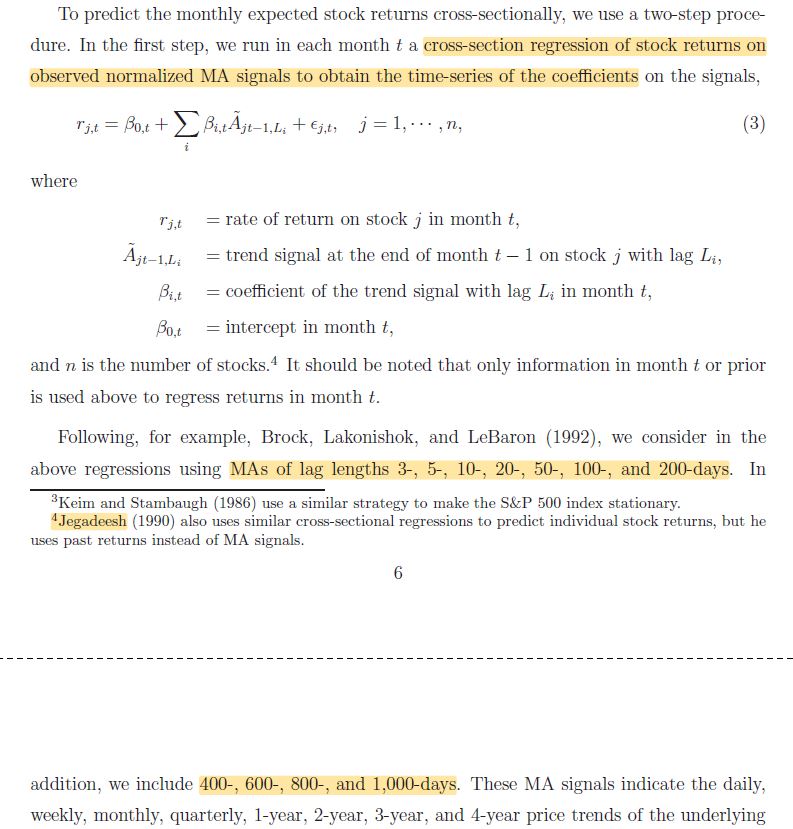

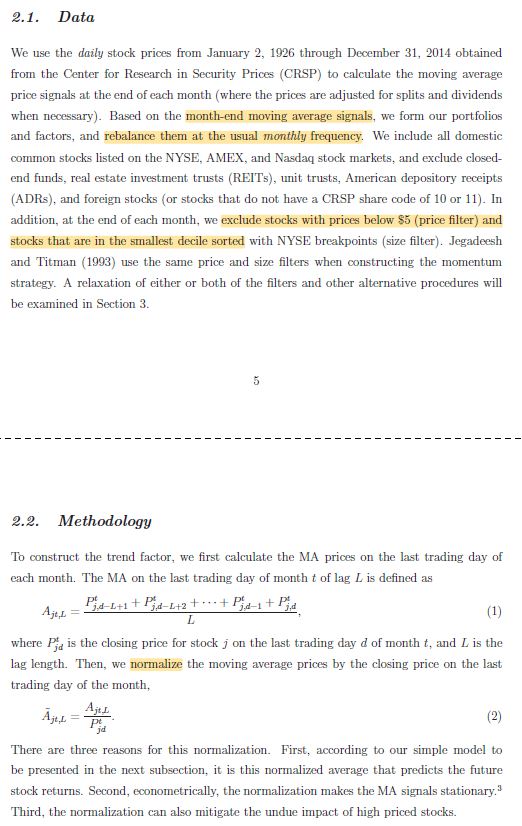

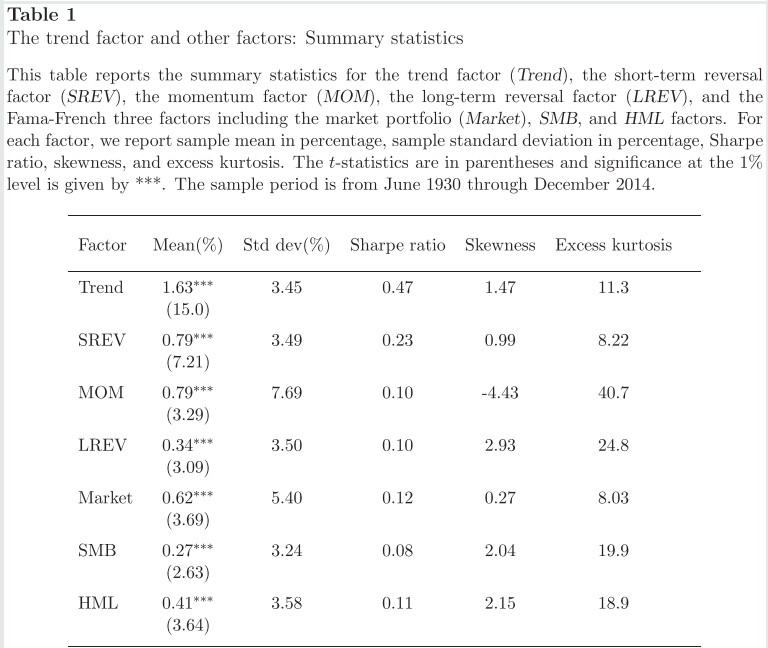

1/ Implementing Momentum: What Have We Learned? (Ross, Moskowitz, Israel, Serban)

"Live momentum portfolios are capable of capturing the momentum premium, even after expenses, trading costs, taxes, & other frictions associated with real-life portfolios."

papers.ssrn.com/sol3/papers.cf…

"Live momentum portfolios are capable of capturing the momentum premium, even after expenses, trading costs, taxes, & other frictions associated with real-life portfolios."

papers.ssrn.com/sol3/papers.cf…

2/ "We decompose the performance differences between the live momentum strategies and the theoretical AQR Momentum Indices.

"We expect that trading costs and expenses will always be a drag on performance, but ‘smarter’ portfolio construction decisions should offset this."

"We expect that trading costs and expenses will always be a drag on performance, but ‘smarter’ portfolio construction decisions should offset this."

3/ "Momentum's historical excess return is 1.0-1.5%/yr. Even if transaction costs were twice as high as realized, they may only put a small dent in performance.

"These results contrast with papers that estimates costs based on liquidity-demanding orders for immediate execution."

"These results contrast with papers that estimates costs based on liquidity-demanding orders for immediate execution."

4/ "While the momentum style has had a tough period over the past seven years, transaction costs were not the culprit.

"Despite the higher turnover relative to other style strategies, such as value and defensive, momentum still survives transaction costs."

