KPIT Technologies concall was today at 4:00 pm

Here are the concall highlights 😀

Here are the concall highlights 😀

Business Updates:

• Revenue drop YoY, however volumes is same.

• Autonomous driving trend is long term trend which requires software for multiple use.

• Shared Mobility is also showing good trend. For this vehicle replacement with software inbuilt can be seen.

• Revenue drop YoY, however volumes is same.

• Autonomous driving trend is long term trend which requires software for multiple use.

• Shared Mobility is also showing good trend. For this vehicle replacement with software inbuilt can be seen.

• Company has made strategies to intake efficient employees

• Company focus is to attract few clients but to have very long term plan with those customers.

• Company focus is to attract few clients but to have very long term plan with those customers.

Deals and Pipelines:

• Pipeline has been increased at highest in the last quarter, which is across the region and verticals.

• Electric Power train has grown marginally, but company expect much of the growth to be coming from Electric Power train.

• Got few deals in OEM

• Pipeline has been increased at highest in the last quarter, which is across the region and verticals.

• Electric Power train has grown marginally, but company expect much of the growth to be coming from Electric Power train.

• Got few deals in OEM

Revenue Share and Margin:

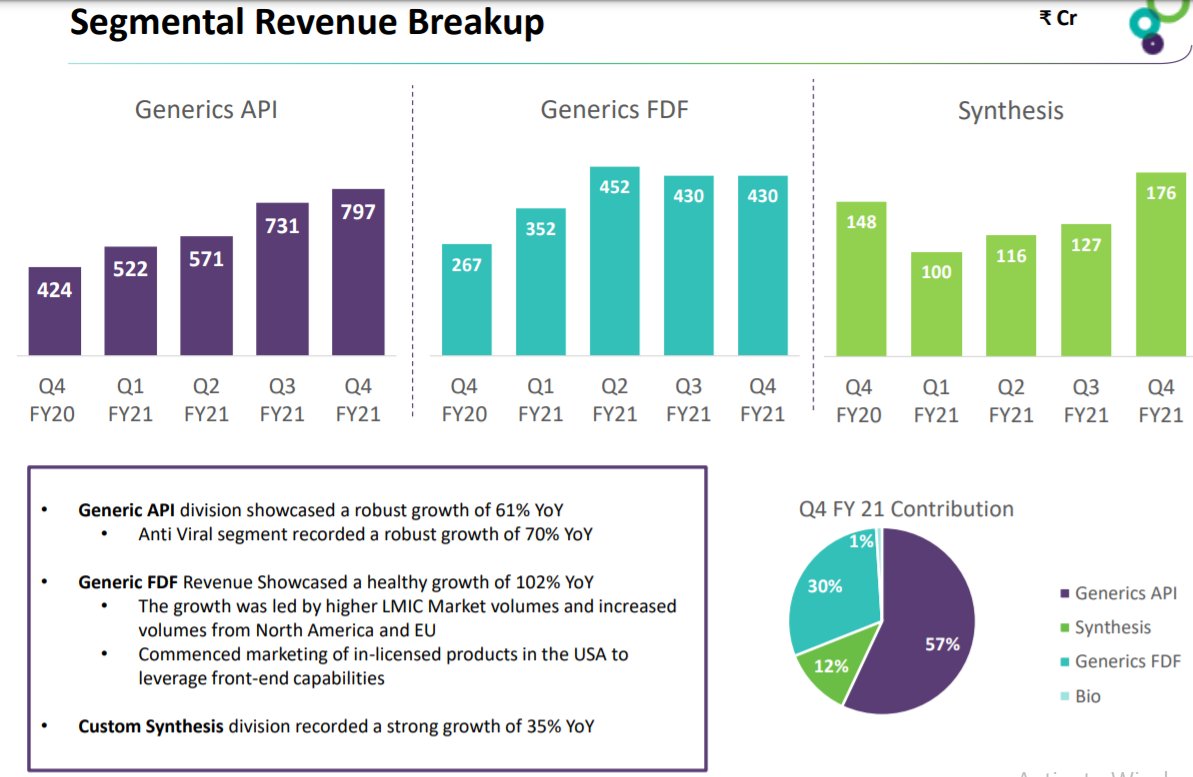

• Revenue Share of quarter in image

• Offshoring is expected to be increasing and company is looking for margins improvement.

• Fixed PRice engagement have gone up for productivity side, and company is expected to see growth productivity as well.

• Revenue Share of quarter in image

• Offshoring is expected to be increasing and company is looking for margins improvement.

• Fixed PRice engagement have gone up for productivity side, and company is expected to see growth productivity as well.

Competitive Landscape:

• There are companies are like Luxoft in Software and technology, and there are certain OEM who wants to own the software.

• Company is working in Tier 1, with their own software.

• Current Run rate is 12%.

• There are companies are like Luxoft in Software and technology, and there are certain OEM who wants to own the software.

• Company is working in Tier 1, with their own software.

• Current Run rate is 12%.

Focus:

• Company is engage with semiconductor companies for software past (some software called middle ware).

• Semi Conductor will not be the direct customer but this can be helpful for indirectly connecting with OEM

• Company is engage with semiconductor companies for software past (some software called middle ware).

• Semi Conductor will not be the direct customer but this can be helpful for indirectly connecting with OEM

Commercial Vehicle (CV):

• Growth in electrification in CV and the area of focus remains the same as other vehicle.

• On Autonomous vehicle company has strong focus, as area of scope is wide.

• Company don't see any softness in the autonomous side. Both domestic and export.

• Growth in electrification in CV and the area of focus remains the same as other vehicle.

• On Autonomous vehicle company has strong focus, as area of scope is wide.

• Company don't see any softness in the autonomous side. Both domestic and export.

T25 Clients:

• These are designated client where company investment over more on the long term contracts with customer. Company is do seeing adding and improving these client list as well.

• These are designated client where company investment over more on the long term contracts with customer. Company is do seeing adding and improving these client list as well.

Risk on Software:

• It is similar to that of software development.

• Main focus remains on quality of product.

• Company has focus of defect free delivery.

• It is similar to that of software development.

• Main focus remains on quality of product.

• Company has focus of defect free delivery.

For more discussion on Equity analysis

Subscribe to our YouTube channel 😃

Link 🔗: youtube.com/channel/UCDmd6…

Subscribe to our YouTube channel 😃

Link 🔗: youtube.com/channel/UCDmd6…

• • •

Missing some Tweet in this thread? You can try to

force a refresh