It's a bit out of date (it predates the mandate penalty actually being zeroed out by the GOP), but it's still a good overview:

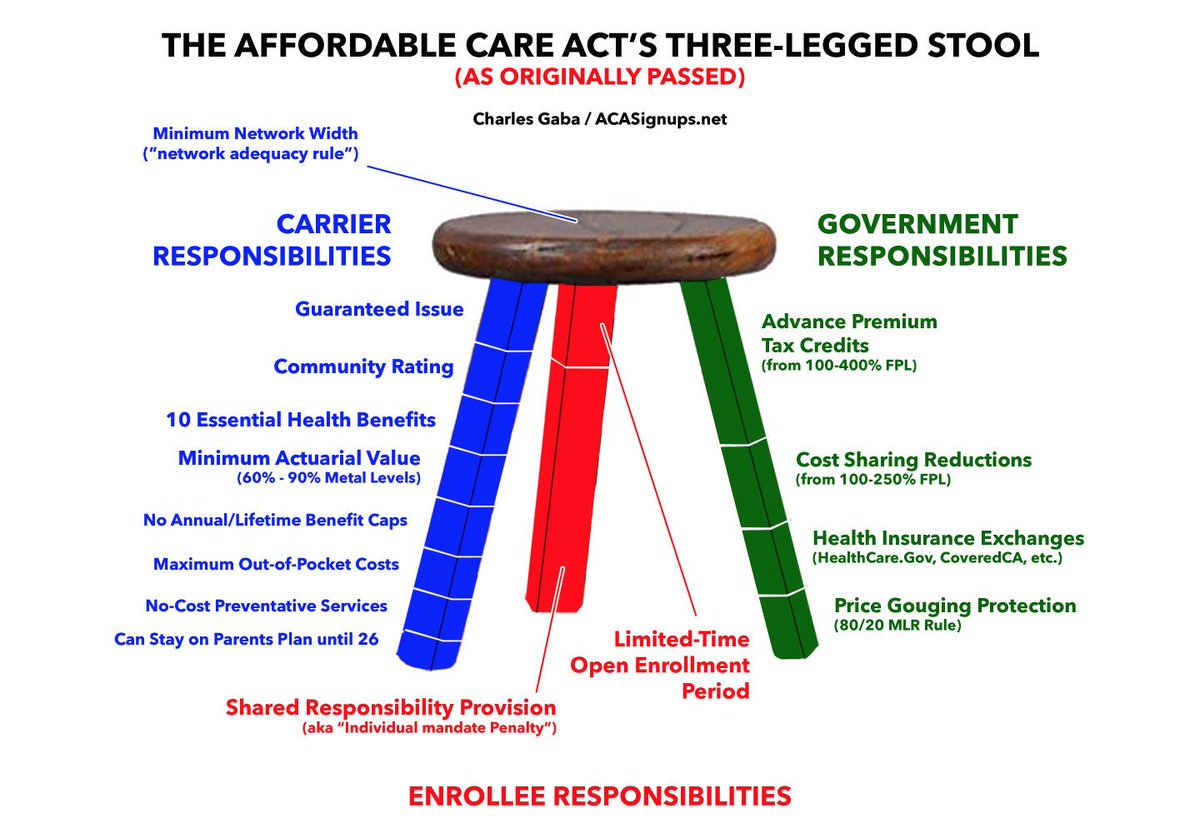

Here's what the #ACA's 3-legged stool was originally supposed to look like. When people talk about "protections for coverage of pre-existing conditions", they're basically talking about the Blue Leg on the left:

There's 8 items listed, but it's really the first three which are the most critical:

--Guaranteed Issue: Carriers must offer policies to ANYONE regardless of health/medical condition/history

--Community Rating: Policy prices can't vary based on health/medical condition/etc.

--Guaranteed Issue: Carriers must offer policies to ANYONE regardless of health/medical condition/history

--Community Rating: Policy prices can't vary based on health/medical condition/etc.