"Despite the higher turnover relative to other style strategies, such as value and defensive, momentum still survives transaction costs."

5/ "Tax-managed strategies have captured a similar return premium as the regular MOM strategies, further evidenced by the high correlation of excess returns and low realized tracking error.

"They also have realized similar or lower taxes than the corresponding passive indices."

"They also have realized similar or lower taxes than the corresponding passive indices."

6/ "We expect and find that the costs of implementation are small, while the benefits of portfolio construction are significant. A live strategy captures the theoretical momentum premium without incurring substantial real-world costs and potentially adds value."

7/ Related research:

Option Trading Costs Are Lower than You Think

Tax-Managed Factor Strategies

Tax Benefits of Separating Alpha from Beta

Taxes, Shorting, and Active Management

Option Trading Costs Are Lower than You Think

https://twitter.com/ReformedTrader/status/1346160221408829441

Tax-Managed Factor Strategies

https://twitter.com/ReformedTrader/status/1218724897544794112

Tax Benefits of Separating Alpha from Beta

https://twitter.com/ReformedTrader/status/1221273388057915392

Taxes, Shorting, and Active Management

https://twitter.com/ReformedTrader/status/1073478278080475136

8/ To Trade or Not to Trade? Informed Trading With Short-Term Signals for Long-Term Investors

Comparing Cost-Mitigation Techniques

https://twitter.com/ReformedTrader/status/1323470487171706884

Comparing Cost-Mitigation Techniques

https://twitter.com/ReformedTrader/status/1341581135944376321

• • •

Missing some Tweet in this thread? You can try to

force a refresh