Laurus Labs conducted their earnings con-call today at 11:00 am

Here are the key highlights 😀👇

@unseenvalue @drprashantmish6 @punitbansal14 @shrutiahuja110 @SwarnashishC

#concall

Here are the key highlights 😀👇

@unseenvalue @drprashantmish6 @punitbansal14 @shrutiahuja110 @SwarnashishC

#concall

Business Updates:

• Contributor for this year was the robust product basket.

• Formulation contribution of 39%.

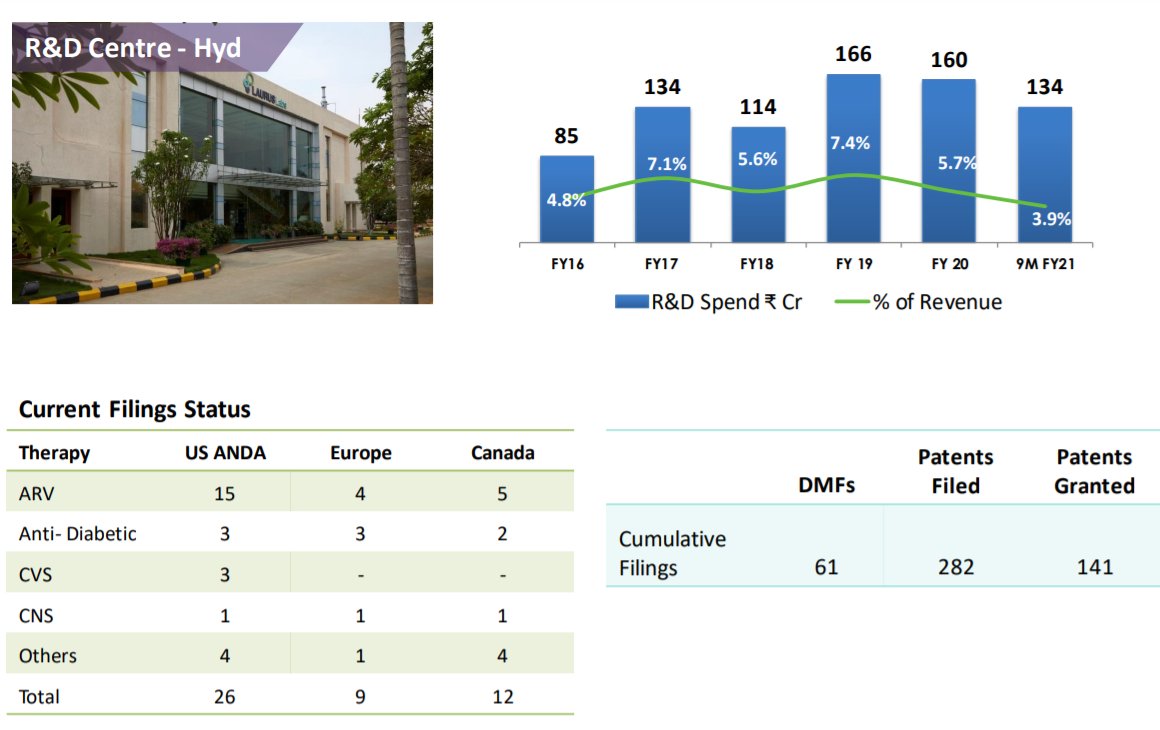

• See product filing in image

• Continue investing in infrastructure.

• De-bottle-necking the plant continuous to remain online.

• Contributor for this year was the robust product basket.

• Formulation contribution of 39%.

• See product filing in image

• Continue investing in infrastructure.

• De-bottle-necking the plant continuous to remain online.

• Expanding capacities in key API.

• See the segment revenue breakup in the image.

• Dedicated a special plant location for CRAMS Facility.

• Richcore will be named as Lauruas Bio and acquired 100% in Richcore

• See the segment revenue breakup in the image.

• Dedicated a special plant location for CRAMS Facility.

• Richcore will be named as Lauruas Bio and acquired 100% in Richcore

TLE to TLE transaction

• Majority of the sales coming from TLD.

• However company has more molecules filed in TLE which make more growth available in TLE segment

• Majority of the sales coming from TLD.

• However company has more molecules filed in TLE which make more growth available in TLE segment

• ARV margins- Gross margins was less in Q3 due to delay of of export incentives. However this quarter margins remain on line.

Capacity:

• Currently company is at optimum utilization and de-bottlenecking of the plant will be finished in Q4.

Capacity:

• Currently company is at optimum utilization and de-bottlenecking of the plant will be finished in Q4.

• There are 8 formulation player active who have filed for Doltagrovate molecule while there are no player who is WHO certified for the API division.

HIV:

• Doubling the segment is impossible as the patients in the disease are not that higher.

• Growth in HIV will come from demand moving from weak players to strong players.

• Doubling the segment is impossible as the patients in the disease are not that higher.

• Growth in HIV will come from demand moving from weak players to strong players.

Diabetic and Cardiovascular

• Strong product basket in Diabetic, while Cardiovascular will be another growth driver.

• There are not much development left in ARV segment for Laurus, hence in future major growth driver non ARV.

• After 3-5 year, growth driver will be Laurus Bio

• Strong product basket in Diabetic, while Cardiovascular will be another growth driver.

• There are not much development left in ARV segment for Laurus, hence in future major growth driver non ARV.

• After 3-5 year, growth driver will be Laurus Bio

Investment in Laurus Bio

• Co. don't see any challenges to invest over there

• Bio is high margin business and is expected to deliver good cash flow for the business. Hence mgmt expect most of the investment to be internally funded.

• Not much of CAPEX is allocated now to Bio.

• Co. don't see any challenges to invest over there

• Bio is high margin business and is expected to deliver good cash flow for the business. Hence mgmt expect most of the investment to be internally funded.

• Not much of CAPEX is allocated now to Bio.

Nutraceuticals and Cosmoceuticals

• It was added in CDMO product. As it also commodity business company is not much in the business but there are tie ups with big customer.

• It was added in CDMO product. As it also commodity business company is not much in the business but there are tie ups with big customer.

Long Active Injectables

• Co. is watching ARV business since past many years, hence any new disruption will be in close eyes of Laurus.

• Injectables is currently not signed by WHO and and company don't expect it till 2025

• Co. have molecules in the pipeline for injectables.

• Co. is watching ARV business since past many years, hence any new disruption will be in close eyes of Laurus.

• Injectables is currently not signed by WHO and and company don't expect it till 2025

• Co. have molecules in the pipeline for injectables.

For more stock market discussion do join our Telegram Channel

t.me/thetycoonminds…

t.me/thetycoonminds…

• • •

Missing some Tweet in this thread? You can try to

force a refresh