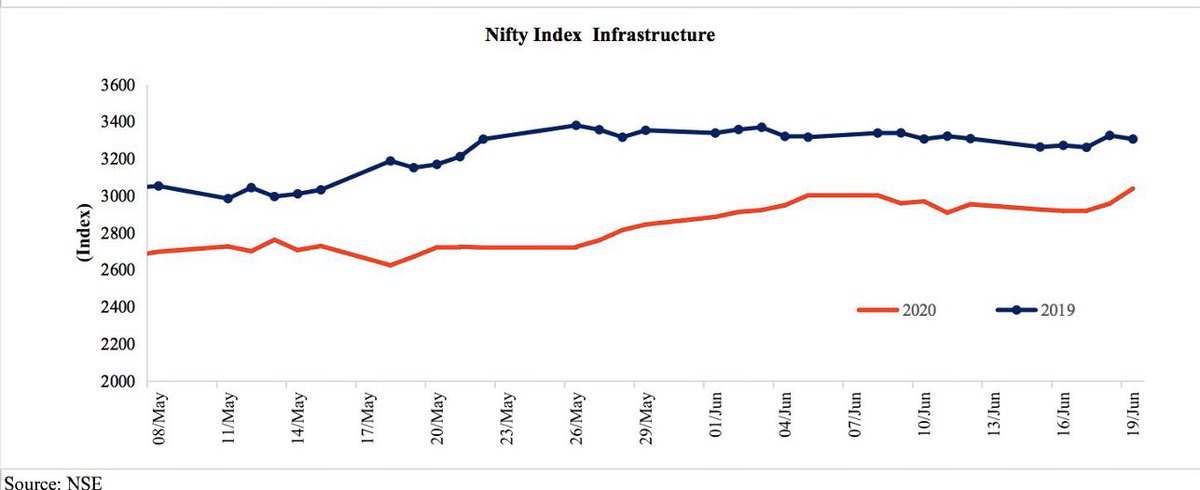

19/n Investment: Growth of bank credit to commercial sector inched up marginally compared to previous fortnight, 6.31% YoY growth, Metal and infra equities gained by 1.6% and 2.9% respectively while capital goods growth marginally declined @tulsipriya_rk

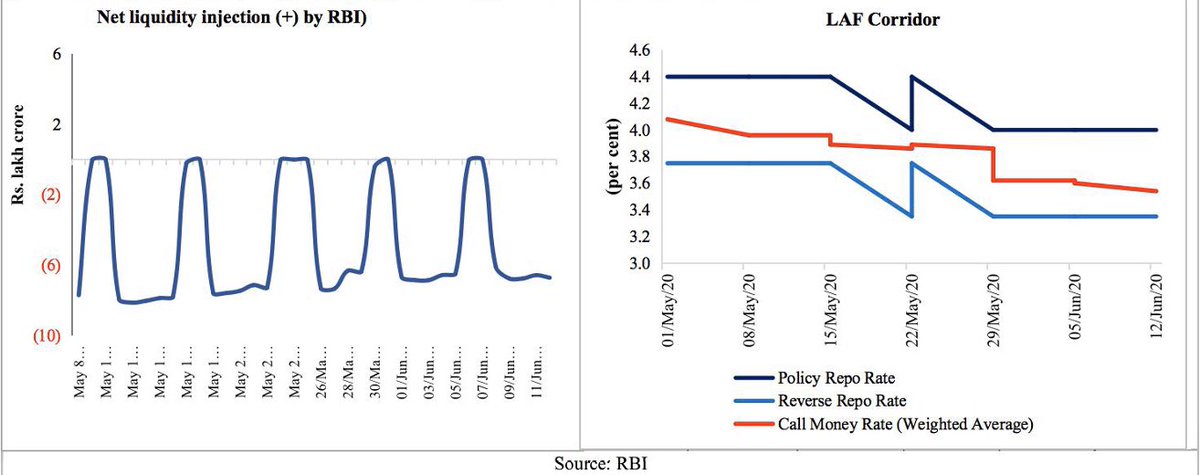

20/9 Monetary: Avg daily net absorption increased to Rs 6.6 lakh crore in the wk ending 12th June, compared to ~Rs 4.0 lakh crore in the previous wk. Low risk appetite.Call money rate fell and stood at 46 bps below repo @tulsipriya_rk

