Ltts concall was today at 8:30 pm

" LTTS has emerged as largest pureplay engineering services company in India"

@ParveenBhansali @saketreddy @AvinashGoraksha @safiranand @abhymurarka

Here are the key takeaways 😀

🧵👇

" LTTS has emerged as largest pureplay engineering services company in India"

@ParveenBhansali @saketreddy @AvinashGoraksha @safiranand @abhymurarka

Here are the key takeaways 😀

🧵👇

Overview

-Revenue grew by 6% QoQ with broad-based growth across all the segments.

- Improvement was driven by combination of higher utilization, improvement in offshore revenue mix.

- Segmental margin improvement also saw improvement across the board.

-Revenue grew by 6% QoQ with broad-based growth across all the segments.

- Improvement was driven by combination of higher utilization, improvement in offshore revenue mix.

- Segmental margin improvement also saw improvement across the board.

- Industrial products, plant engineering and telecom & Hi-tech grew in access of 5%

- Sequential margin improvement from Q2 to Q4.

- Free cashflow generation continues to be robust

- Sequential margin improvement from Q2 to Q4.

- Free cashflow generation continues to be robust

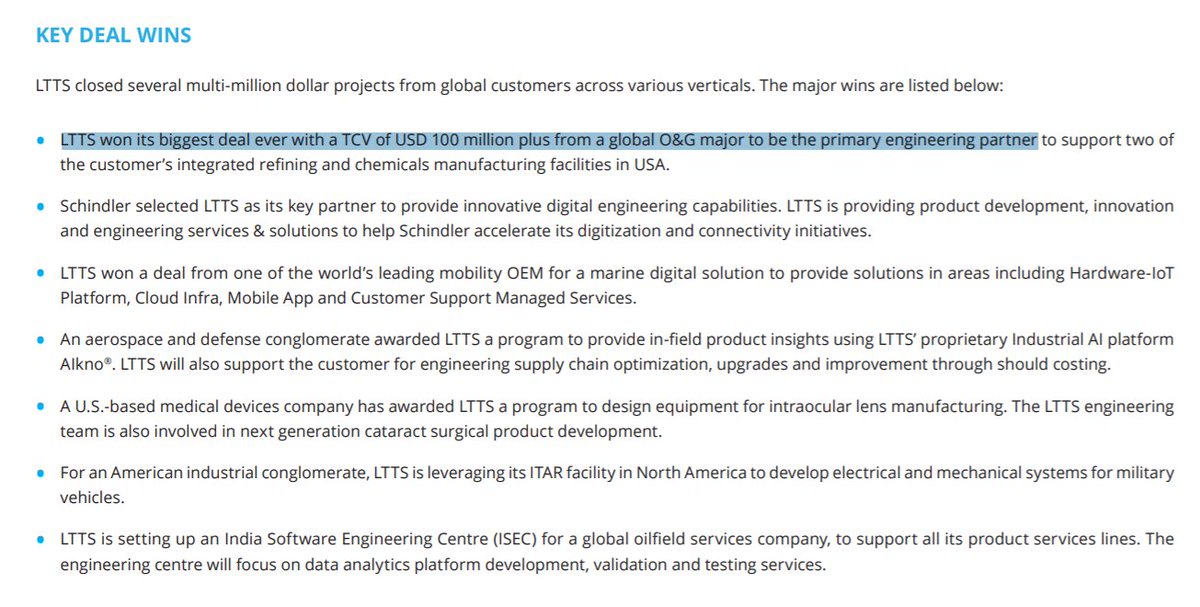

- Last quarter LTTS won its biggest deal ever with a TCV of USD 100 million plus from a global O&G major to be the primary engineering partner.

- Deal pipeline is healthy.

- LTTS is the leader in Digital Engineering, IoT & AI which forms the backbone of new product development

- Deal pipeline is healthy.

- LTTS is the leader in Digital Engineering, IoT & AI which forms the backbone of new product development

Verticles

1) Transportation:

- Sequential growth 3.1%.

- Outlook in commercial auto is still challenged, the company see consolidation and product software opportunity.

- Spending continues to rise in electric, autonomous, and connected vehicle space.

