Trouble came & went in 2020 in one of the most Epic Downturns…& Bank Capital proved Super Resilient.

https://twitter.com/kamiller1/status/1405523339481804815

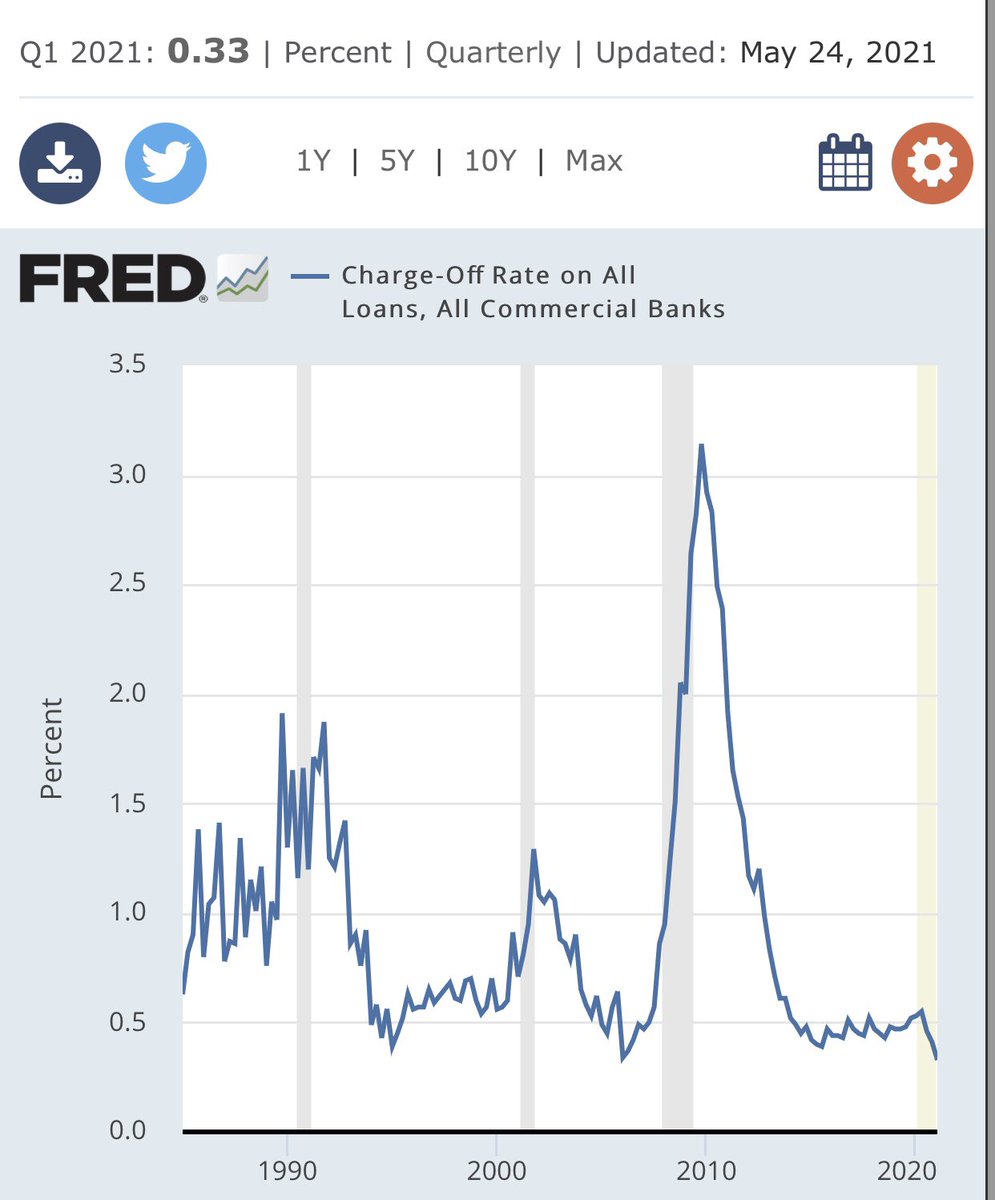

That’s not to say there’s not going to be some Tail in Credit Losses/NCOs rising from now such epically low levels will be close to nothing in 2021… partly coz of Stimmy.. but people forget $2Trillion in XS Savings isn’t all Stimmy.. Regardless the Insane amount of Loss Reserves

that r already built into Capital coz of actions taken to their P&L & BS getting smashed in 1H20 coz of CECL Pulling Forward Loan Loss Reserves for “Lifetime Losses” vs previous “Incurred next 12 months Loss” regime is what killed Banks & Market on Build in 1H20 but also swift V.

NCOs may rise off floor in 2H22 (180 days Post DQs), but not even remotely close to level of reserves they have on now.. so when NCOs rise they will deplete some level of Reserves that currently still reflect 12-15% Unemployment despite fact we are at 6%. Capital Keeps Building.

Fiscal Stimulus & Public Debt has absorbed a huge amount of the traditional private credit losses…that has accrued to the Consumer & as a result Banks…that’s coz of a Global Pandemic.. now one could easily make the argument… these loss reserves shouldn’t have been this high..

…Banks took huge Income Statement & Balance Sheet pain in 1H20 - Coz the Government “FORCED” the Shutdown of the economy… Sustained Lockdowns now have proven to be a Big Mistake.

• • •

Missing some Tweet in this thread? You can try to

force a refresh