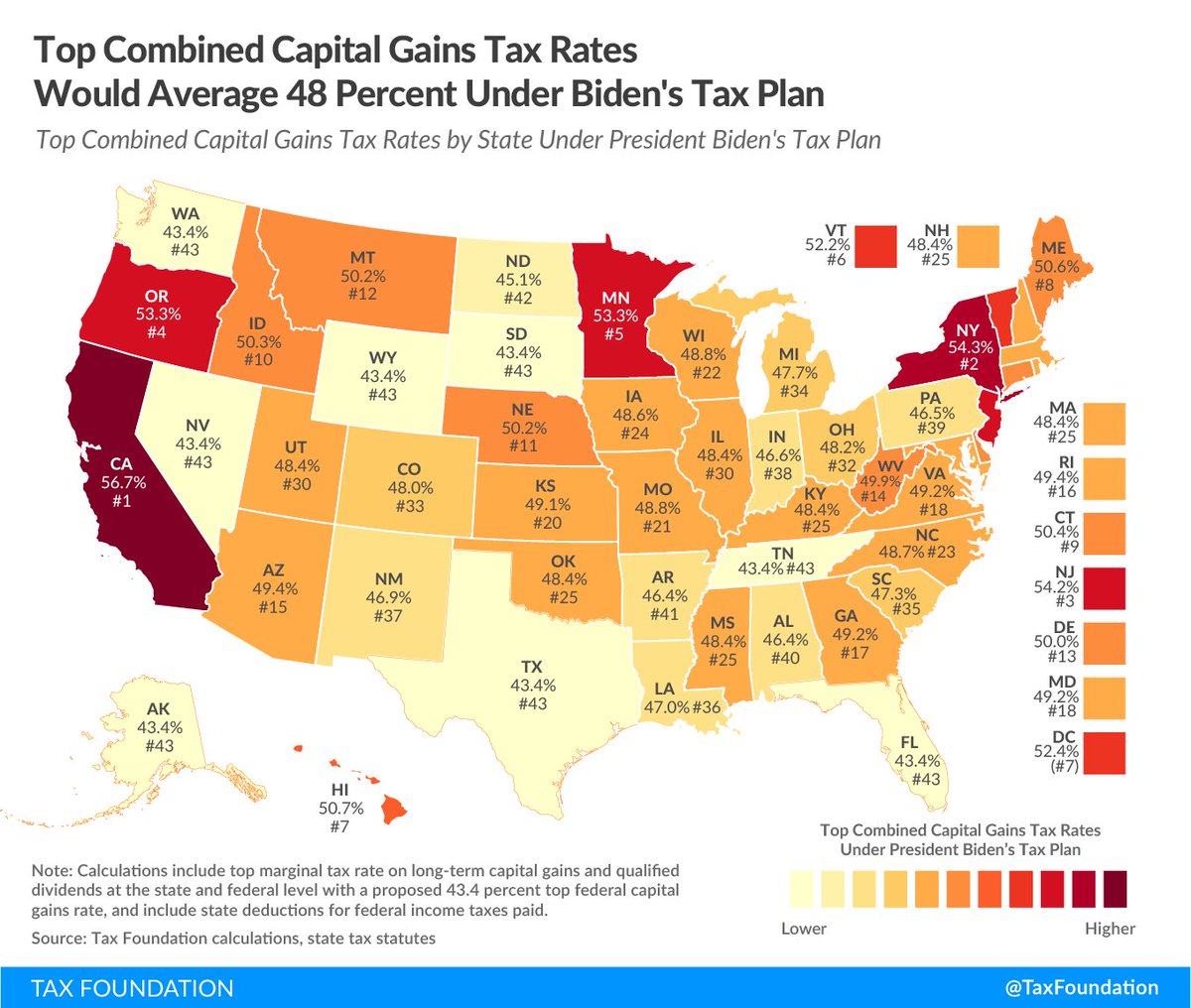

Raising the U.S. corporate tax rate to 28 percent would reduce GDP by $720 billion over ten years: analysis buff.ly/3n62Bsu @ericadyork

In our new book, Options for Reforming America’s Tax Code 2.0, we illustrate the economic, distributional, and revenue trade-offs of 70 tax changes, including President Biden’s proposal to increase the corporate tax rate to 28 percent.

taxfoundation.org/tax-reform-opt…

taxfoundation.org/tax-reform-opt…

The Options guide presents the economic effects we estimate would occur in the long term (20-30 years from now), but we can also model the cumulative effects of a policy change—providing more context about how the effects of a higher corporate income tax rate compound over time.

We estimate that increasing the U.S. corporate rate to 28 percent would, in the long run, lead to 138,000 fewer FTE jobs.

A significant portion of the economic cost of the corporate tax falls on workers.

In the long term, we estimate that taxpayers in the bottom quintile would see their after-tax incomes drop by 1.5%.

In the long term, we estimate that taxpayers in the bottom quintile would see their after-tax incomes drop by 1.5%.

Like the decrease in economic output, declines in after-tax income would accumulate over time.

While the percentage change in after-tax income is the right way to measure tax changes by income group—it creates the most accurate representation of the change in the distribution of the tax burden—we can also look at the average tax change in dollars.

On a conventional basis, which does not factor in the negative effect of the corporate tax increase, after-tax income accumulated over 10 years for the bottom quintile would drop by an average of $550 (the decline increases to $740 when factoring in the smaller economy).

According to OECD economists, corporate income taxes are one of the most harmful ways to raise revenue.

They place a higher burden on investment, reduce economic output, and reduce after-tax incomes across the income spectrum—negative economic effects that compound over time.

They place a higher burden on investment, reduce economic output, and reduce after-tax incomes across the income spectrum—negative economic effects that compound over time.

• • •

Missing some Tweet in this thread? You can try to

force a refresh