1/ .@alexh_johnson asked if I might weigh in on why the CFPB is requesting info on the U.S. consumer credit card market.

Buckle up for a tale of gun-toting senators, people being angry about mail, slow government regulators and Maxine Waters . . .

Buckle up for a tale of gun-toting senators, people being angry about mail, slow government regulators and Maxine Waters . . .

2/ First a brief detour --

Folks are angry due to the horrible incident with Jacob Blake. Regardless of how you feel about BLM or democrats, I bet you do have feelings about people.

I bet we can all agree keeping people alive is good, and US people should have the same rights.

Folks are angry due to the horrible incident with Jacob Blake. Regardless of how you feel about BLM or democrats, I bet you do have feelings about people.

I bet we can all agree keeping people alive is good, and US people should have the same rights.

3/ Almost done -- if you typically dismiss things like BLM, or raise what-about-isms to confirm your views, why not think differently for a few days? Maybe ask how you’d feel if your neighbors and and people that look like you kept getting shot just for doing normal things.

4/ Sorry one more -- if you can’t do this, then ask yourself how you’d respond to the following:

My six year old daughter asked me “why do police shoot so many black people?”

And maybe ask yourself how we can stop this from being a question in the future.

My six year old daughter asked me “why do police shoot so many black people?”

And maybe ask yourself how we can stop this from being a question in the future.

5/ Back to FinTech stuff! Actually way back to the early 2000s. Screechy dial-up modems, multi-colored iMacs and financial services junk mail. Lots and lots of junk mail.

6/ Around this time (@fintechjunkie probably knows when) Capital One pioneered the balance transfer check offer.

You know, the thing where a credit card company mails you some blank checks. You use them, and bingo! You’ve opened a credit card (on purpose or not).

You know, the thing where a credit card company mails you some blank checks. You use them, and bingo! You’ve opened a credit card (on purpose or not).

7/ Capital One built a huge customer base using this easy way to move existing debt. And other card issuers followed suit, with balance checks and all sorts of crazy junk mail offers.

8/ As the card industry was getting bigger and bolder, the typical lobbying games and legislative markers played out. Carolyn Maloney started to introduce bills in the house to rein in the credit card industry. Various senators introduced measures to do the same.

9/ This happened as the Fed Board was trying to use its UDAP powers to just write rules to regulate the industry. A quick tangent on UDAP.

10/ UDAP stands for “unfair or deceptive act or practice.” It goes back to the FTC Act of 1914, and amended a few times including 1938. Congress gave the FTC the power to prohibit commercial activities and practices that were unfair or deceptive.

11/ The banking regulators got this power hooked into their authorizing statutes and it was off to the . . .

federal register to die a . . .

slow . . .

administrative . . .

death.

federal register to die a . . .

slow . . .

administrative . . .

death.

12/ No seriously, the Fed spent ~2 years “studying” the Card industry and proposing various rules to amend Reg AA and Regulations for TILA. They received THOUSANDS of comments. Held ad nauseum hearings. And likely took a few too many unwanted calls from bank lobbyists.

13/ The Fed was bogged down and taking fire from everyone. Consumer advocates were unhappy. Banks were unhappy. Legislators were . . . well, they were raising money and doing other stuff.

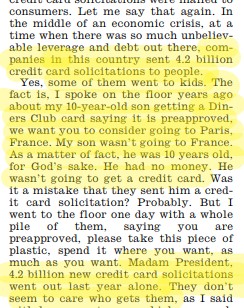

14/ It was all fun, games, profits and a little bankruptcy (just as a treat) until *SOMEBODY* sent a few too many mailers to children and grandchildren of U.S. Senators in the midst of the greatest collapse of credit and equity markets since October 1929.

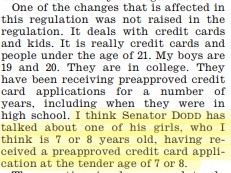

15/ I know I throw a joke or two. Just ask @ohad and his brother @nadavsamet. But this is serious. Credit card companies were sending pre-approved card offers to 10 year old kids who happened to be . . . children of U.S. senators.

