Here’s the thing about bubbles: They always need more buyers to push the price higher.

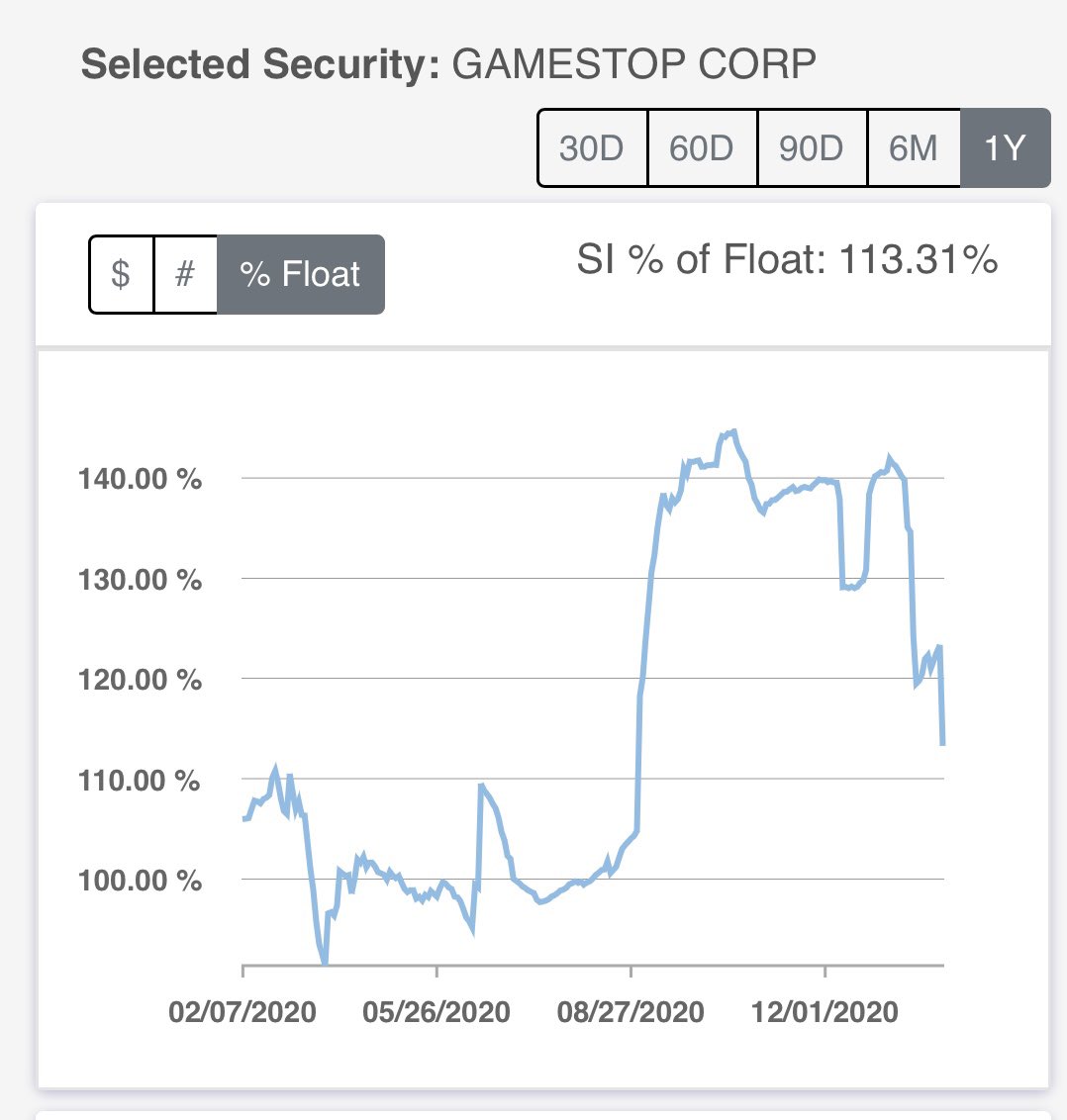

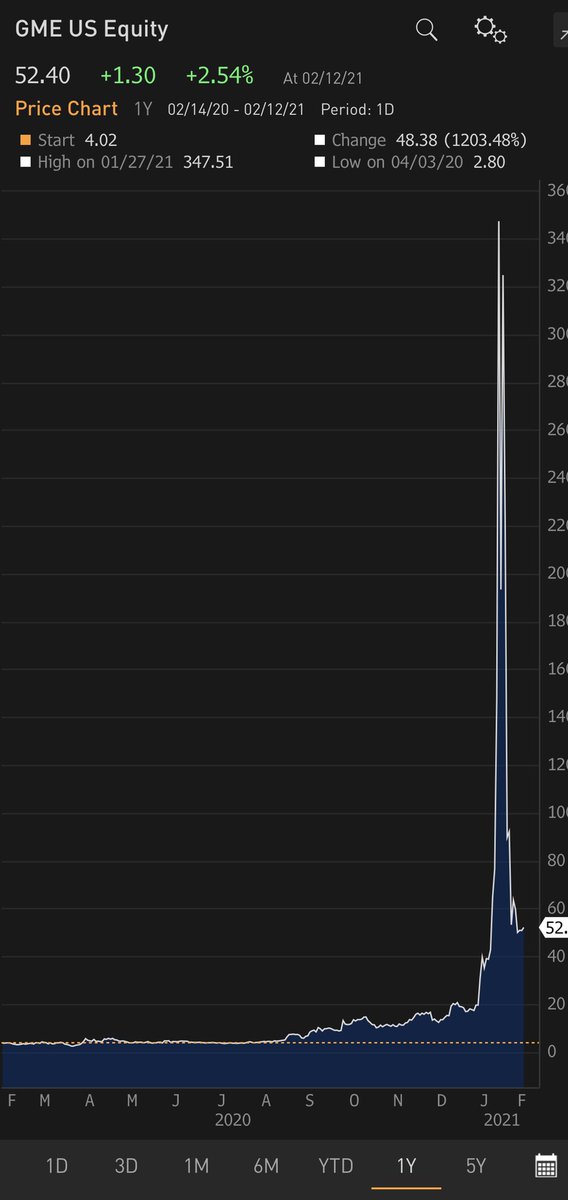

The $GME bubble inflated initially as #wallstreetbets realized that with 140% short interest, $ could be made. Seeing others’ blood in the Street, HFs jumped in, further inflating the bubble.

The $GME bubble inflated initially as #wallstreetbets realized that with 140% short interest, $ could be made. Seeing others’ blood in the Street, HFs jumped in, further inflating the bubble.

