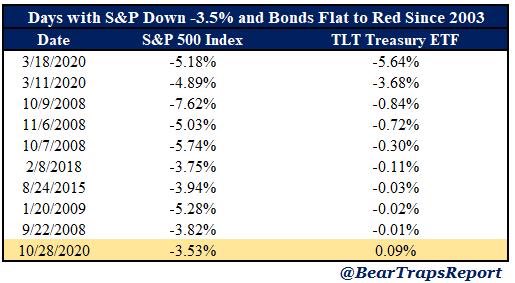

The Next Bitcoin Mania is Here...

The main thesis (explained in the thread below) has been that rising institutional demand coupled with an already-tiny float will catapult Bitcoin higher in the short to medium term.

Brief update.👇

The main thesis (explained in the thread below) has been that rising institutional demand coupled with an already-tiny float will catapult Bitcoin higher in the short to medium term.

Brief update.👇

https://twitter.com/bvddycorleone/status/1316441107308457984

Let’s run through all the Old Guards of Wall Street who’ve recently morphed into Bitcoin advocates...

First up, we got George Ball, ex-Prudential CEO, coming out in favour of Bitcoin on Aug 14:

reuters.com/video/watch/id…

First up, we got George Ball, ex-Prudential CEO, coming out in favour of Bitcoin on Aug 14:

reuters.com/video/watch/id…

Next, we got the legendary Paul Tudor Jones, declaring that “it’s like investing early in a tech company” on Oct 22:

coindesk.com/paypal-paul-tu…

coindesk.com/paypal-paul-tu…

Then, we got none other than the man himself, Stan Druckenmiller, telling us on Nov 9 that “if the gold bet works, the Bitcoin bet will probably work better because it’s thinner and has a lot more beta to it.”

https://twitter.com/lashercorson/status/1325872804714180610

This week, we had Ray Dalio come out and admit that he “might be missing something” about Bitcoin (what he’s missing is 165% YTD return...)

bloomberg.com/news/articles/…

bloomberg.com/news/articles/…

This morning, Blackrock’s CIO for fixed income, Rick Reider, noted that he thinks Bitcoin is “here to stay”...

seekingalpha.com/news/3638337-b…

seekingalpha.com/news/3638337-b…

With all these influential Old Guards coming out in favour, everyone’s gonna need some Bitcoin. Most allocators will eventually capitulate to at least a small Bitcoin allocation.

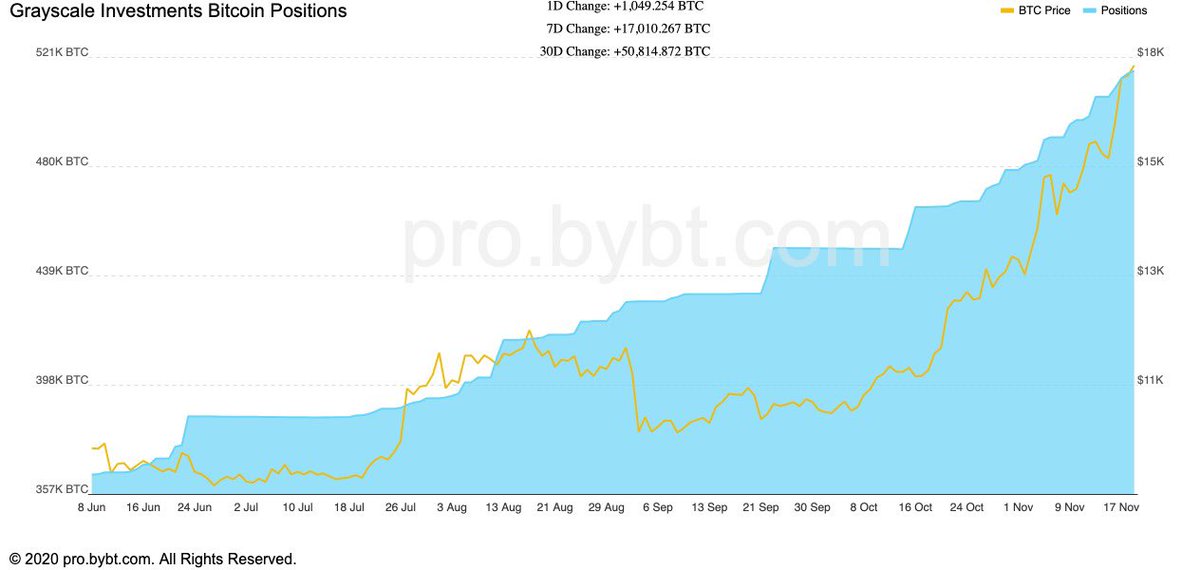

And let’s not forget the monster that is $GBTC, which continues to corner the float at astounding speed, gobbling up around 120,000 coins since mid October... and collecting 2% management fees...

And, if Google Search Trends mean anything, we could just be in the very early innings of this Mania...

https://twitter.com/ronstoeferle/status/1329816091082813444

All that said, Bitcoin is, as we well know, extremely volatile.

It’s up 65% since I wrote that it was “On the Precipice of Another Mania” on Oct 14, but it could easily give back those gains before rocketing past its previous all-time high.

It’s up 65% since I wrote that it was “On the Precipice of Another Mania” on Oct 14, but it could easily give back those gains before rocketing past its previous all-time high.

If you think Bitcoin is the future and the answer to all our monetary woes, I wish you luck.

If you think Bitcoin is a giant Ponzi scheme, then I urge you to channel your inner Soros and hop in regardless: “When I see a bubble forming, I rush to buy, adding fuel to the fire.”

If you think Bitcoin is a giant Ponzi scheme, then I urge you to channel your inner Soros and hop in regardless: “When I see a bubble forming, I rush to buy, adding fuel to the fire.”

• • •

Missing some Tweet in this thread? You can try to

force a refresh