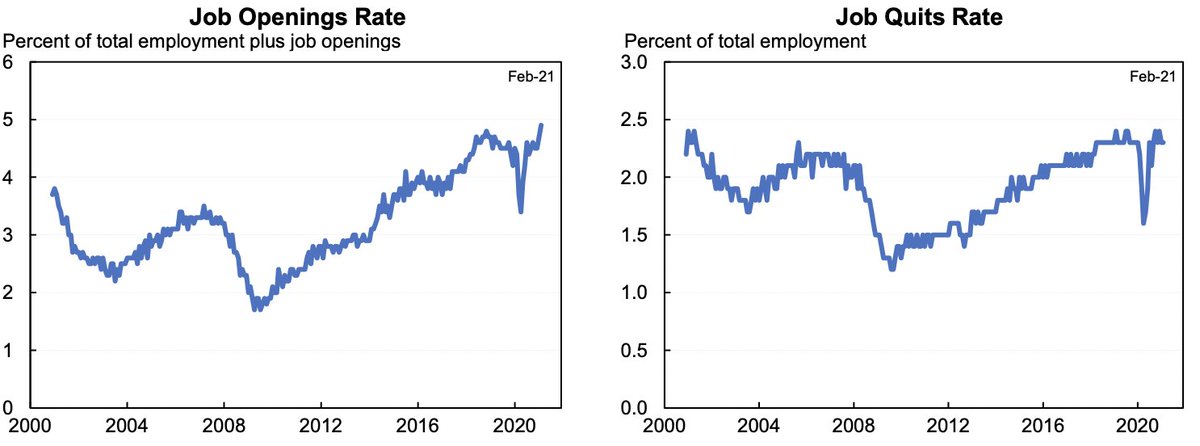

I spent a lot of time swatting down the counterintuitive stories about labor shortages in the aftermath of the Great Recession.

But it is different now: post Great Recession wage growth was 2pp below what it was pre-Great Recession. Now wage growth is equal to pre-pandemic.

But it is different now: post Great Recession wage growth was 2pp below what it was pre-Great Recession. Now wage growth is equal to pre-pandemic.

https://twitter.com/hshierholz/status/1389574486584815617

You see this especially in the distribution of wages. The first quartile of workers had extremely low wage growth in 2011-14 but have particularly high wage growth now. atlantafed.org/chcs/wage-grow…

Moreover, these data only go through March and as @arindube has pointed out there is a lot of intertia in the data. So would not expect to see a lot of increase yet.

The labor market right now is complex, many different parts. But fighting the same post-Great Recession battles misses a lot of what is going on right now.

• • •

Missing some Tweet in this thread? You can try to

force a refresh