1) Transportation:

- Sequential growth 3.1%.

- Outlook in commercial auto is still challenged, the company see consolidation and product software opportunity.

- Spending continues to rise in electric, autonomous, and connected vehicle space.

- Company won 3 deals greater than 10 millions dollars. Company see multiple deals in the pipeline in autonomous and EV space

2) Telecom & Hi-tech

- Organic growth 3.7%

- Opportunity continues to be in localization and electrification.

2) Telecom & Hi-tech

- Organic growth 3.7%

- Opportunity continues to be in localization and electrification.

- In Semiconductor, company is seeing deal improvement towards new generation chips which gives opportunity in design chip verification.

- Company is participating network virtualization in 5g activities.

- Company is participating network virtualization in 5g activities.

3) Plant engineering

- Good quarter with 9.2% qoq.

- In FMCG & chemicals company see projects related to brownfield expansion and low cost automation of plants.

- Growth momentum will continue.

- Good quarter with 9.2% qoq.

- In FMCG & chemicals company see projects related to brownfield expansion and low cost automation of plants.

- Growth momentum will continue.

4) Industrial products

- Demand was driven by digital, In creating smart products, value engineering of existing products and productivity improvement initiative from the shop floor.

- Company is setting up specialized labs in creating solution in cyber security.

- Demand was driven by digital, In creating smart products, value engineering of existing products and productivity improvement initiative from the shop floor.

- Company is setting up specialized labs in creating solution in cyber security.

- Sustainability trend is driving more spend towards alternative energy. Company is leveraging its domain and technical strengths to assist with the technology framework in this area.

5) Medical

- Soft quarter of 2.4%

- Some caution in spending because of resurgence of covid cases.

- New growth areas for the company telehealth & population health management.

- Soft quarter of 2.4%

- Some caution in spending because of resurgence of covid cases.

- New growth areas for the company telehealth & population health management.

Operations front

1) Training & upskilling

- Invested in global engineering academy, able to provide upskilling to 9K employees

- Focus on design labs, made company become only India based service provider to support amazon's Alexa voice service integration.

1) Training & upskilling

- Invested in global engineering academy, able to provide upskilling to 9K employees

- Focus on design labs, made company become only India based service provider to support amazon's Alexa voice service integration.

- Company has inhouse asset management portal, which has seen good traction.

2) Utilization

- Improved it in past 2 quarter which has improved the margin level.

- Employees have been getting back to office.

- Tried to adapt the Covid times

2) Utilization

- Improved it in past 2 quarter which has improved the margin level.

- Employees have been getting back to office.

- Tried to adapt the Covid times

R&D expenditure

- Company is seeing R&D spend in the areas of digital engineering and medical engineering.

- Commercial aerospace will take a little bit of time, the company is focusing on defense area in US.

- Company is seeing R&D spend in the areas of digital engineering and medical engineering.

- Commercial aerospace will take a little bit of time, the company is focusing on defense area in US.

On Deals

- Decision making happening at a faster pace than the last 2 quarter.

- For 100 millions dollar deal, the ramp up will start in a gradual manner. It has not contributed the revenue till now. It is going to contribute in a big way by next year.

- Decision making happening at a faster pace than the last 2 quarter.

- For 100 millions dollar deal, the ramp up will start in a gradual manner. It has not contributed the revenue till now. It is going to contribute in a big way by next year.

Digital engineering

- 49% of business comes from digital engineering.

- DE is divided into product, design, cloudification, analytics, creating cyber security product and remote design collab.

- The other part of DE is smart manufacturing.

- 49% of business comes from digital engineering.

- DE is divided into product, design, cloudification, analytics, creating cyber security product and remote design collab.

- The other part of DE is smart manufacturing.

Margins

- Headwinds including variable pay & sub contracting costs.

- As pandemic came, automotive customer asked for more discount than any other vertical.

- Aerospace business took a big hit which affected the company.

- Headwinds including variable pay & sub contracting costs.

- As pandemic came, automotive customer asked for more discount than any other vertical.

- Aerospace business took a big hit which affected the company.

• • •

Missing some Tweet in this thread? You can try to

force a refresh