--Essential Health Benefits: Policies must cover a wide range of stuff you'd expect from a major medical policy (hospitalization, surgery, prescription drugs, mental health services, maternity/neonatal care, etc)

Before the ACA, none of this stuff was mandated by federal law.

Before the ACA, none of this stuff was mandated by federal law.

If you're gonna mandate everything in the Blue Leg, that naturally means the cost of the policies is gonna go up. It also means that some people might try to game the system by going w/out coverage until they're actually sick/injured. That's where the Red Leg comes in.

The Red Leg has just 2 parts: The Open Enrollment Period & the Individual Mandate Penalty. With certain exceptions, if you didn't #GetCovered, you'd have to pay a tax to help cover the extra cost you're imposing on others; & you have to do so w/in a certain time window.

For all the controversy re. the Red Leg, it's there for the same reason you can't drive a car w/out auto insurance and you can't get a mortgage without homeowner's insurance: To prevent you from trying to sign up for either one AFTER you crash your car/your house catches on fire.

So, the Blue Leg says carriers must offer DECENT policies to ANYONE, & the Red Leg says that (w/exceptions) pretty much everyone has to enroll or pay a tax. The problem is, the Blue Leg still causes policies to be more expensive than some can afford. Enter the Green Leg.

The Green Leg was supposed to address the affordability portion by offering financial assistance to lower-income enrollees on a sliding scale. There's 2 types of assistance: One for premiums, one for deductibles/co-pays. The Green Leg also includes the healthcare exchanges/etc.

Now, the original 3-legged stool of the ACA *did* have some REAL flaws. The financial assistance wasn't generous enough & cut off too low down the income scale. The mandate penalty was actually too *weak* to be fully effective. And the network requirements were too weak.

The obvious solution to these would have been to beef all of them up (especially the financial assistance): Make the policies more affordable for more people; make the minimum network requirements stronger; and, yes, make the penalty stronger (see Switzerland or Germany).

INSTEAD, the GOP refused to let any of this happen for a solid decade, and the Trump Administration has hacked away at the ACA wherever it can. Here's what the 3-Legged Stool looks like TODAY:

Trump tried to cut off payment of one of the 2 types of financial assistance...but in response, carriers switched to something called #SilverLoading which had the seemingly counterintuitive effect of *increasing* subsidies for many people (but also raising premiums for others).

Trump & the GOP zeroed out the Individual Mandate Penalty, lopping off most of the Red Leg...resulting in avg. premiums increasing about $580/year for every enrollee.

Since most enrollees are subsidized, this means taxpayers are paying ~$5 billion MORE each year to cover that.

Since most enrollees are subsidized, this means taxpayers are paying ~$5 billion MORE each year to cover that.

Of course, if you earn too much to qualify for those subsidies, that means that your premiums are now likely $580/year higher than they would have been otherwise.

Oh, and since the mandate penalty revenue is cut off, that's also several $billion in lost federal tax revenue.

Oh, and since the mandate penalty revenue is cut off, that's also several $billion in lost federal tax revenue.

Zeroing out the federal mandate penalty also had one other effect: It opened up the door for TX Atty. General Ken Paxton (and ~20 other GOP AGs) to file one of the most absurd federal lawsuits ever to make it to the Supreme Court: TX vs. US (aka #TexasFoldEm, aka CA vs. TX).

The logic of the #TexasFoldEm lawsuit is this:

1. The GOP cut off most of the Red Leg.

2. Therefore, the Red Leg is Unconstitutional.

3. Therefore, the rest of the ACA is also Unconstitutional.

4. Therefore, we get to burn the entire stool to the ground.

That's it.

1. The GOP cut off most of the Red Leg.

2. Therefore, the Red Leg is Unconstitutional.

3. Therefore, the rest of the ACA is also Unconstitutional.

4. Therefore, we get to burn the entire stool to the ground.

That's it.

