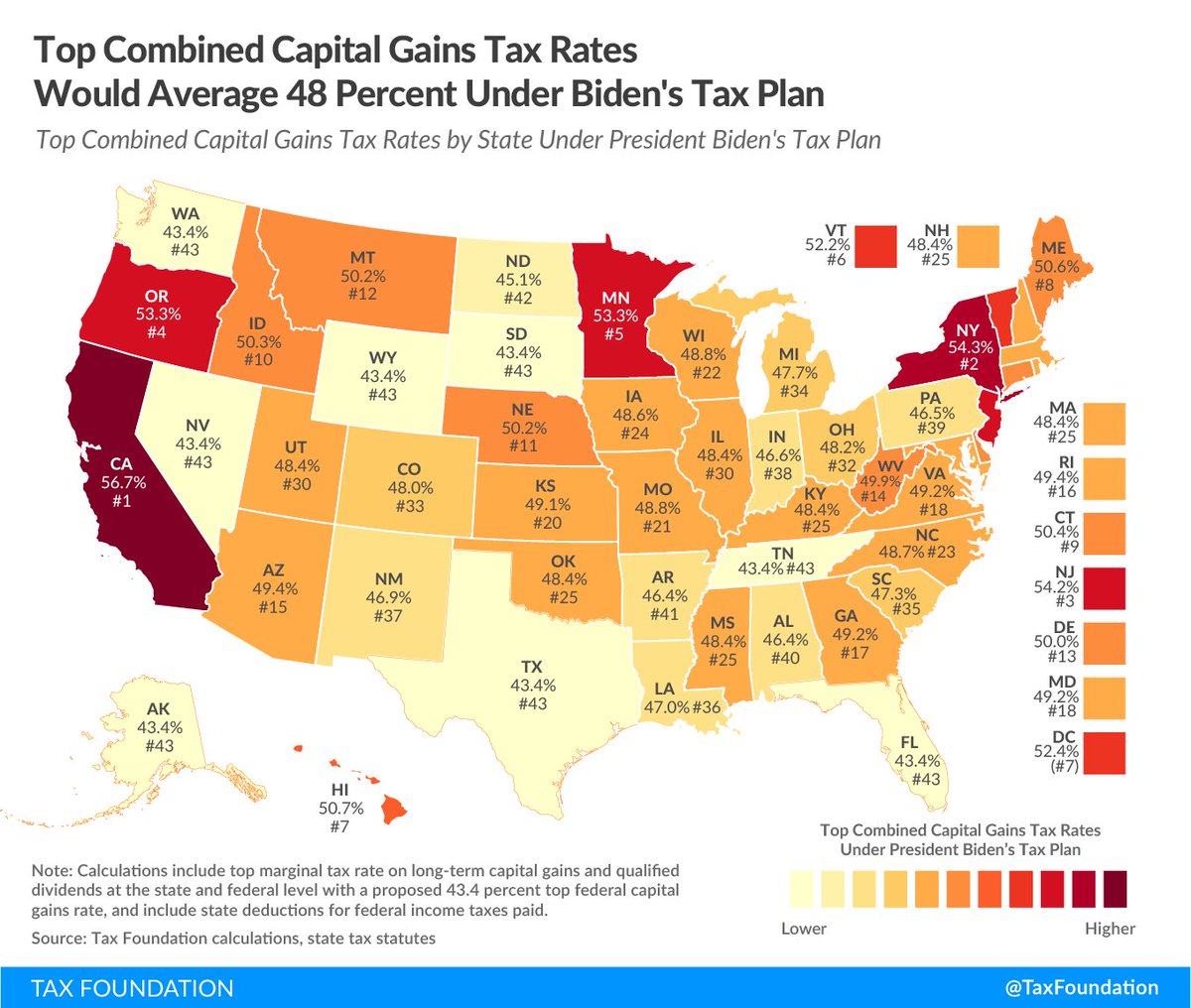

Top combined capital gains tax rates under President Biden’s tax plan:

56.7% -- California

54.3% -- New York

54.2% -- New Jersey

53.3% -- Oregon

53.3% -- Minnesota

taxfoundation.org/biden-capital-… @ericadyork @GS_Watson

56.7% -- California

54.3% -- New York

54.2% -- New Jersey

53.3% -- Oregon

53.3% -- Minnesota

taxfoundation.org/biden-capital-… @ericadyork @GS_Watson

President Biden’s #AmericanFamilyPlan will likely include a large increase in the top federal tax rate on long-term capital gains and qualified dividends, from 23.8% today to 39.6% for higher earners.

When including the net investment income tax, the top federal rate on capital gains would be 43.4%. Rates would be even higher in many U.S. states due to state and local capital gains taxes, leading to a combined average rate of nearly 49% compared to about 29% under current law.

Most states levy their individual income tax rates on long-term capital gains and qualified dividends, though Hawaii levies lower tax rates. The average top tax rate on capital gains at the state level is about 5.4%, for a combined average rate of 29.2% current law.

15 states and D.C. would have a top combined capital gains tax rate north of 50%. California, New York, and New Jersey would have combined rates of more than 54 percent.

Top combined rates in some localities would go even higher. For example, New York City levies a local capital gains rate of 3.876%, which means an investor would pay an all-in rate of nearly 58.2%. Residents of Portland, Oregon would face a top capital gains rate of 57.3%.

Raising the top capital gains tax rate to 39.6 percent for those earning over $1 million would reduce long-run GDP by about 0.1 percent and reduce federal revenue by about $124 billion over 10 years, according to the Tax Foundation General Equilibrium Model.

• • •

Missing some Tweet in this thread? You can try to

force a refresh