Cloudflare $NET recently participated in JP Morgan's Tech conference.

The CEO @eastdakota used this opportunity to really highlight the TRUE identity of Cloudflare and discussed some of their profound competitive advantage.

Here are 8-important takeaways for Investors:

The CEO @eastdakota used this opportunity to really highlight the TRUE identity of Cloudflare and discussed some of their profound competitive advantage.

Here are 8-important takeaways for Investors:

1/ $NET is purposely not a Usage-Based Business Model:

Only about 5% of $NET is usage-based bcos of the potential impact or harm to a customer if some emergency came up.

Over 90% of revenue is subscriptions which gives great revenue visibility & sustains revenue

I like this.

Only about 5% of $NET is usage-based bcos of the potential impact or harm to a customer if some emergency came up.

Over 90% of revenue is subscriptions which gives great revenue visibility & sustains revenue

I like this.

2/ $NET's business model & strategic focus (compared to $FSLY or $AKAM):

$NET has pivoting from becoming a "CDN provider that cares about speed of streaming event"

Into

More of a security company and network ecosystem that protects their customers entire network. This is key.

$NET has pivoting from becoming a "CDN provider that cares about speed of streaming event"

Into

More of a security company and network ecosystem that protects their customers entire network. This is key.

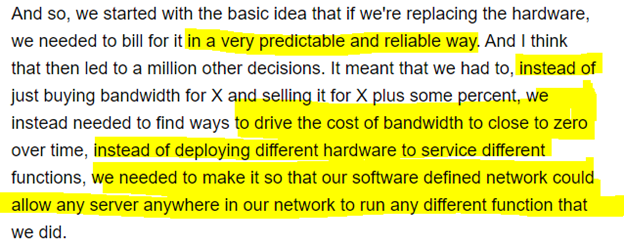

3/ Software Defined Network (SDN)

This is likely the biggest moat that many ignore! Well done @zatlyn & @eastdakota

$NET has an advanced SDN. It was built from Day-1 to make $NET extremely asset light requiring less servers & led to high margins

More on this in a future thread

This is likely the biggest moat that many ignore! Well done @zatlyn & @eastdakota

$NET has an advanced SDN. It was built from Day-1 to make $NET extremely asset light requiring less servers & led to high margins

More on this in a future thread

4/ $NET benefits from Cybersecurity Tailwinds

It's not explicit below but due to $NET's Zero trust (ZT) security & their move into SASE networks, they stand to become one of the beneficiaries of the Biden security executive plan - Including attracting major enterprise customers.

It's not explicit below but due to $NET's Zero trust (ZT) security & their move into SASE networks, they stand to become one of the beneficiaries of the Biden security executive plan - Including attracting major enterprise customers.

5/ $NET's true identity:

They are a network company at heart - building security features to make a network reliable.

He noted, we shouldn't compare them to $FSLY (CDN), $CRWD (End-point protection) or $OKTA (identity access) due to their different approach. They're partners!

They are a network company at heart - building security features to make a network reliable.

He noted, we shouldn't compare them to $FSLY (CDN), $CRWD (End-point protection) or $OKTA (identity access) due to their different approach. They're partners!

6/ Their biggest competitor-> $AMZN

$AMZN's Cloudfront is the CEO's biggest threat.

Why? - They have extensive resources than $NET could ever deploy.

However, most companies are using multi-cloud strategies and $NET is closer to developers - so this is how $NET stays relevant

$AMZN's Cloudfront is the CEO's biggest threat.

Why? - They have extensive resources than $NET could ever deploy.

However, most companies are using multi-cloud strategies and $NET is closer to developers - so this is how $NET stays relevant

7/ $NET's Edge Compute Platform:

Beyond cybersecurity, Workers is the most exciting product for investors.

The biggest value add of Edge besides speed, is that $NET can build organic products and ensure data regional compliance for businesses. There are even many more use-cases

Beyond cybersecurity, Workers is the most exciting product for investors.

The biggest value add of Edge besides speed, is that $NET can build organic products and ensure data regional compliance for businesses. There are even many more use-cases

8/ $NET's real advantage!

i) Low Unit Economics due to their SDN Tech -> leads to higher margins

ii) Brand leads to Low CAC: Due to their freemium model, they are closer to more developers and can use this advantage for testing new products

iii) Culture of Innovation machines!

i) Low Unit Economics due to their SDN Tech -> leads to higher margins

ii) Brand leads to Low CAC: Due to their freemium model, they are closer to more developers and can use this advantage for testing new products

iii) Culture of Innovation machines!

9/Summary:

1⃣ Subscription based b-model has worked great

2⃣ $NET has pivoted from being CDN to a network cybersecurity provider

3⃣ SDN Technology architecture is a key moat behind everything

4⃣ Major beneficiary from Biden's security executive order due to their ZT security

..

1⃣ Subscription based b-model has worked great

2⃣ $NET has pivoted from being CDN to a network cybersecurity provider

3⃣ SDN Technology architecture is a key moat behind everything

4⃣ Major beneficiary from Biden's security executive order due to their ZT security

..

10/ Summary (2):

5⃣ $NET's true identity is about creating partnerships.

6⃣ $AMZN is the biggest threat

7⃣ Edge Compute offers much more than speed

8⃣ $NET's moat is Low CAC, Asset light tech and the culture.

I'll be creating another thread to connect this! @InvestiAnalyst

END/

5⃣ $NET's true identity is about creating partnerships.

6⃣ $AMZN is the biggest threat

7⃣ Edge Compute offers much more than speed

8⃣ $NET's moat is Low CAC, Asset light tech and the culture.

I'll be creating another thread to connect this! @InvestiAnalyst

END/

• • •

Missing some Tweet in this thread? You can try to

force a refresh