How much of road spending is funded with user taxes in your state?

taxfoundation.org/state-infrastr…

taxfoundation.org/state-infrastr…

Both the federal government and the states raise revenue for infrastructure spending through taxes on motor fuel and vehicles. States also collect fees from toll roads and other road charges.

However, neither the federal government nor the vast majority of states collect enough taxes through these levies to cover infrastructure-related spending.

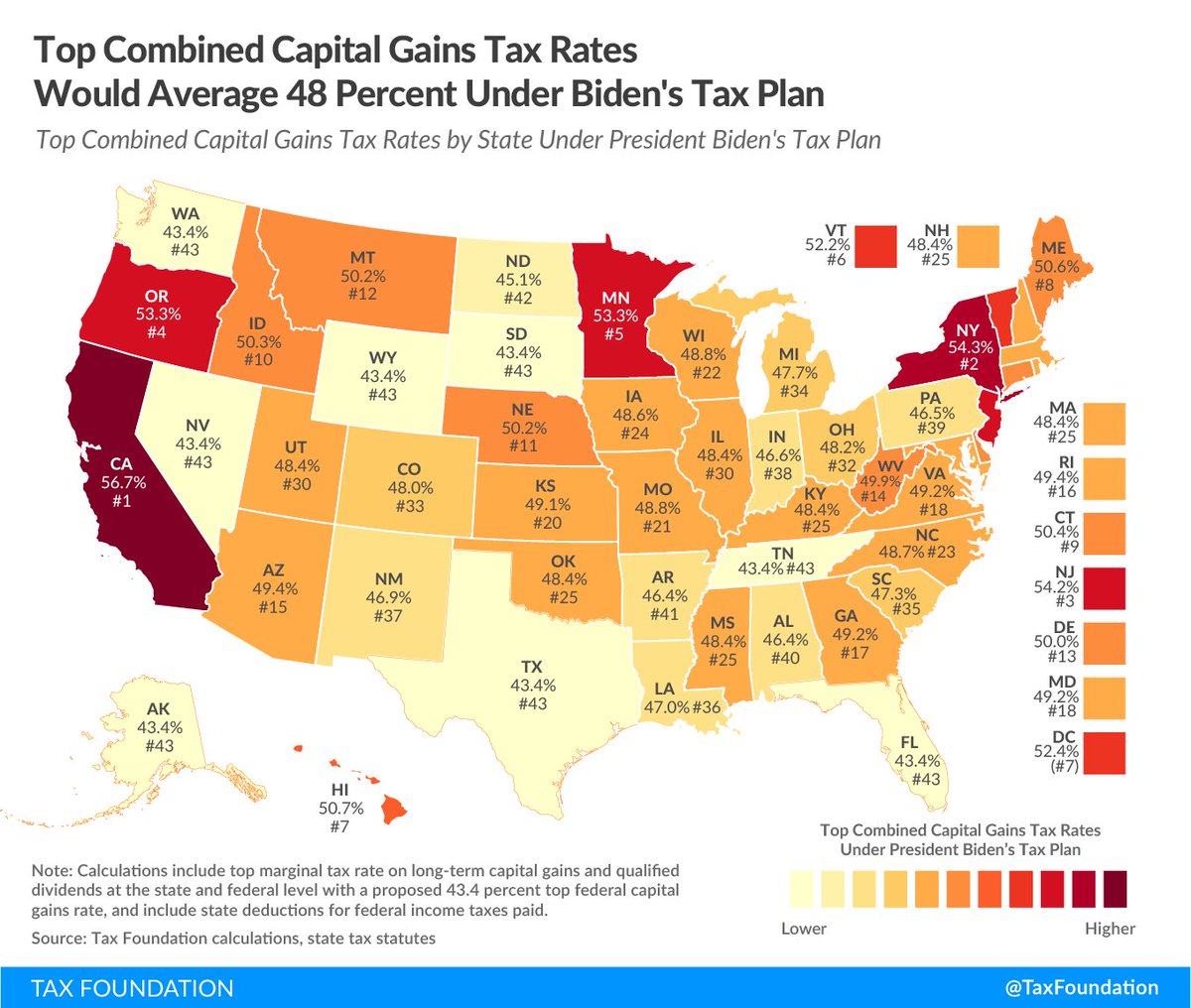

Since the Biden administration unveiled its proposal for increased infrastructure spending in the American Jobs Plan, debate over how to fund investments in infrastructure has taken center stage.

taxfoundation.org/biden-infrastr…

taxfoundation.org/biden-infrastr…

A similar discussion is happening in many states, where lawmakers are grappling with questions over the future of infrastructure revenue and spending.

taxfoundation.org/road-funding-v…

taxfoundation.org/road-funding-v…

Among developments in vehicles’ fuel economy, increased sales of electric vehicles, and inflation, taxes on motor fuel generally raise less revenue per vehicle miles traveled (VMT) than they did in the past.

As a result, most states contribute revenue from other sources to make up differences between infrastructure revenue and expenditures.

With the sustainability of established motor fuel taxes increasingly threatened, it may be time for lawmakers at both state and federal levels to consider other options for transportation revenue.

One such option is a vehicle miles traveled (VMT) tax.

taxfoundation.org/road-funding-v…

One such option is a vehicle miles traveled (VMT) tax.

taxfoundation.org/road-funding-v…

A few states have already begun pilot programs to study the feasibility of VMT taxes, and Pennsylvania Gov. Tom Wolf (D) recently announced a commission to study phasing out motor fuel taxes.

taxfoundation.org/pa-gas-tax-gov…

taxfoundation.org/pa-gas-tax-gov…

On both a federal and a state level, imposing a vehicle miles traveled (VMT) tax does require lawmakers to make some hard decisions on trade-offs.

Significant concerns regarding privacy must be addressed and balanced against a desire for a targeted, equitable, and efficient tax.

Significant concerns regarding privacy must be addressed and balanced against a desire for a targeted, equitable, and efficient tax.

• • •

Missing some Tweet in this thread? You can try to

force a refresh