“The Politics of Bad Options. Why the Eurozone’s problems have been so hard to resolve”, co-authored with @ariray and @niredeker, is out at @OUPPolitics.

As promised, here is a thread on what it is about:

global.oup.com/academic/produ…

As promised, here is a thread on what it is about:

global.oup.com/academic/produ…

Why was the Euro crisis so hard to resolve? Why were crisis resolution cost so unequally distributed? Why did no country leave the euro? And who supported and opposed different policy options domestically?

Our book sets out to answer these questions.

Our book sets out to answer these questions.

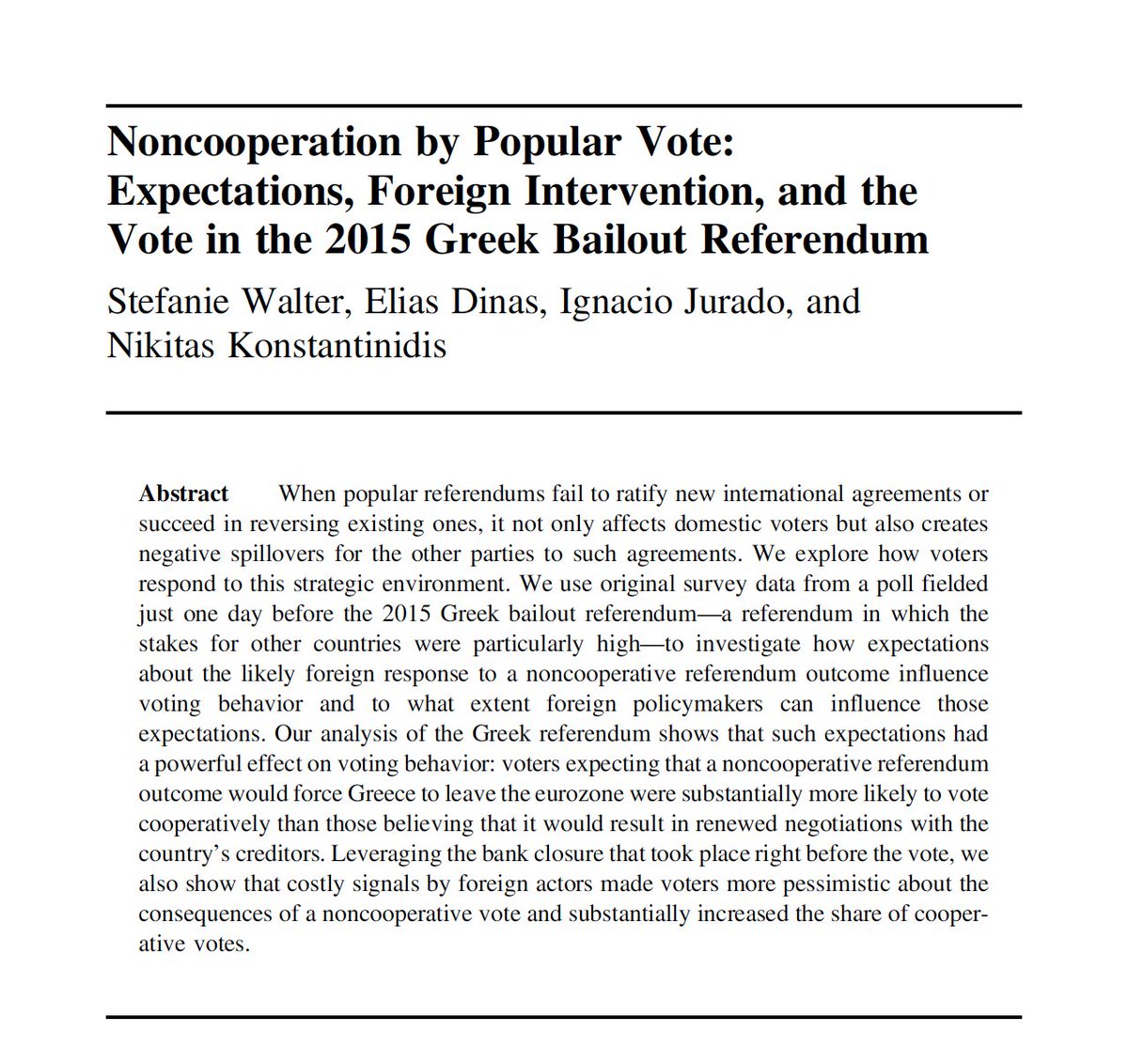

To this end we study the crisis in both deficit-debtor and surplus-creditor countries and consider distributive concerns associated with all policy options, including those that were not chosen: external adjustment, internal adjustment, and financing.