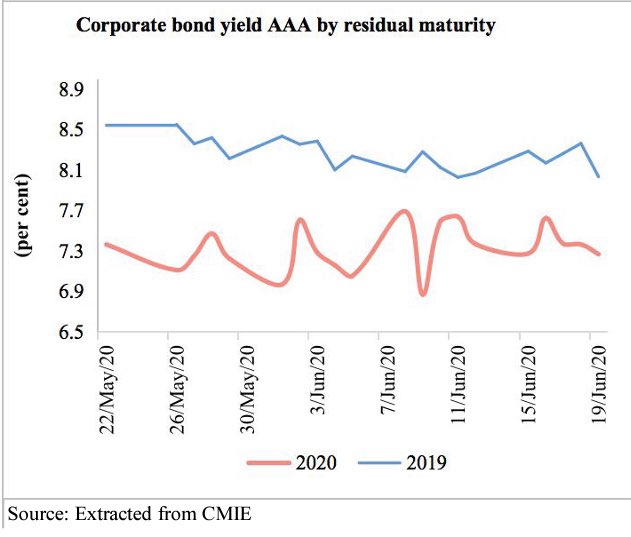

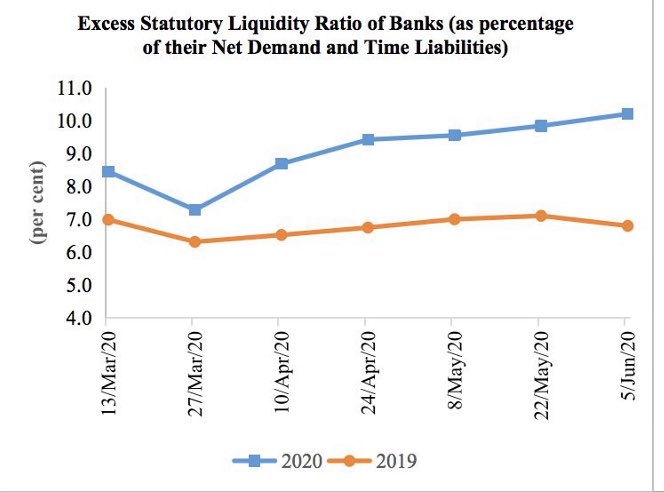

21/9 Corporate bond yield eased to 7.27% in the week gone by. Banks preferred to hold G-Secs with excess SLR increasing to 10.2% (our calc) in the fortnight ending 5 June. @tulsipriya_rk

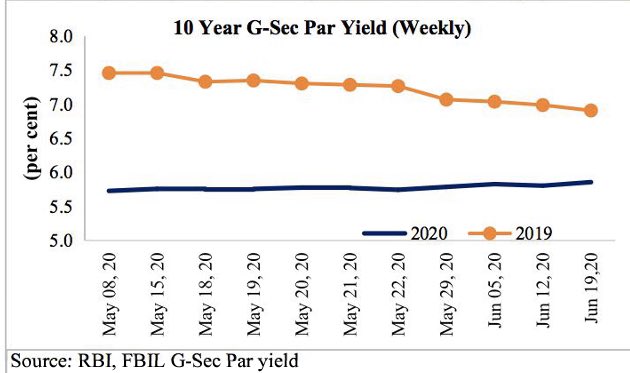

22/9 Fiscal: G-Sec yield rose to 5.86% in the week ending 19th June reflecting saturated gilt market appetite. @tulsipriya_rk

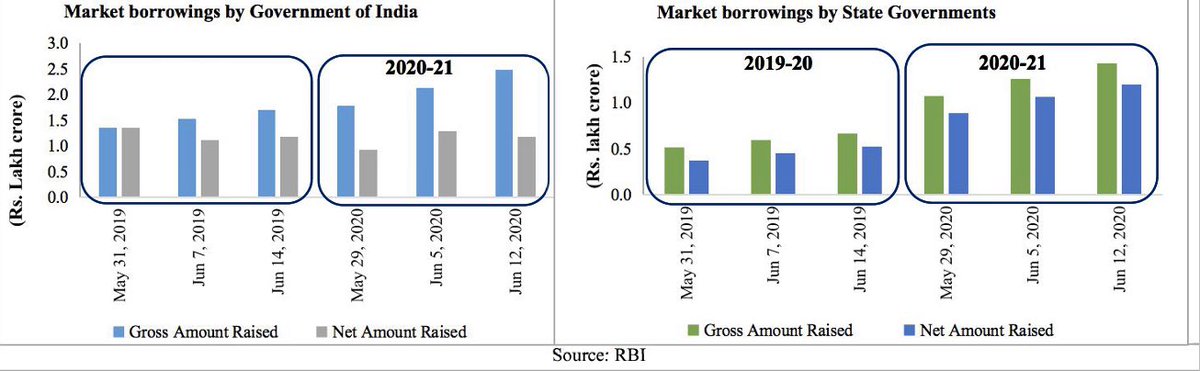

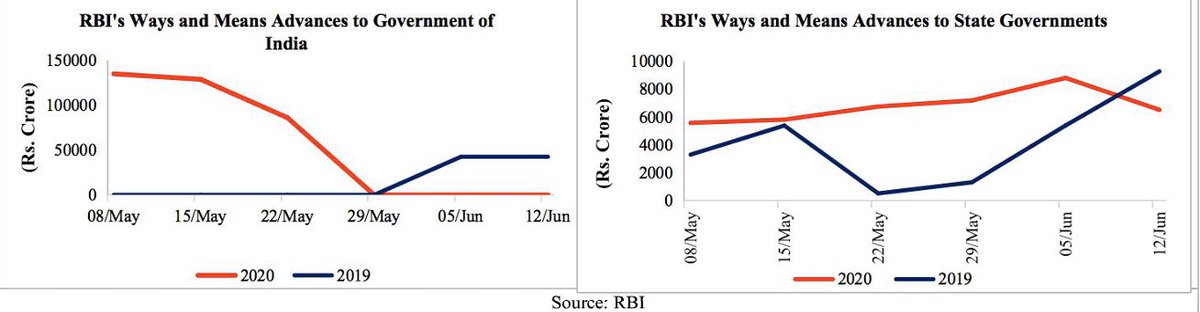

23/9 Centre's gross market borrowings in the wk ending 12th June stood at 1.45 times of last year levels, net borrowings stable. States borrowed more than double, both on gross and net basis, rel. to last year. WMA borrowings of centre 0 and states lower. @tulsipriya_rk

unroll @threadreaderapp