Put another way, their argument is that if you cut someone's leg off with a chainsaw, it means you're allowed to murder them as well.

The Trump Administration, which is supposed to DEFEND the ACA, instead sided with the plaintiffs and specifically called for exactly this.

The Trump Administration, which is supposed to DEFEND the ACA, instead sided with the plaintiffs and specifically called for exactly this.

That brings us to the other day, when Trump surreally claimed that he's signing an executive order to "make insurance companies cover pre-existing conditions"...which the ACA ALREADY DOES, and which TRUMP HIMSELF IS SUING TO HAVE STRUCK DOWN.

And THAT brings me back to @pbump's original tweet at the top: If you ONLY mandate Guaranteed Issue WITHOUT any of the other protections, WITHOUT the financial assistance and WITHOUT the penalty or open enrollment period, it's a recipe for utter disaster.

New York tried doing exactly this in the '90's. @ReedAbelson wrote the definitive piece on this a decade ago: latimes.com/archives/la-xp…

From his *2010* article:

"Since 2001, the average premiums for a health plan on the individual market in New York has nearly tripled, according to the state Insurance Department. In some counties, it is impossible to buy an individual plan for less than $12,000 a year."

"Since 2001, the average premiums for a health plan on the individual market in New York has nearly tripled, according to the state Insurance Department. In some counties, it is impossible to buy an individual plan for less than $12,000 a year."

That would be $14,160/year today, or nearly $1,200/month. Note that this would have been for a policy which DIDN'T necessarily include the coverage mandated by the ACA, either. It presumably would've been for the equivalent of a bare-bones BRONZE plan at best.

By contrast, in June the @HouseDemocrats did exactly what SHOULD have been done years ago by passing #HR1425, which is basically #ACA2.0.

It solves most of the REAL issues with the ACA, while also strengthening/improving protections and other aspects.

acasignups.net/20/06/30/victo…

It solves most of the REAL issues with the ACA, while also strengthening/improving protections and other aspects.

acasignups.net/20/06/30/victo…

And then there's #BidenCare. @JoeBiden's healthcare proposal would be an even stronger version of the House #ACA2.0 bill, PLUS a robust Public Option and a bunch of other important improvements to the system. Here's my write-up on it:

acasignups.net/20/07/23/biden…

acasignups.net/20/07/23/biden…

Oh, one more thing: While zeroing out the mandate penalty did cause premiums to increase by ~$580/enrolled, it DIDN’T cause the entire ACA to collapse...because the financial assistance is still in place to help absorb most of the damage. If you remove THAT as well...collapse.

Again, the GOP’s Texas case claims that cutting off the Red Leg causes the entire stool to collapse...which WOULD be true, except for the World’s Most Expensive Shim effectively replacing it.

Also, even if THAT happened, there would still be no justification for killing the ACA’s Medicaid Expansion provision.

And THAT’S the REAL reason the GOP wants the ENTIRE ACA killed: Tax cuts for the wealthy.

And THAT’S the REAL reason the GOP wants the ENTIRE ACA killed: Tax cuts for the wealthy.

The REAL force driving the GOP to STILL keep trying to kill the ACA isn’t about the blue or red legs...it’s the GREEN leg: Financial assistance (and MedicId expansion funding) are both primarily funded by small surtaxes on the wealthy. They don’t like that, so the law must go.

Here’s an example of how angry they were (and still are) about having to pay a few bucks more so low- and moderate-income people get decent healthcare treatment:

acasignups.net/20/07/06/basta…

acasignups.net/20/07/06/basta…

As an aside: Six states (including California) have reinstated the mandate penalty at the state level instead, which has also helped stabilize the market and mitigate the damage from the federal penalty being zeroed out. That’s the other reason the Texas case is bullshit.

In short: Yes, zeroing the federal penalty out *hurt* the ACA, but it turned out to be a relatively minor injury mitigated by other factors...as evidenced by the fact that ACA exchange enrollment has only dropped slightly since it happened.