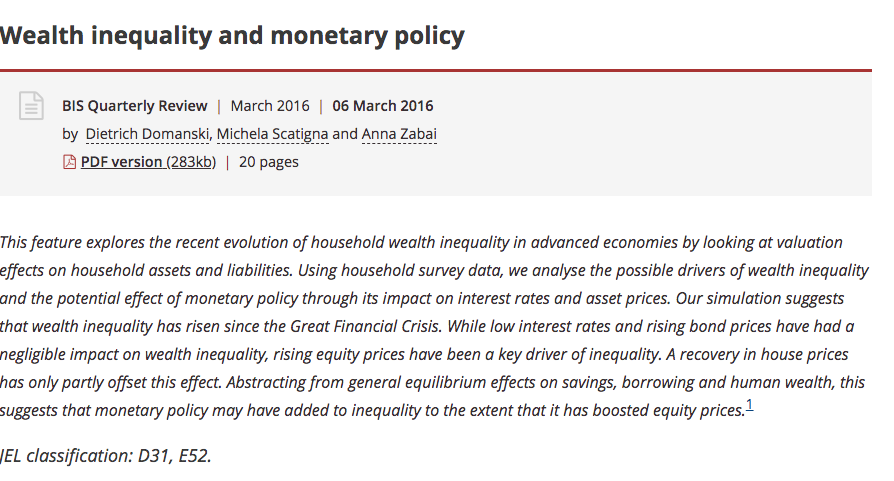

remember those massive central bank purchases of governments bonds & 'we're here to close spreads' last year?

my new report 'Revolution without revolutionaries: the return of monetary financing'

argues we live in a world of Minsky without Keynes.

transformative-responses.org/wp-content/upl…

my new report 'Revolution without revolutionaries: the return of monetary financing'

argues we live in a world of Minsky without Keynes.

transformative-responses.org/wp-content/upl…

Historically, we can trace two regimes of monetary financing, subordinated MF vs shadow MF.

across (a) objectives of intervention, (b) targets, (c) institutional hierarchy, (d) macroeconomic paradigm, and (e) accumulation regime/distribution of political power.

across (a) objectives of intervention, (b) targets, (c) institutional hierarchy, (d) macroeconomic paradigm, and (e) accumulation regime/distribution of political power.

Since 2008, central banks have quietly adopted shadow monetary financing. This is Minsky without Keynes: central banks upgrade tools to evolving financial system – shadow banking or market-based finance– without fiscal authorities reclaiming their Keynesian dominance.

Alberto Giovannini – the architect of Eurozone’s macro-financial architecture – called the state a collateral factory for modern financial systems.

central bank purchases reflect the new macro-financial role that government bonds play in collateral-intensive finance.

central bank purchases reflect the new macro-financial role that government bonds play in collateral-intensive finance.

In contrast to Keynesian “public-sector subordination” channel, shadow MF relies on “private-sector” channel, w two-fold objective:

(a) prudential or market-maker of last resort purchases of government bonds

(b) macrodriven purchases that anchor inflationary expectations (QE)

(a) prudential or market-maker of last resort purchases of government bonds

(b) macrodriven purchases that anchor inflationary expectations (QE)

my favourite empirical nugget: shadow monetary financing had by 2021 lasted for longer & involved more systematic central bank interventions in government bond markets than the much-feared subordinated monetary financing under Keynesian fiscal dominance.

In the Revolution without Revolutionaries, central banks have been remarkably successful at breaking monetary taboos they worked hard to construct, without having to specify boundaries of – and their accountability in – the new policy regime.

But:

But:

https://twitter.com/DanielaGabor/status/1355140854592249856?s=20

if we dont ensure the 'revolution' is transformative of monetary-fiscal relations, we may sacrifice fiscal support for low-carbon transition on altar of central bank independence.

next Friday, 05/02, at 15.45 CET:

you can watch a former ECB central banker disagreeing with my take (she promised!), at the @finanzwende conference, in what must be the first women-only panel on central banking!

registration here:

transformative-responses.org/the-project/ne…

you can watch a former ECB central banker disagreeing with my take (she promised!), at the @finanzwende conference, in what must be the first women-only panel on central banking!

registration here:

transformative-responses.org/the-project/ne…

as many have pointed out, this is not the first women-only panel on central banking, I've even been in one, just unable to contain my excitement on what promises to be some proper disagreement.

chaired by the marvellous @Frank_vanlerven

chaired by the marvellous @Frank_vanlerven

shadow monetary financing stats: UK's Treasury has received £110bn in 'net earnings' from Bank of England's £800bn QE program since 2009.

nice to have your own bazooka.

nice to have your own bazooka.

the UK Treasury is literally paying interest to itself - while Bank of England keeps rates low.

• • •

Missing some Tweet in this thread? You can try to

force a refresh