16/ It was the tipping point. Consumer advocates + members who thought the Fed was moving too slowly + the 2008 recession + angry parents/grandparents proved to be too much for the banking industry. In 2009, the Credit Card Accountability and Responsibility Disclosure Act passed.

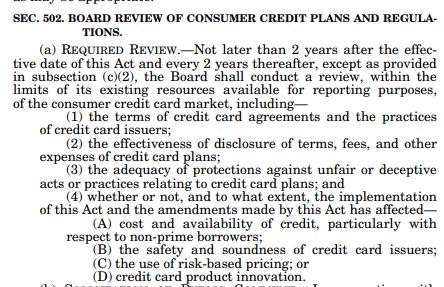

17/ The law has a study component - Section 502 - that requires the authorized agency (formerly the Fed Board, now the CFPB) to publish a study of the credit card markets. They have to do this every two years.

18/ Studies are a legislative tactic for one side to explore an idea they want in the law but can’t get enough votes to pass. E.g., a study on usury rates. Some want rates capped at 36% annually. If they can’t pass it in the next Dem administration, you can bet there’s a study.

19/ Other study requirements are used as a compromise to water down something seen as too extreme. If some requirement has enough votes to pass, one political party might peel some votes away and swap the language with a requirement to “study” the impact of the proposed law.

20/ The CARD Act study is this latter form. Conservative members (including some Dems) saw that they couldn’t kill the law, so they forced the study to give regulators tools to surface “unintended consequences” that could support future laws to cancel some of the CARD Act.

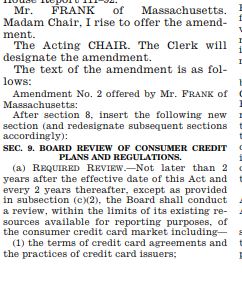

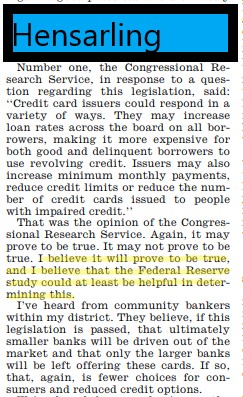

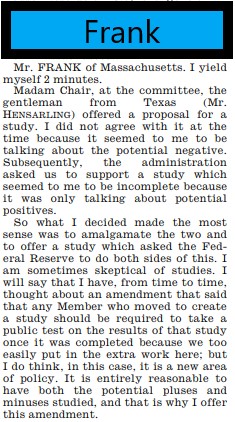

21/ Barney Frank and Jeb Hensarling discussed the study requirement on the House floor. Both supported it, but for different reasons.

22/ Frank says that initially he saw the GOP’s study amendment as a negative tactic to lay the groundwork to later overturn the bill and was opposed. But then the Obama Administration asked them to include a study.

23/ So to answer @alexh_johnson ‘s question, the CFPB has requested information to fulfill its statutory requirement to publish a study of the U.S. card markets in 2021.

But there’s a twist on this year's request for information . . .

But there’s a twist on this year's request for information . . .

24/ The CFPB Request for Information or RFI says it serves a dual purpose. It’s not well spelled out, but the Bureau seems to be asking for comments on what parts of the CARD Act don’t work for smaller enterprises.

They’re asking what parts of the rules should be repealed.

They’re asking what parts of the rules should be repealed.

25/ FWIW, I don’t think the CFPB will actually repeal any of the CARD Act regs, found as part of Regulation Z (12 C.F.R. 1026.5-16 and 1026.51-61).

The statute and regs seem too intertwined, and anything they try to remove will ultimately be backstopped by the statute.

The statute and regs seem too intertwined, and anything they try to remove will ultimately be backstopped by the statute.

26/ There’s also a timing element. Assuming Joe Biden wins the Presidency, there will be shift at the CFPB and folks won’t be directed to find ways to water down Reg Z.