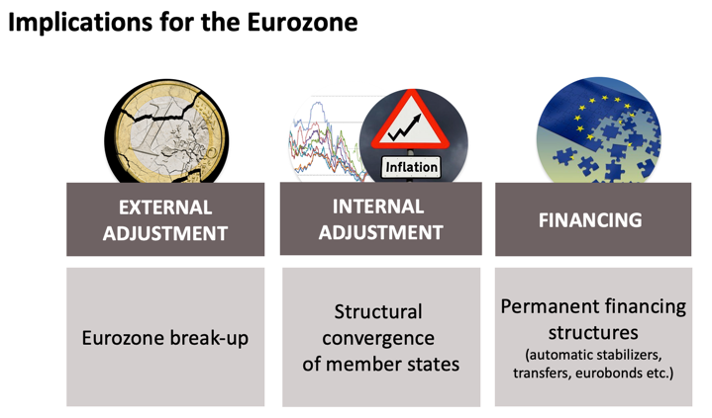

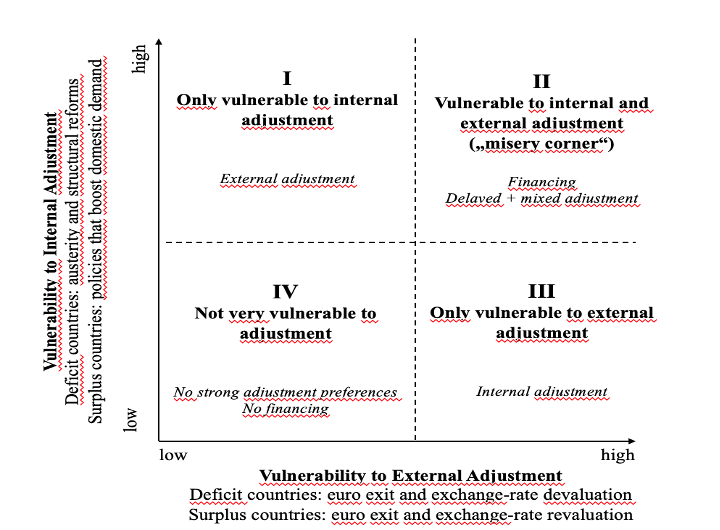

Countries, groups, and individuals differ in the extent to which they are vulnerable to each of these options.

Their vulnerability profiles and the trade-offs they represent influence crisis politics both within countries and at the international level.

Their vulnerability profiles and the trade-offs they represent influence crisis politics both within countries and at the international level.

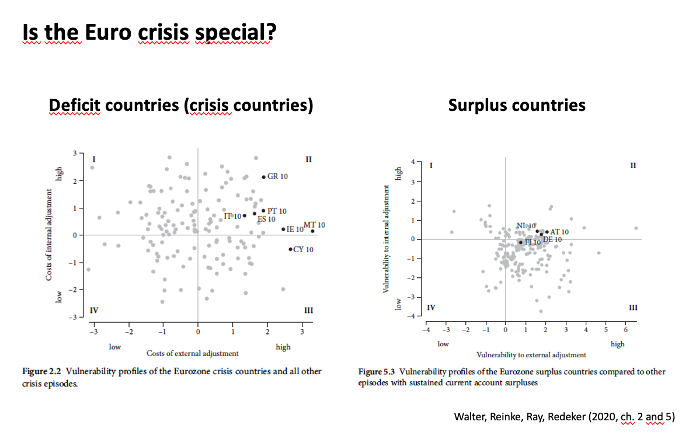

[What would a political economy book be without a 2x2?]

Crisis resolution is most difficult in the "misery corner", where vulnerability to both internal and external adjustment is high.

We expect political conflict, delay, and a higher willingness to finance rather than rebalance here.

We expect political conflict, delay, and a higher willingness to finance rather than rebalance here.

We test our argument by comparing country-level vulnerability profiles in the Euro crisis with those of previous crises, analysing survey data from 700 interest groups about their policy preferences, and conducting case studies of Eurozone crisis politics.

