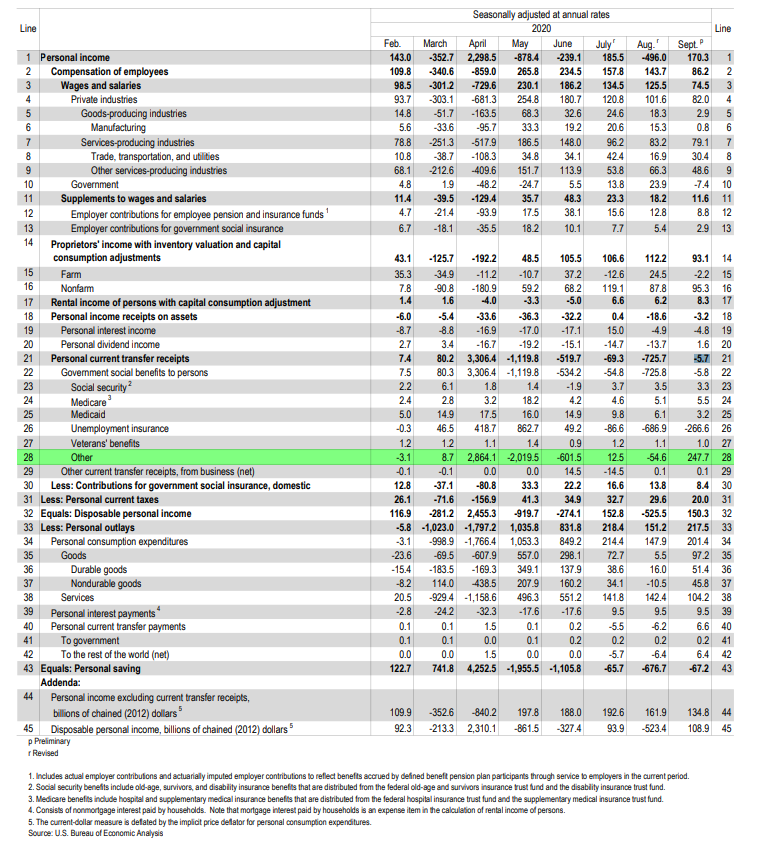

GDP growth is in a cyclical upturn, but structural issues still exist.

Today's GDP report reminded us that debt-financed consumption policies have consequences.

Government borrowing = domestic savings + inflows of foreign capital - domestic investment.

1/n

Today's GDP report reminded us that debt-financed consumption policies have consequences.

Government borrowing = domestic savings + inflows of foreign capital - domestic investment.

1/n

If government borrowing is increasing then domestic savings need to rise, inflows of capital need to rise or domestic investment needs to fall.

Net national savings is negative and barely recovered despite the +33% GDP print.

2/n

Net national savings is negative and barely recovered despite the +33% GDP print.

2/n

It is true that foreign holdings of Treasury bonds as a % of the total has been declining.

3/n

3/n

https://twitter.com/tracyalloway/status/1331385346106351617?s=20

But that means private domestic investment is the leg that takes the fall.

That is exactly what has been happening and it accelerated in Q3, even with the positive GDP print

If we use debt to force consumption, we're making a choice to forego other parts of the economy

4/n

That is exactly what has been happening and it accelerated in Q3, even with the positive GDP print

If we use debt to force consumption, we're making a choice to forego other parts of the economy

4/n

Private investment in structures and equipment was over 13% of GDP in 1980.

There has been a trend of lower highs and lower lows in terms of investment in structures and equipment as a % of GDP.

5/n

There has been a trend of lower highs and lower lows in terms of investment in structures and equipment as a % of GDP.

5/n

Investment in structures and equipment includes things like hospitals, power plants, manufacturing plants, industrial supplies, transportation equipment, construction machinery, and more.

apps.bea.gov/national/FA200…

apps.bea.gov/national/FA200…

6/n

apps.bea.gov/national/FA200…

apps.bea.gov/national/FA200…

6/n

Investing less in these areas will continue to hinder productivity growth

With declining population growth we need to get productivity growth higher to break out of our stagnation

We should look at cyclical upturns in growth + inflation separately from these secular trends

7/7

With declining population growth we need to get productivity growth higher to break out of our stagnation

We should look at cyclical upturns in growth + inflation separately from these secular trends

7/7

• • •

Missing some Tweet in this thread? You can try to

force a refresh