As investors & companies globalize, we recognize that risk varies across countries for many reasons, and the need to incorporate that "country risk" into decisions. My seventh annual update on country risk is here: bit.ly/3ylZ8dK, with data here: bit.ly/3jEHP3m

1. Corruption: The roots of corruption don't lie in cultures, but in systems (over regulated regimes, with underpaid rule enforcers), but corruption is an implicit tax, and its effects varies widely across the world. Paper: bit.ly/3ylZ8dK & data: bit.ly/3jEHP3m

2. Violence: Operating a business in the midst of violence, from within or outside, is riskier than in peace. The threat of that violence is higher in some parts of world than others. Paper: bit.ly/3ylZ8dK & data: bit.ly/3jEHP3m

3. Property rights: For businesses to survive and thrive, property rights need to be enforced, and they are more strongly in some parts of the world than others. Paper: bit.ly/3ylZ8dK & data: bit.ly/3jEHP3m

Measuring country risk is complex, but entities do try. I use @PRS_Group measure of composite country risk to capture differences across the world. Paper: bit.ly/3ylZ8dK & data: bit.ly/3jEHP3m

Market measures of country risk are narrowly focused on lenders & investors, but they are correlated with other risk measures. My updated equity and country risk premiums from July 2021, with Moody's ratings. Paper: bit.ly/3ylZ8dK & data: bit.ly/3jEHP3m

Company exposure to country risk comes from where it operates. It is lazy & dangerous to assume that a company is only exposed to the risk of its country of incorporation. Paper: bit.ly/3ylZ8dK & data: bit.ly/3jEHP3m

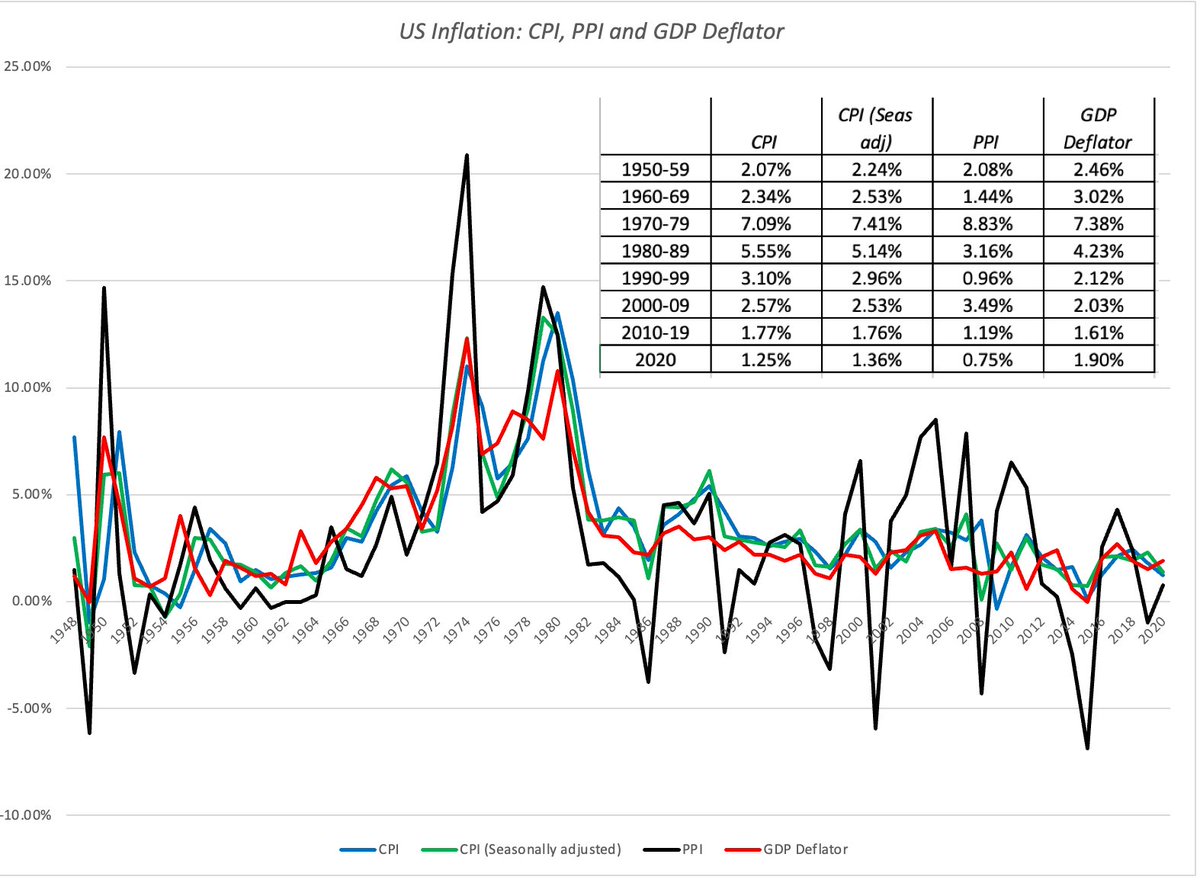

Currencies are more reflections of underlying risk, than sources of risk. Ultimately, it is inflation & real growth differentials that drive currency levels, changes over time and volatility. Paper: bit.ly/3ylZ8dK & data: bit.ly/3jEHP3m

• • •

Missing some Tweet in this thread? You can try to

force a refresh