Comparing aggregate, country-level vulnerability profiles in crisis/surplus episodes (122 countries, 1990-2014), we find most Eurozone countries were located in the “misery corner”, where crisis resolution is politically difficult and burden sharing is unlikely.

The Eurozone crisis is thus unusual, but our analysis underscores that it is not completely distinct from other balance-of-payments and debt crises.

(see also this special issue with @mcopelov and @jafrieden)

journals.sagepub.com/doi/abs/10.117…

(see also this special issue with @mcopelov and @jafrieden)

journals.sagepub.com/doi/abs/10.117…

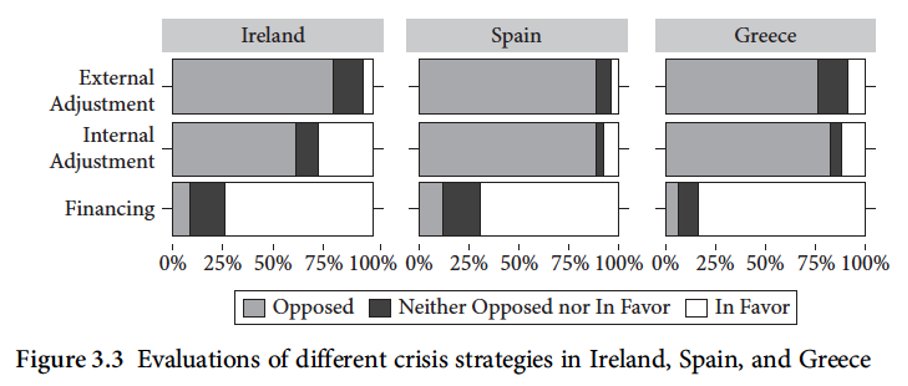

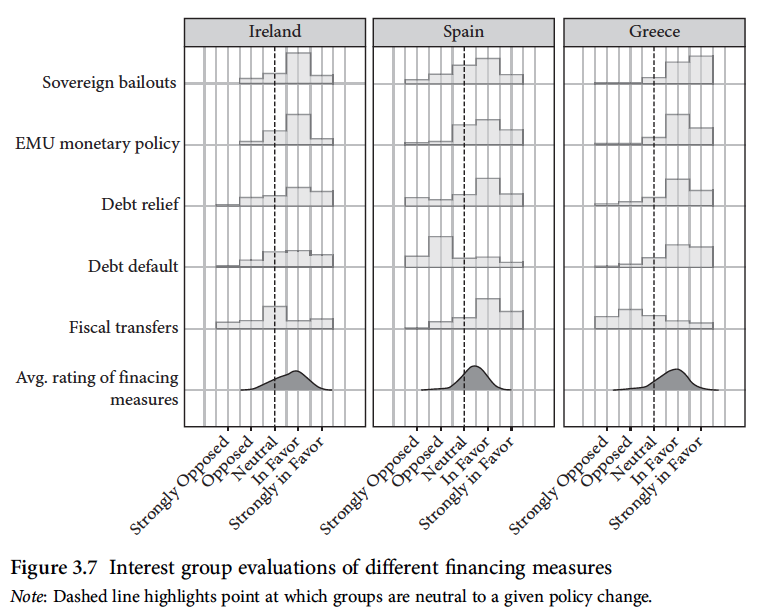

To study within-country conflicts about crisis resolution, we surveyed about 700 socioeconomic interest groups in a) Greece, Ireland, and Spain and b) Austria, Germany and the Netherlands, and interviewed 47 interest group representatives and policymakers in these countries.

