Forex & Cryptos my expertise. Chairman and Founder at https://t.co/oTbBlzoN9X, https://t.co/Mo23d7Q7yd and The ITI - International Trading Institute

Forex Live 2/5: That said, the dollar looks vulnerable across the board with 10-year #Treasury yields also sitting on the cusp of a soft bottom closer to 1.60%, so there's that to consider.

Forex Live 2/5: That said, the dollar looks vulnerable across the board with 10-year #Treasury yields also sitting on the cusp of a soft bottom closer to 1.60%, so there's that to consider. JP Morgan 2/7: far surpassing the consensus expectation of 61.5. This 37-year record high is a reflection of robust manufacturing activity driven by strong growth in orders, production and employment, along with increases in prices paid for inputs.

JP Morgan 2/7: far surpassing the consensus expectation of 61.5. This 37-year record high is a reflection of robust manufacturing activity driven by strong growth in orders, production and employment, along with increases in prices paid for inputs.

MUFG 2/5: a one-day record. In Germany on Thursday, 719k vaccines were administered while in Italy the 7-day average of administered vaccines hit 200k for the first time over the weekend.

MUFG 2/5: a one-day record. In Germany on Thursday, 719k vaccines were administered while in Italy the 7-day average of administered vaccines hit 200k for the first time over the weekend.

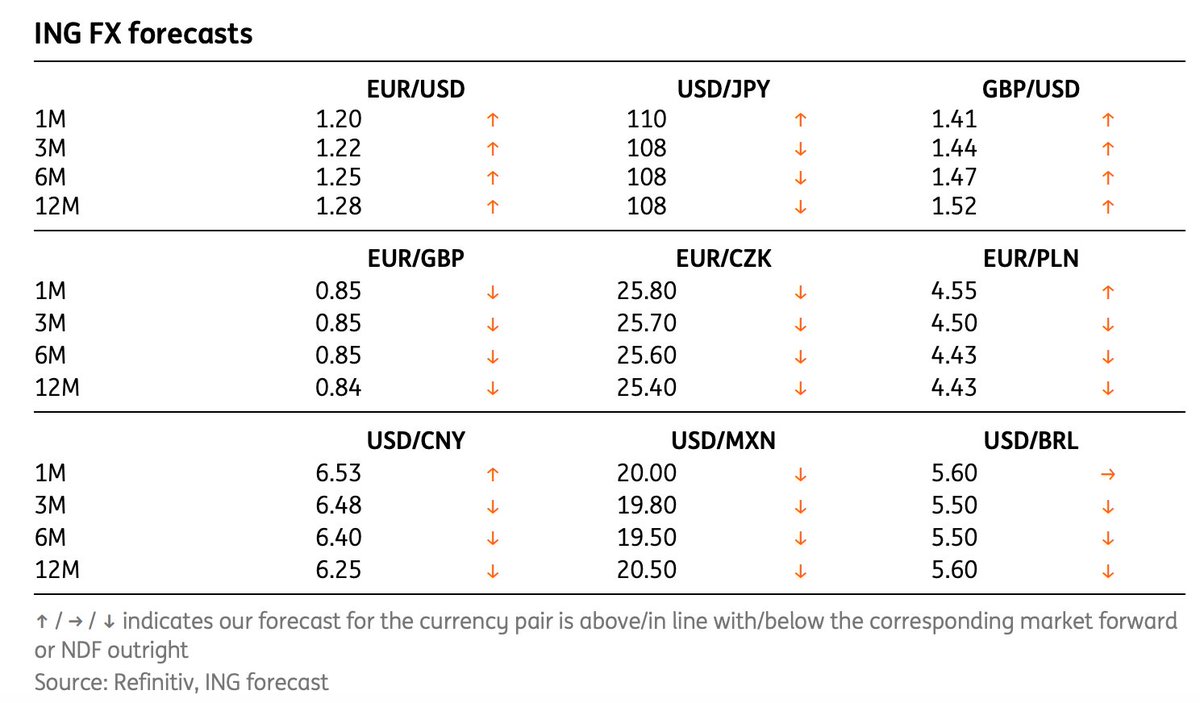

ING Bank 2/4: is gathering dust in a Karlsruhe courtroom stand in stark contrast to the achievements in the US. Yet all is not lost. European manufacturing is holding up well and there are signs of life in the EU vaccine roll-out.

ING Bank 2/4: is gathering dust in a Karlsruhe courtroom stand in stark contrast to the achievements in the US. Yet all is not lost. European manufacturing is holding up well and there are signs of life in the EU vaccine roll-out.