27/ The CARD Act is near and dear to my heart, in large part because I can’t seem to get away from it.

28/ In 2009, I was laid off from my law firm and found a job working for Maxine Waters. My first substantive task was to write her a speech in support of the CARD Act.

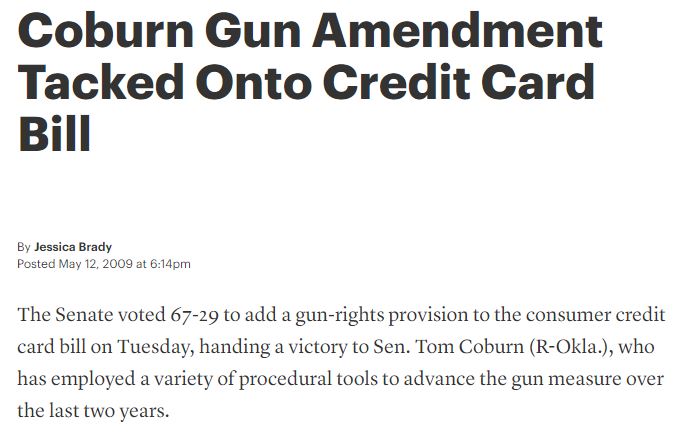

29/ The CARD Act has some great quirks in it. Sen. Tom Coburn pulled a stunt to add language that allowed guns in national parks. It worked!

I assume it was spurred on by Coburn’s love of Warren Zevon. The next few weeks, lawyers argued over guns and money.

I assume it was spurred on by Coburn’s love of Warren Zevon. The next few weeks, lawyers argued over guns and money.

30/ Coburn was able to pull it off due to a procedural difference in the Senate.

In the House, things must relate or be “germane” to be a valid amendment.

There’s no germaneness requirement in the Senate, so Senators can stick all sorts of wacky things into must-pass bills.

In the House, things must relate or be “germane” to be a valid amendment.

There’s no germaneness requirement in the Senate, so Senators can stick all sorts of wacky things into must-pass bills.

31/ Side tangent - this is how Round 4 of PPP will get passed. It'll be attached to some spending bill for something like the Department of Agriculture, likely by Marco Rubio.

(I'm for this, btw - SMBs are hurting and need the help)

(I'm for this, btw - SMBs are hurting and need the help)

32/ The CARD Act had enough votes to for sure pass. But expanded gun rights - here, carrying into national parks - didn’t have enough votes to be stripped out.

Moderate Dems and GOP members combined to make it a thing. The Tea Party would eat most of those Dem seats in 2010.

Moderate Dems and GOP members combined to make it a thing. The Tea Party would eat most of those Dem seats in 2010.

33/ I’d later go to Capital One. I didn’t work on CARD Act implementation, but it was a massive project for our attorneys and compliance folks. Heard about its progress in lots of team meetings.

34/ My next stop was the law firm of Morrison Foerster (MoFo!). I’d spend the next few years writing comment letters on behalf of bank and network clients, and also providing advice on dispute resolution, change-in-terms and ability-to-pay requirements.

media.mofo.com/files/uploads/…

media.mofo.com/files/uploads/…

35/ I’ve since gotten various questions about whether Reg Z applies to this or that product, usually from folks that know enough that it exists, but forget the quirks on how it applies to commercial offerings. Hint - check 12 CFR 1026.12.

36/ For those of you building in the revolving credit space, you’ll definitely want to give the CFPB’s biannual reports a read. They give great snapshots of the U.S. market, and summarize interesting trends. Here’s the 2019 report.

files.consumerfinance.gov/f/documents/cf…

files.consumerfinance.gov/f/documents/cf…

37/ The last report highlights delinquency rates were trending up for the first time since the 2008 recession. Total cost of credit also increasing, despite rock-bottom Fed rates. Will be interesting to see how this compares in 2021, given the likely K-shaped COVID recovery.