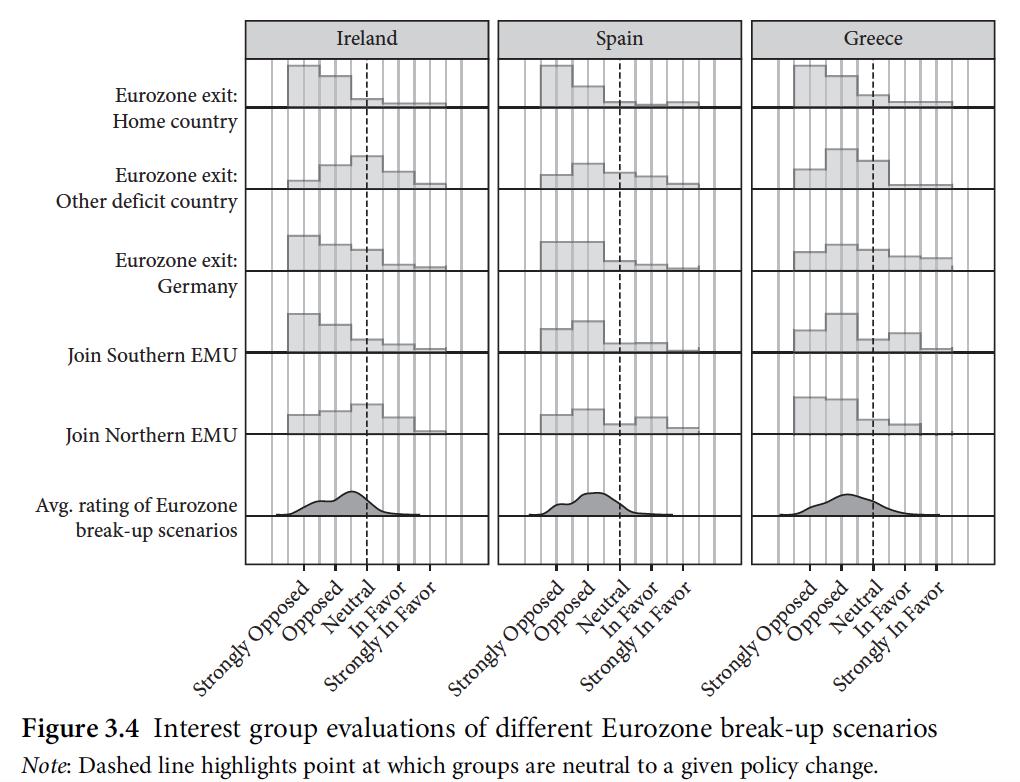

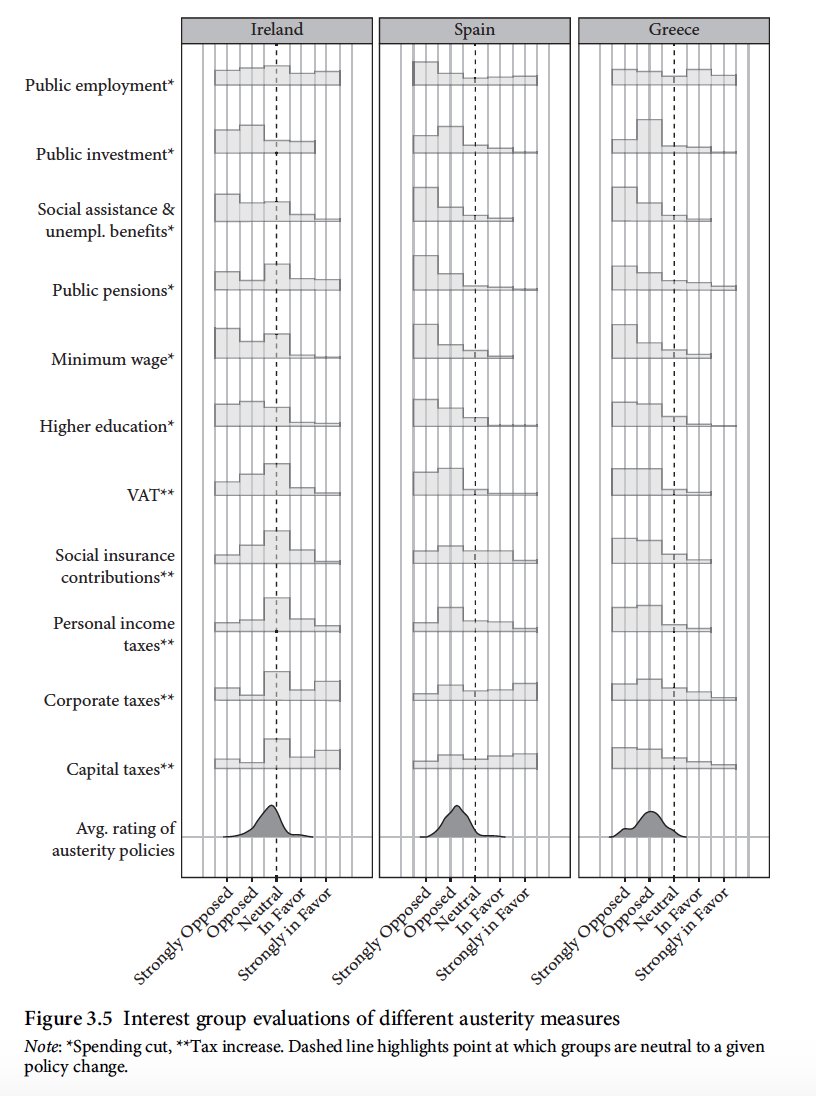

Interest groups in deficit-debtor countries opposed both internal and external adjustment, but were more positive about financing. When pressed to choose, those in the misery corner prefer austerity over euro exit.

… but these preferences are policy-specific, and evaluations of different policies vary widely, both across countries and across interest groups.

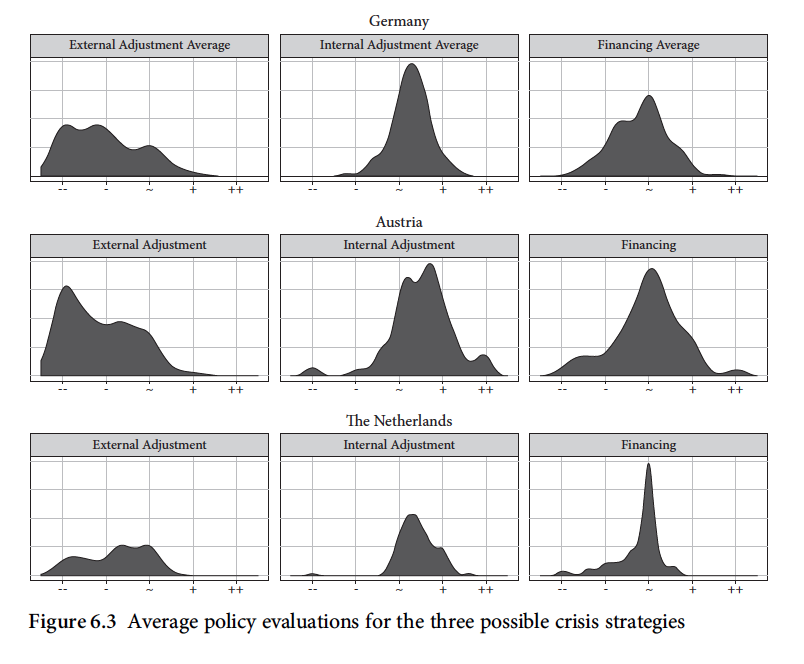

Surplus-creditor country interest groups had very similar preference structures. They opposed a break-up of the Eurozone (external adjustment), were rather indifferent about financing, and, perhaps surprisingly, and evaluated internal adjustment somewhat positively.

Contrary to the common perception about the „frugal North“, we find no general opposition to internal rebalancing: interest groups assessed internal adjustment rather positively overall.

