Thread on the good things that have come from WSBs yolos:

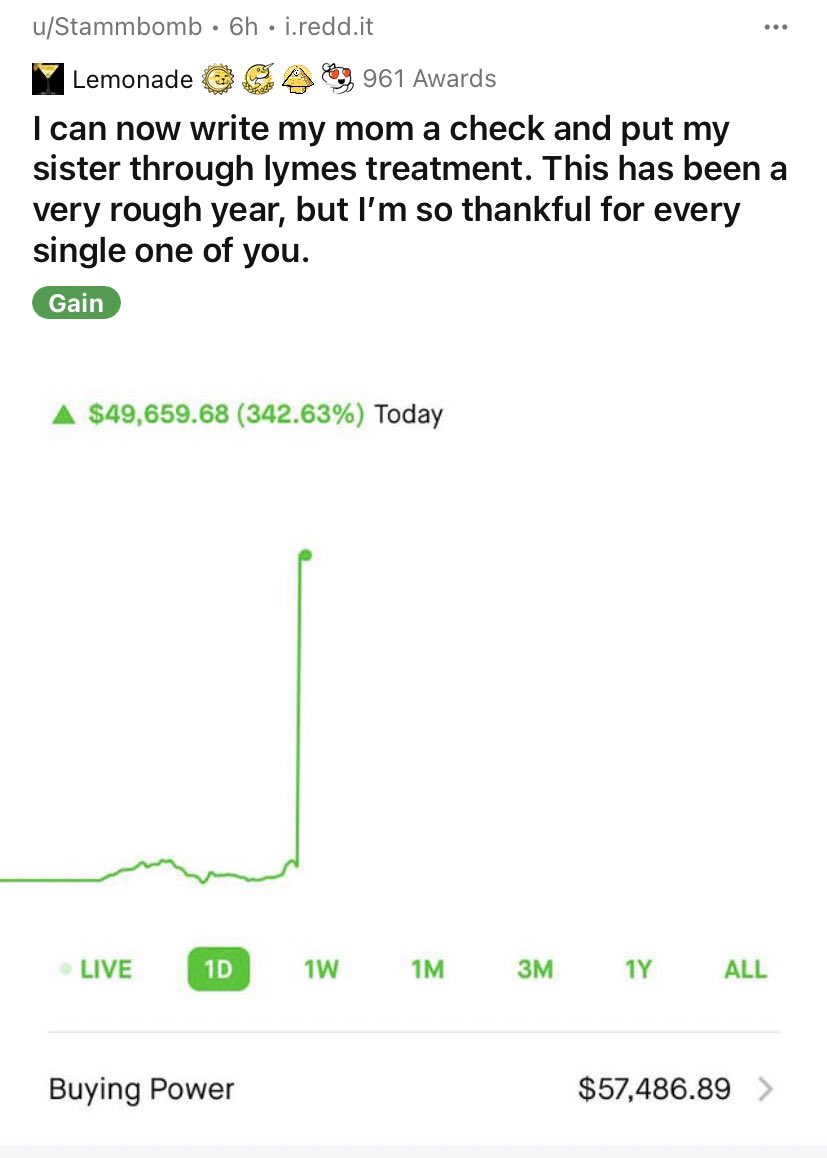

Kid helps his mom pay for his sisters Lyme Disease treatment:

Kid helps his mom pay for his sisters Lyme Disease treatment:

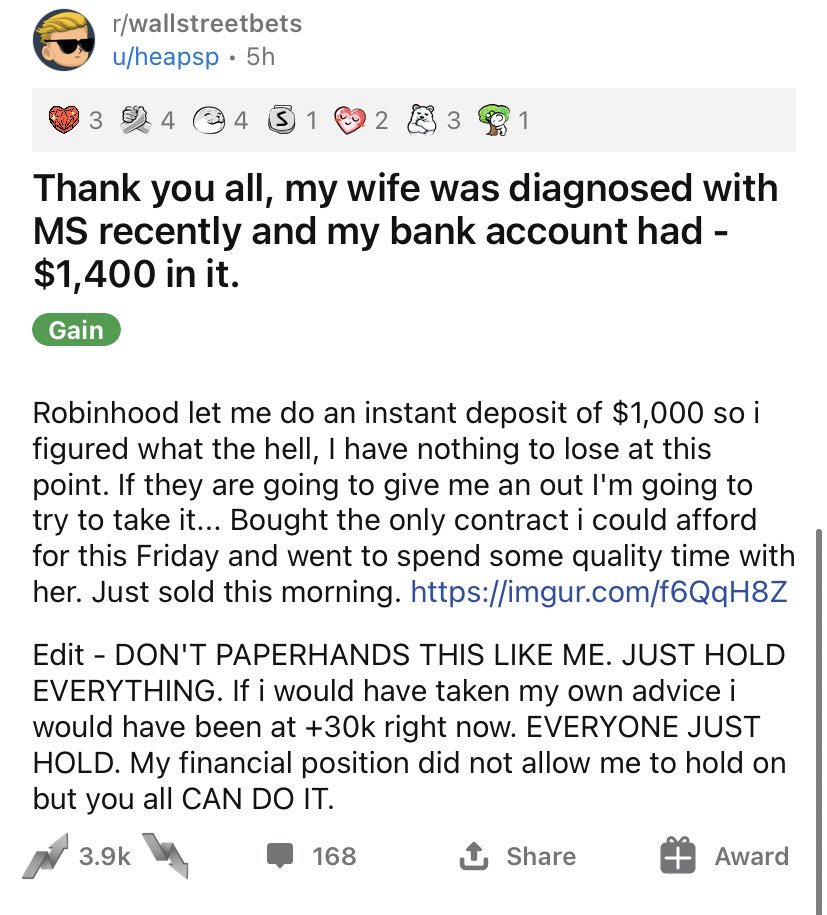

Husband supporting his wife who was just diagnosed with MS.

Guy wanted to buy a Nissan, is now probably buying a BMW.

Poor as dirt guy able to buy groceries with his GME profits.

Single Dad able to turn left overs from his stimmy check into $4k for his 5 kids.

Guys paid off his student loan debt:

Donating to Charity with your winnings is actually a huge thing on WSBs, several posts about that, even list of good charities that do go work.

Feel free to add more. Please include a screenshot.

• • •

Missing some Tweet in this thread? You can try to

force a refresh