New paper:

Risk Parity: Methods and Measures of Success

investresolve.com/risk-parity-me…

Thanks to the following and others for feedback and edits:

@choffstein

@investingidiocy

@profplum99

@larryswedroe

@maratikus_quant

@Steven_Downey86

An introductory thread:

Risk Parity: Methods and Measures of Success

investresolve.com/risk-parity-me…

Thanks to the following and others for feedback and edits:

@choffstein

@investingidiocy

@profplum99

@larryswedroe

@maratikus_quant

@Steven_Downey86

An introductory thread:

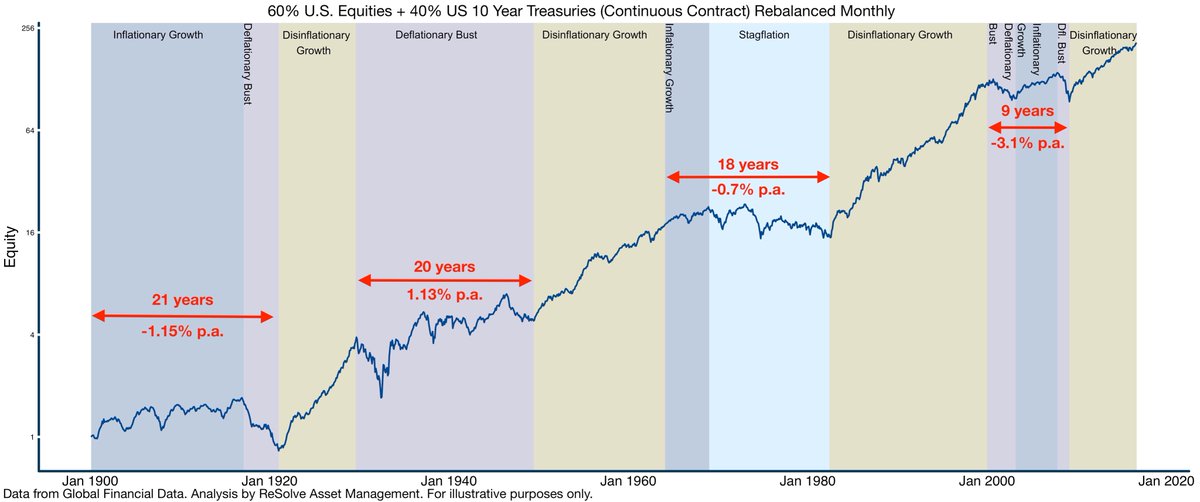

1. Risk Parity (RP) portfolios are designed to achieve reliable investment performance given any trajectory of future growth and inflation shocks. This is in contrast to typical “balanced” stock & bond portfolios like 60/40 which only thrive in periods of disinflationary growth.

2. Many investors are under the misapprehension that RP strategies are typically constructed with levered bonds and stocks. While this construction is more robust than a typical 60/40 portfolio it is NOT a RP strategy, and would be expected to suffer during inflationary shocks.

3. Despite having a weaker long-term premium, adding a commodity sleeve to RP portfolios helps to insulate investors against inflationary shocks. Note how commodities are accretive overall but especially during the inflationary 1970s.

4. This example highlights a critical point: the objective of RP portfolios is to thrive in all sustained market environments. Yet many managers design and clients evaluate Risk Parity strategies on completely different objectives.

5. For example, managers might design RP strategies to maximize common performance metrics, like Sharpe ratios, in simulation. And clients often evaluate strategies based on live performance.

6. These actions represent fundamentally flawed thinking. In fact, if a RP strategy delivers especially strong performance, either in simulation or in live trading, it probably reflects a major bias in the construction.

7. We propose a suite of tools to evaluate RP strategies to complement traditional performance-based metrics. These tools reflect how different RP implementations deliver on the objectives of balance – across markets, asset classes, independent bets, and economic shocks.

