The spark behind the birth of Vanguard passed away earlier this month, aged 88. Nick Thorndike might not be as famous as Jack Bogle, Vanguard’s actual founder, but he (inadvertently) played a pivotal role in its genesis. Short thread of recondite financial history: 1/n

Back in the 1950s, Nick Thorndike was a precocious fund manager at Fidelity, mentored by Ned Johnson himself. In 1960 he and three Bostonian friends set up their own shop, Thorndike, Doran, Paine and Lewis, which kicked arse in the “go-go” boom of the 1960s.

The go-go years were much tougher for more conservative investment groups, such as Walter Morgan’s Wellington. It ran a big, successful bond-and-stocks fund, but in the 60s boom people wanted GROWTH, not a boring “balanced” fund.

Under a wonderboy executive called John Clifton Bogle, Wellington had in 1958 launched a pure stock fund. This would eventually be called Windsor and be managed by John Neff, an absolute legend of the investment industry. But Wellington's mutual fund market share kept falling.

So in 1965 Morgan and Bogle went for a Hail Mary. They merged Wellington with a bunch of hotshot money managers in Boston – Thorndike’s TDP&L. (from Bogle's biography)

And initially it looked like the marriage of the Bostonians investing nous and Wellington’s brand distribution would be a huge success. Here’s an Institutional Investor cover from the time, depicting Bogle as a quarterback handing footballs over to the young "whiz kids" of TDP&L.

But when the go-go era fizzled out, many of the merged group’s funds started bombing. Personality clashes between the headstrong Bogle and the more consensual Thorndike and Robert Doran turned into full-scale warfare.

Eventually, the Boston partners – who by then controlled a majority of Wellington Management Company’s board – teamed up and voted to fire Bogle as chief executive on January 23, 1974.

But Bogle refused to give up. US mutual funds have to have separate, nominally independent boards, and the Bostonians led by Thorndike and Doran didn’t control a clear majority on the Wellington funds’ board.

So the very next day after his humiliating defenestration, Bogle pitched the funds that they should acquire Wellington, de facto mutualise themselves and reinstate him as chief executive.

This was a bridge too far, given the likelihood of legal challenges. So the funds’ board instead voted for Bogle’s weakest option – setting up an administrative unit owned by the funds themselves, which would mostly do clerical work.

Bogle had no intention of being a glorified clerk, and gave the new company a grandiose name: The Vanguard Group of Investment Companies. Over the next few years he gradually turned it into a fully-fledged investment company that would ultimately grow to manage over $7tn today.

Why do I say that Thorndike was the inadvertent spark behind the birth and growth of Vanguard? Because the humiliation of his sacking by Wellington - and a burning desire to stick it to his Boston nemeses - was vital fuel for Bogle’s already thermonuclear drive.

That said, I don’t want to relegate Thorndike’s life into a footnote in the Saga of Bogle. As this obituary makes clear, legacy.com/obituaries/bos… he played a huge role in the Welllington turnaround, and chaired Massachusetts General Hospital after retiring from there.

Bogle, Thorndike and Doran also eventually made up, after Bogle came across the story of John Adams and Thomas Jefferson’s late-life friendship after a long period of bitter political enmity.

I think the message is that mistakes can prove to be salvations, enemies may actually make you, and enmities don't have to be eternal. And if you thought this is kinda neat and interesting, pls check out this. amazon.com/dp/0593087682

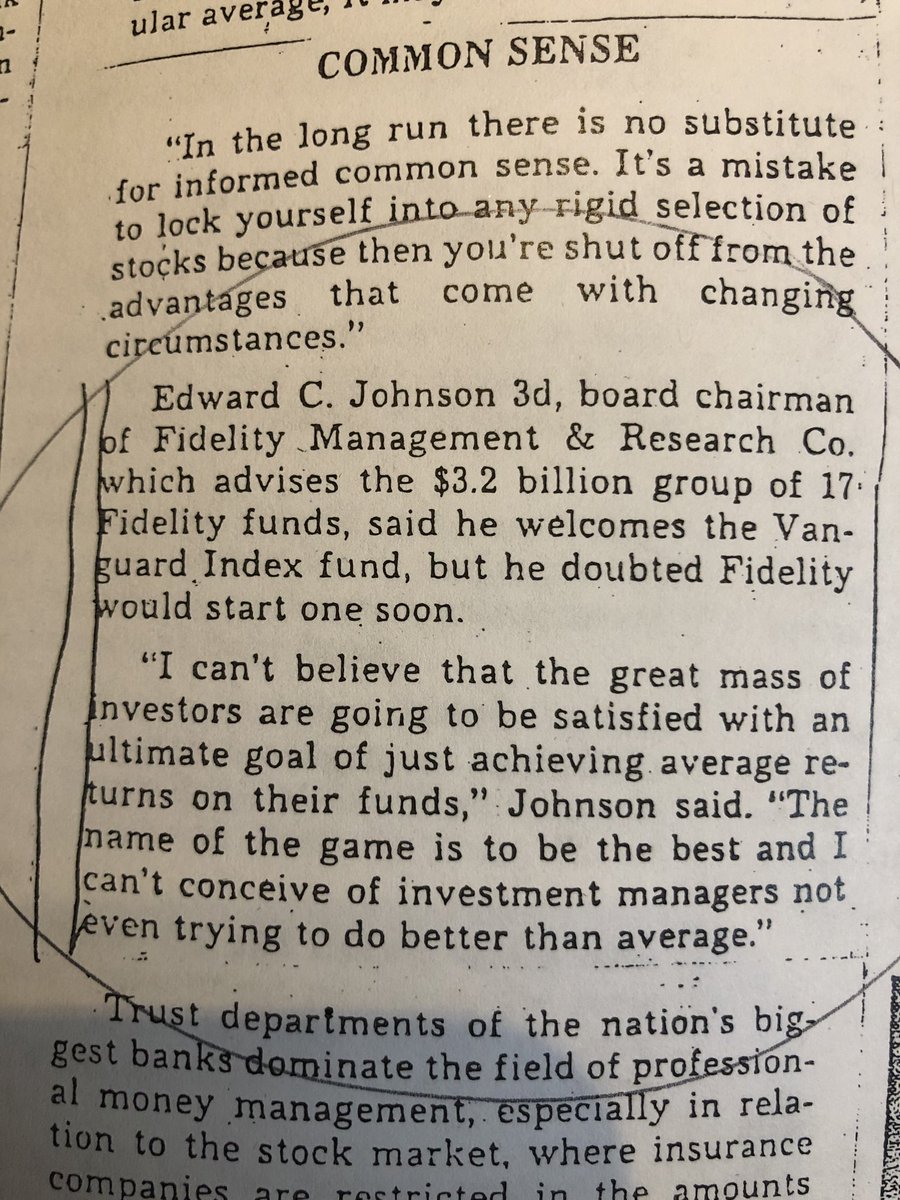

Btw this is how quants were seen back in the 1960s.

• • •

Missing some Tweet in this thread? You can try to

force a refresh