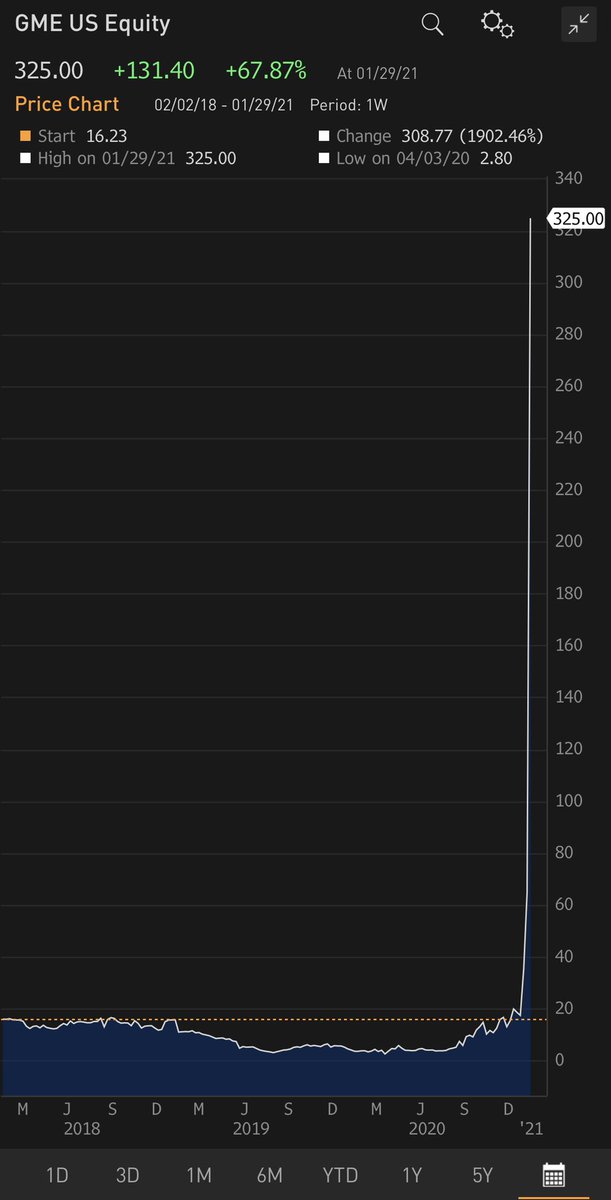

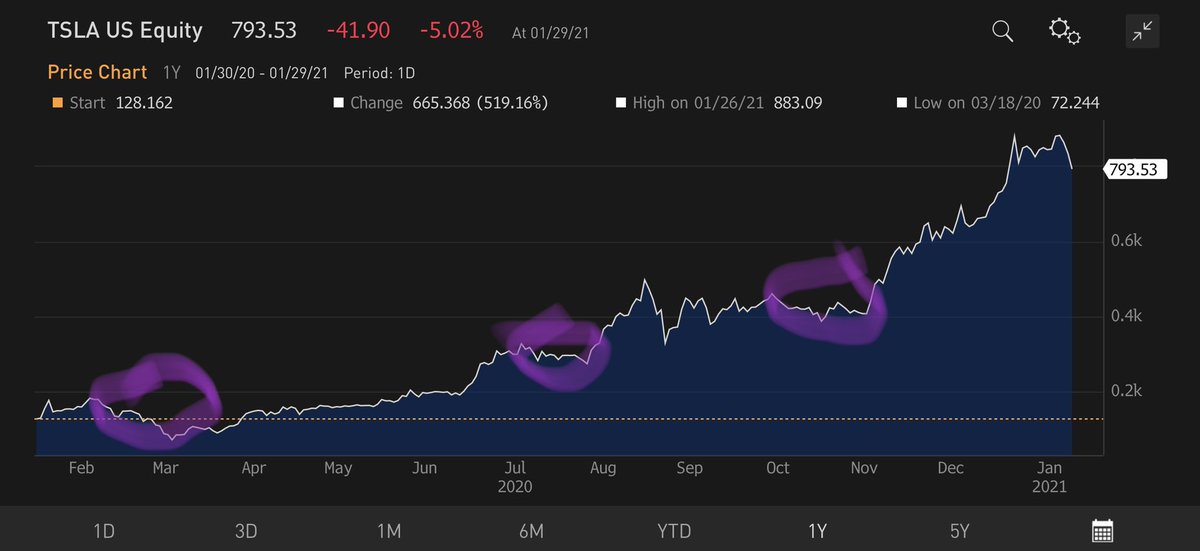

2/ At $325, up from $20 two wks earlier w/ no chg in fundamentals, the $GME bubble was clear for all to see, but shorts needed a catalyst. The catalyst came when RH slapped a limit on new purchases, which shorts correctly perceived would keep new buyers out, and the bubble burst.

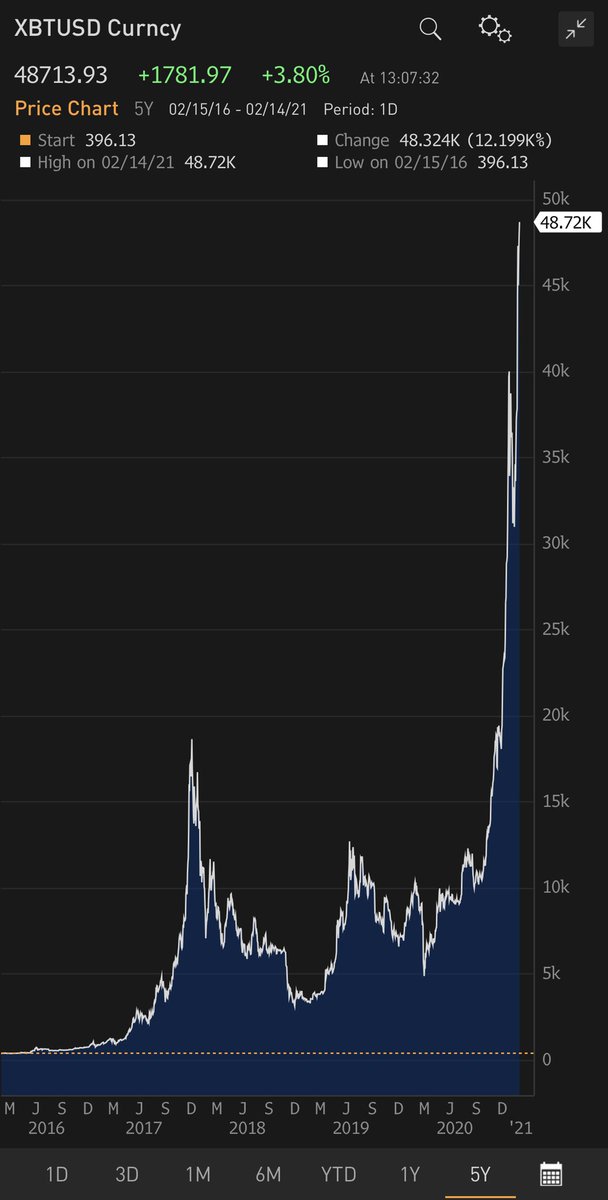

3/ Now there’s #BTC approaching $50K, up from $10K four months ago, w/ no change in fundamentals. As with $GME initially, there’s no catalyst to stop buyers from entering the #BTC bubble. Once Treasury Secretary Yellen proposes new regs, the #BTC bubble will burst just like $GME.

4/ Those who get hurt as #BTC collapses will certainly blame Secy Yellen in the same way those who got burned gambling on $GME blamed RH for imposing new restrictions. Both bubbles were destined to break, and all bubbles ultimately burst when there are no more fools to entice.

• • •

Missing some Tweet in this thread? You can try to

force a refresh