1/ Thread: $UBER 4Q'20 Update

"If a stock doubles on you and you thought it was expensive 50% lower, nine times out of ten its time to learn something."- @JerryCap

I passed on $UBER at $34/share, and it's been +85% since then.

Here are my notes from Q4 earnings call.

"If a stock doubles on you and you thought it was expensive 50% lower, nine times out of ten its time to learn something."- @JerryCap

I passed on $UBER at $34/share, and it's been +85% since then.

Here are my notes from Q4 earnings call.

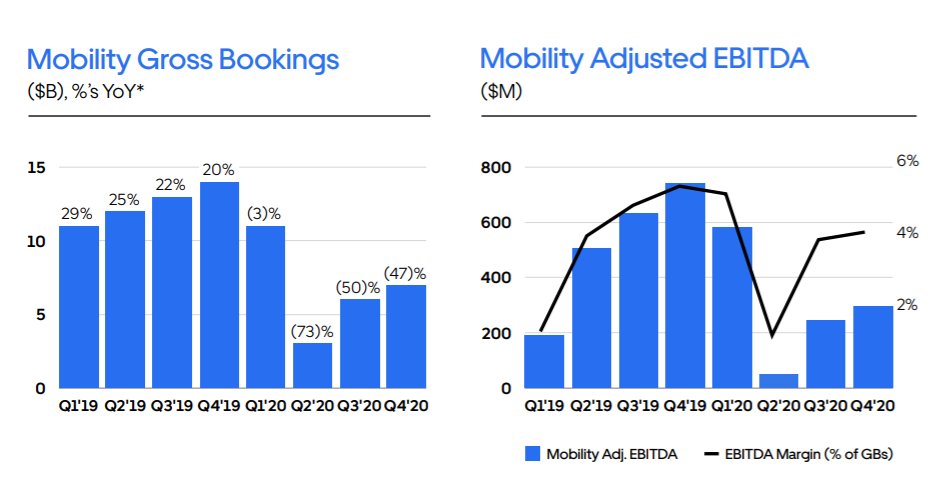

2/ Total gross bookings -4% YoY, but +16% QoQ.

Revenue -15% YoY, but +13% QoQ

Take rates down 221 bps YoY, primarily because mix shift to delivery which is lower take rates business

Strong conviction of reaching adj EBITDA profitability sometime in 2021.

Revenue -15% YoY, but +13% QoQ

Take rates down 221 bps YoY, primarily because mix shift to delivery which is lower take rates business

Strong conviction of reaching adj EBITDA profitability sometime in 2021.

3/ Mobility

Mobility appears to be improving in January; Brazil is at ~90% of last year's bookings.

Airport travel is the real laggard here, currently indexed at 27% of last year's bookings.

Expects WFH to continue, but travel to come back strongly this.

Mobility appears to be improving in January; Brazil is at ~90% of last year's bookings.

Airport travel is the real laggard here, currently indexed at 27% of last year's bookings.

Expects WFH to continue, but travel to come back strongly this.

4/ Delivery

I seriously underestimated delivery's pace of growth. It continues unabated.

Delivery is adj EBITDA profitable in "profitable markets" (15 markets). "Investment markets" also showed a significant progress and getting closer to breakeven.

I seriously underestimated delivery's pace of growth. It continues unabated.

Delivery is adj EBITDA profitable in "profitable markets" (15 markets). "Investment markets" also showed a significant progress and getting closer to breakeven.

5/ On track to achieve $200 mn synergy with Postmates deals.

Company gross bookings likely to come back to growth in Q1.

Company gross bookings likely to come back to growth in Q1.

6/ "And we continue also to benefit from basket-size increases. And as basket size increase, the cost of the delivery stays the same. And again, that accrues to margin as well."

Frequency of orders by members is "significantly higher" than non-members. Membership increased to 5M

Frequency of orders by members is "significantly higher" than non-members. Membership increased to 5M

7/ Although Brazil is at ~90% recovery, 30% of high-value customers are yet to come back (airport travel?)

When mobility comes back, Uber is slightly concerned whether they will have enough drivers to support the demand.

When mobility comes back, Uber is slightly concerned whether they will have enough drivers to support the demand.

8/ Uber has come back faster than taxi and transit demand.

Number of trips is growing faster than bookings.

Number of trips is growing faster than bookings.

9/ Comment on Drizly

Eats is search merchant first, and then product while Drizly is search product first, and then merchant.

Take rates, basket size are larger for Drizly. Currently profitable.

Eats is search merchant first, and then product while Drizly is search product first, and then merchant.

Take rates, basket size are larger for Drizly. Currently profitable.

10/ Uber Direct, although small % of Uber's business, is 18% of Postmates' business which experienced strong growth.

11/ Overall, 2020 was a very busy year for Uber; executed 17 transactions in 2020.

Uber expects structurally lower CAC compared to competitors, primarily driven by the membership model.

Uber expects structurally lower CAC compared to competitors, primarily driven by the membership model.

End/ Used @KoyfinCharts transcripts this time (no affiliation): app.koyfin.com/news/ts/eq-jt7…

My deep dive on Uber: mbi-deepdives.com/deep-dive-on-u…

My deep dive on Uber: mbi-deepdives.com/deep-dive-on-u…

• • •

Missing some Tweet in this thread? You can try to

force a refresh