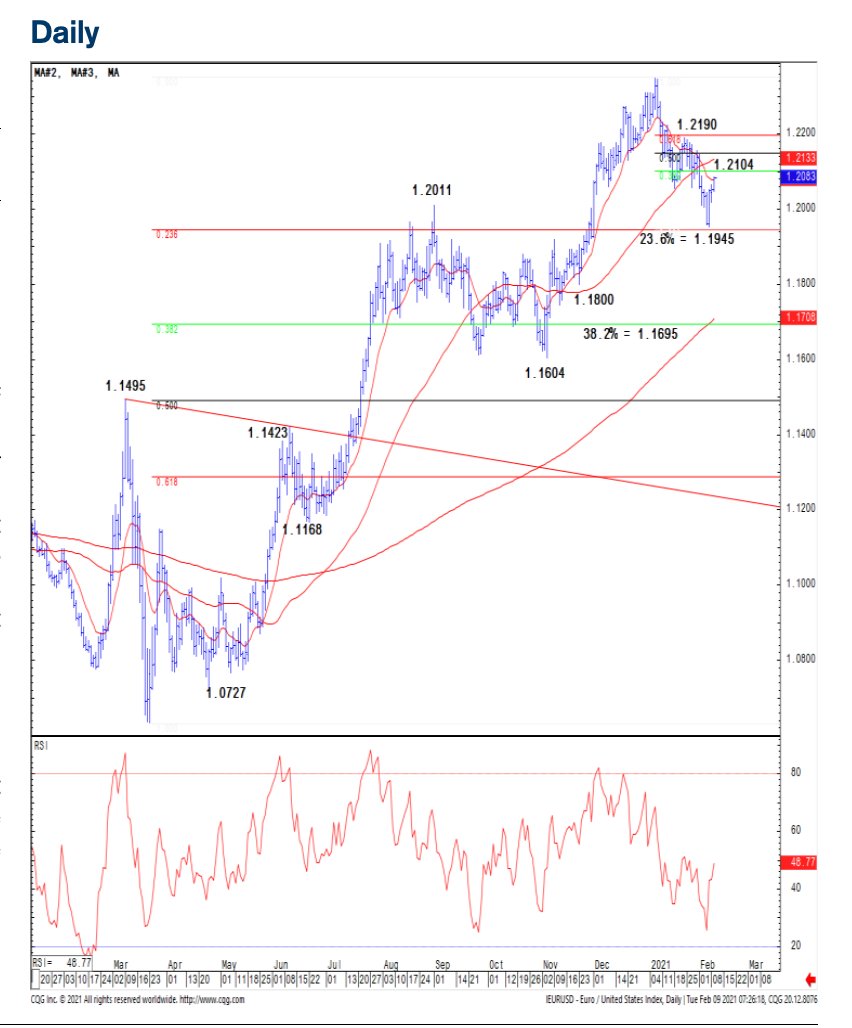

Credit Suisse 1/5: #EURUSD: A bullish “reversal day” from our 1.1945/14 target leaves the immediate risk higher #EURUSD continues to push higher following the bullish “reversal day” from our target at 1.1945/14- the 23.6% retracement of the entire 2020/2021 uptrend

Credit Suisse 2/5: and first “measured top objective” – and whilst we think there is scope for this recovery to further yet, our bias for now remains to treat this as a temporary bounce.

Resistance moves to 1.2088 initially, then 38.2% retracement of the Jan/Feb fall at 1.2104.

Resistance moves to 1.2088 initially, then 38.2% retracement of the Jan/Feb fall at 1.2104.

Credit Suisse 3/5: We would look for this to then ideally cap for a fresh move lower. Beyond 1.2104 though would suggest we may be seeing near-term range shift sideways with resist then seen next in 1.2156/90 zone, but with this then expected to cap to define the top of a range.

Credit Suisse 4/5: Support is seen at 1.2046 initially, then 1.2019, beneath which is needed to reassert a bearish bias for a move back to 1.1981, then 1.1951/45. Below here would confirm a more significant correction lower with support seen next at 1.1800

Credit Suisse 5/5: and more importantly at 1.1705/1.1695– the 38.2% retracement of the 2020/2021 uptrend and 200-day average.

Support at 1.1945 is holding for now as expected with

resistance seen at 1.2104.

Support at 1.1945 is holding for now as expected with

resistance seen at 1.2104.

• • •

Missing some Tweet in this thread? You can try to

force a refresh