Bitcoin's total energy usage is determined primarily from market capitalization and difficulty adjustments, not transaction volume.

In other words, the marginal bitcoin transaction/spending choice has virtually no impact on bitcoin's total energy usage.

In other words, the marginal bitcoin transaction/spending choice has virtually no impact on bitcoin's total energy usage.

https://twitter.com/LucasdiGrassi/status/1374751398861144067

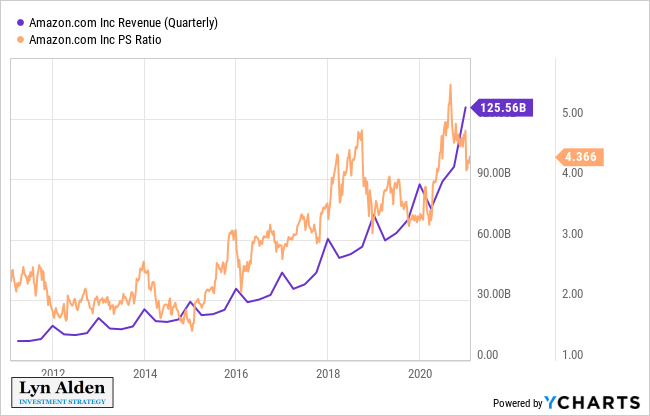

Like with a company, it takes a ton of work to make a good software product (equipment, staff, time, etc).

But then, it takes minimal work to send that software to 1,000,000,000 users compared to 10,000 users.

High base cost for it to exist + tiny cost per marginal user.

But then, it takes minimal work to send that software to 1,000,000,000 users compared to 10,000 users.

High base cost for it to exist + tiny cost per marginal user.

Bitcoin's overall energy usages does go up with adoption as a store of value as its market cap grows, but in a nonlinear way as it matures. It needs to be secure to function, but from there, its marginal cost per user is efficient.

swanbitcoin.com/bitcoin-fee-ba…

swanbitcoin.com/bitcoin-fee-ba…

However, the bitcoin network can only handle a finite number of daily base layer transactions. From there, secondary layers can multiply that number arbitrarily.

In other words, if 10x more people use bitcoin in 5 years, it won't use 10x more energy than now.

In other words, if 10x more people use bitcoin in 5 years, it won't use 10x more energy than now.

Dividing "bitcoin's total energy usage" by "number of transactions" to determine "energy per transaction" falsely implies that your decision to spend bitcoin or hold it, linearly affects how much energy the bitcoin network uses that day, whereas it doesn't.

The only way that individual transactions on goods/services affect energy usage in the long run is by affecting the fee portion of miner revenue, but that remains a minimal part of bitcoin's energy usage.

And secondary layers, like Lightning, make that even more efficient, and further eliminate the additional marginal energy usage per transaction.

The marginal decision to make a Lightning transaction has close to zero impact on anything. Like sending an email.

The marginal decision to make a Lightning transaction has close to zero impact on anything. Like sending an email.

This is different from, say, making the marginal decision to fly a private jet somewhere. Your decision to fly or not fly the jet will linearly affect how much C02 gets emitted that day.

This is not the case for deciding whether to hold or spend a bitcoin (or send an email).

This is not the case for deciding whether to hold or spend a bitcoin (or send an email).

Bitcoin's store of value aspect is what mostly drives the total energy usage of the network, since that is what mainly drives the market cap up.

The medium-of-exchange portion of that network, if successful, is very minimal in terms of additional energy usage.

The medium-of-exchange portion of that network, if successful, is very minimal in terms of additional energy usage.

Much of the criticism around bitcoin's energy usage misinterprets the scaling mechanism and which factors affect bitcoin's total energy usage.

Buying it and driving up market cap does indirectly increase energy usage, nonlinearly.

Spending it vs holding it, however, not really.

Buying it and driving up market cap does indirectly increase energy usage, nonlinearly.

Spending it vs holding it, however, not really.

Plus, due to the incentive mechanism for miners to find cheap energy, the energy that is used for the bitcoin network is increasingly renewable or wasted/stranded energy, which is good to strive for.

https://twitter.com/MartyBent/status/1374753249497128961

Lastly, a lot of energy concerns directed at Bitcoin start with the presupposition that it's useless. A trillion dollars in market cap disagrees.

Little concern is given to worldwide washing machine energy usage, for example, because we understand the value.

Little concern is given to worldwide washing machine energy usage, for example, because we understand the value.

• • •

Missing some Tweet in this thread? You can try to

force a refresh