1/ People often talk about $FB's network effects but for me what really flies under the radar is their SMB acquisition engine. This is part of a three step playbook that they've replicated for reach of their properties (Facebook "Blue App", Instagram, etc.)

2/ Step 1 - focus on user acquisition, engagement, and retention. Once they understand the primary behaviours and moments of delight that hook users and drive stickiness, do everything possible with the product to reinforce this.

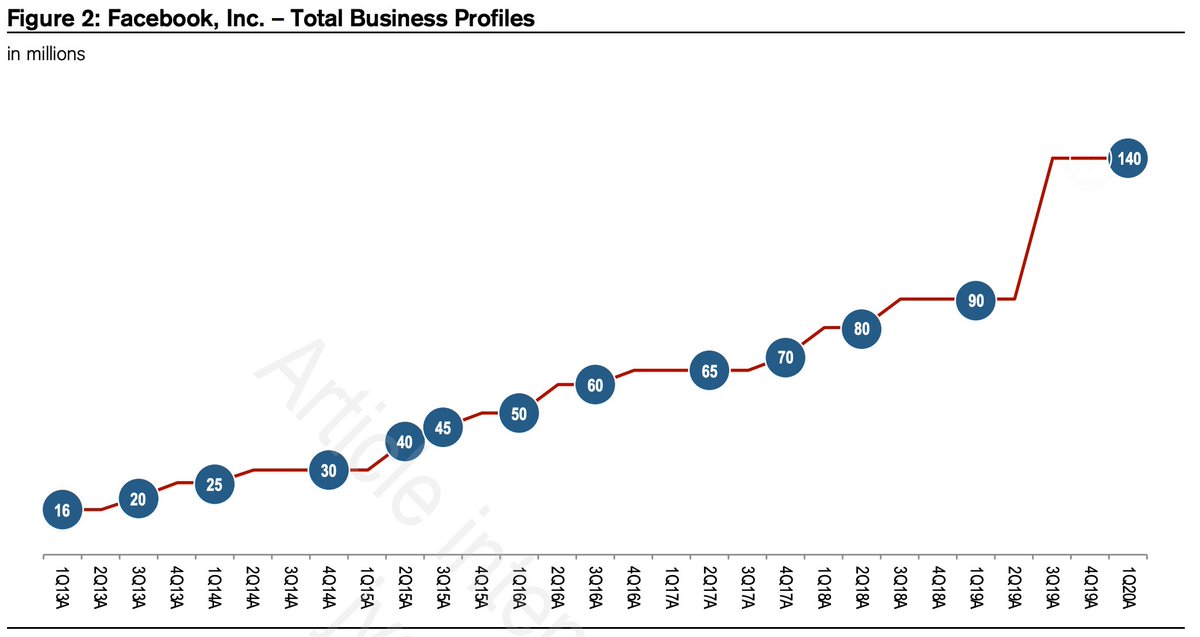

3/ Step 2 - create organic opportunities and free tools for businesses to interact with users in the product. For ex., FB has >140M Business Pages. These pages not only provide utility to users and familiarize businesses with FB tools but they act as a funnel into step 3.

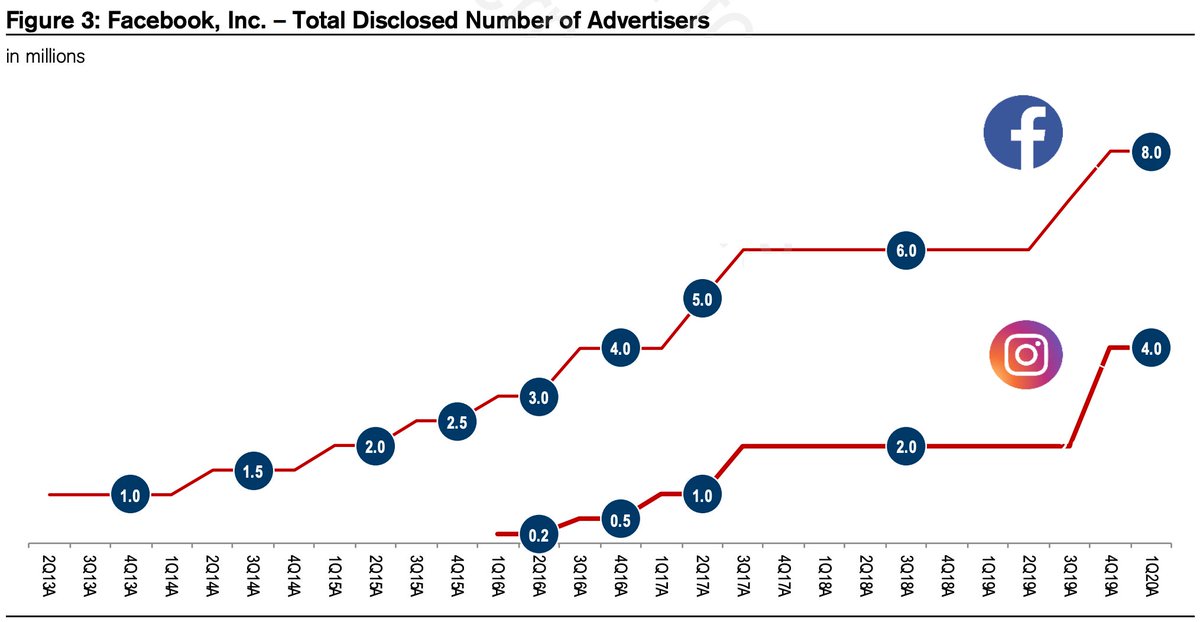

4/ Step 3 - provide paid self-serve tools for businesses to increase their interactions and exposure to potential customers (ie paid ads). Currently $FB has >12M active advertisers

5/ It's step 2 that's really the under appreciated part of $FB's strategy. Instead of building a massive S&M org, they've leveraged product to create a global acquisition engine. Not only has this saved $10B's but you couldn't even scale this fast if you relied on people

6/ This also help explains WhatsApp's current strategy. $FB wants to attract SMBs (ie currently at 15M in India) by providing free tools (ie Kustomer) to facilitate commerce and customer service. They'll then monetize through payments and increased ad prices by "closing the loop"

7/ PS. as you can see from the charts, COVID has led to a huge explosion in SMBs coming on to $FB's free platform. There's been a lag in conversion from free to paid advertising but expect that to jump as things normalize and SMBs are once again comfortable in spending

• • •

Missing some Tweet in this thread? You can try to

force a refresh