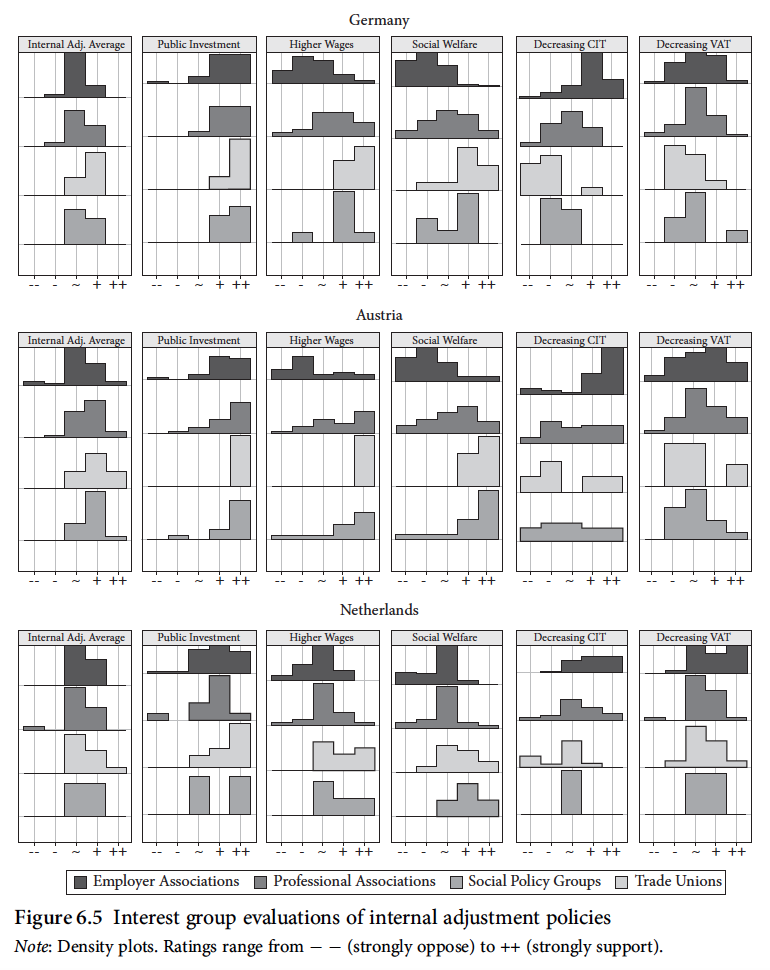

However, they differed considerably in HOW rebalancing should be achieved.

However, they differed considerably in HOW rebalancing should be achieved.

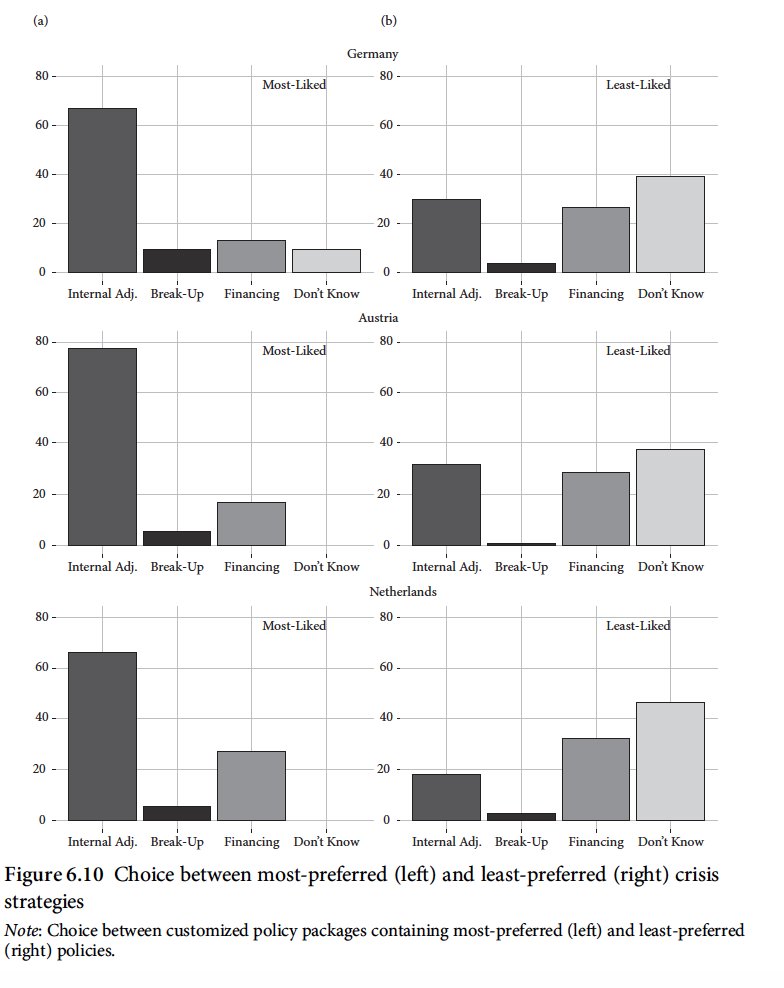

This policy-specific support for internal adjustment matters, because there is much less support for rebalancing when we ask interest groups to choose between the policies they dislike most.

But: A choice between bad options also increases support for financing.

But: A choice between bad options also increases support for financing.

But if surplus-creditor interest groups were not opposed to internal adjustment, why did so little rebalancing happen?