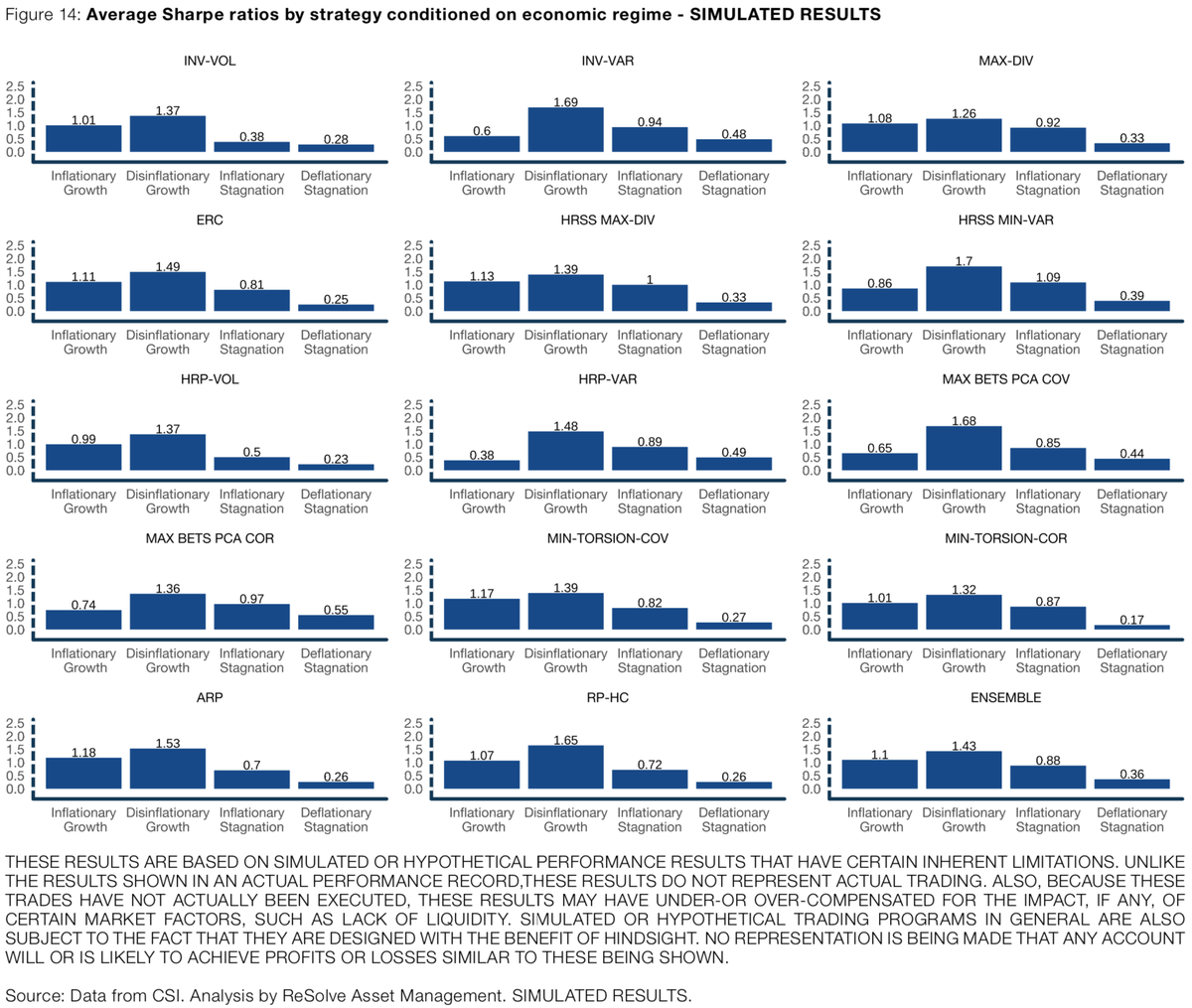

8. RP strategies have delivered strong performance over our simulation horizon from 1985 – 2020. Some methods produced stronger in-sample performance than others. We explore some of the reasons why.

9. Variance-weighted portfolios (like INV-VAR & HRP-VAR) concentrate risk in low-volatility bonds. Since bonds outperformed stocks and commodities over our sample period these methods appear to have an edge.

10. However, variance-weighted methods are poorly balanced in terms of risk as measured by market risk contributions, asset-class based risk contributions, and independent bets.

11. In contrast, other methods exhibit more effective balance, for example across asset-class clusters.

12. Of course, investors’ primary concern should be how RP portfolios perform in response to inflation and growth shocks. The PCA-based methods compare favorably on this metric.

13. RP can extend to other sources of return that behave differently from asset classes. These returns derive from structural and/or behavioural inefficiencies that manifest as “style premia”, “factors” or “edges” that produce returns from different sources at different times.

14. We consider six systematic style-premia strategies expressed on the same diversified futures universe as we employed for our RP analysis.

15. Our proposed Extended RP strategy with style-premia derives about 50 percent of risk from the Ensemble risk parity strategy, and 50 percent from an equal risk allocation across all six systematic strategies.

16. In conclusion, analysis of simulated and/or live performance is not remotely sufficient for the evaluation of Risk Parity strategies. In fact, performance may be misleading if it reflects biased exposure to a certain economic regime.

17. Also, the global risk parity concept may be profoundly enhanced - in terms of long-term performance and resilience to macro-regimes - by the inclusion of uncorrelated alternative style premia sleeves.

@EpsilonTheory I was recalling our podcast chat about your concept of Extreme Agnosticism and the Three Body Problem as I wrote this.

Thanks for the inspiration 🙏🏻

Thanks for the inspiration 🙏🏻