Because governments had few political incentives to pursue it:

Polarization meant that there was no strong societal push for any one rebalancing policy. Key policymakers opposed rebalancing for ideological reasons. And policy alternatives existed - let others to the adjusting.

Polarization meant that there was no strong societal push for any one rebalancing policy. Key policymakers opposed rebalancing for ideological reasons. And policy alternatives existed - let others to the adjusting.

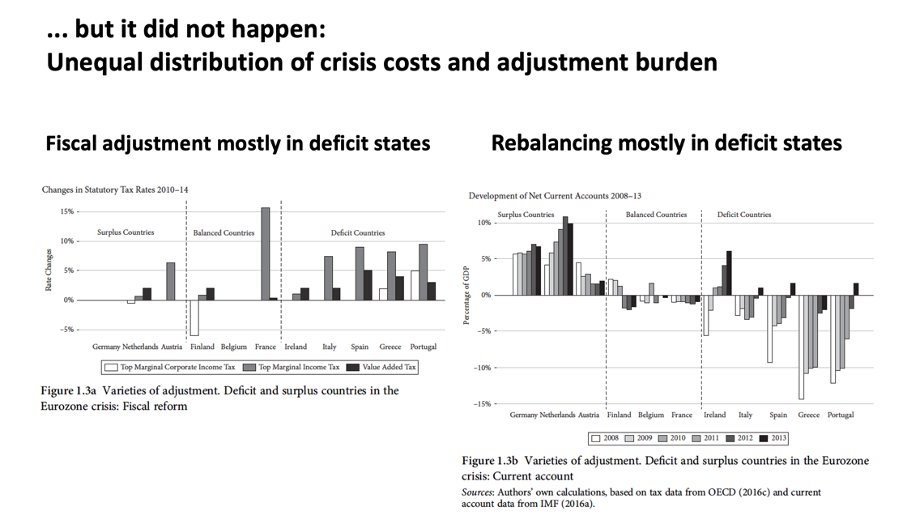

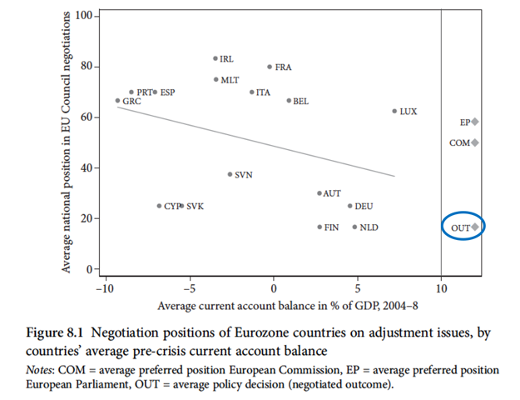

On the European level, policy proposals concerning the distribution of the adjustment burden were mostly decided in line with surplus country preferences. An example are bailouts liked to strong conditionality that forced deficit-debtor countries to adjust.

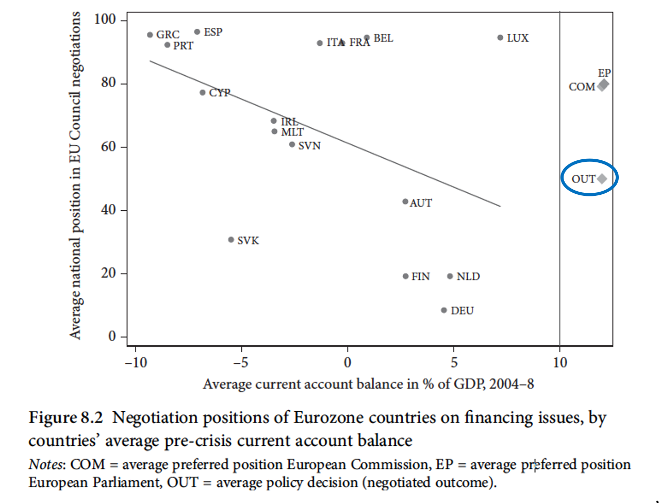

Surplus-creditor countries were much more willing to make concessions with regard to financing:

In sum, our book shows that in the Euro crisis, countries’ vulnerability profiles clustered in the “misery corner”, where any type of adjustment is costly – all options are bad. When we consider these bad alternatives, the unusual euro crisis trajectory becomes less puzzling.

• • •

Missing some Tweet in this thread? You can try to

force a refresh