Survey: What is the best type of aggregator e-mails?

Genuinely curious what people enjoy reading the most

Genuinely curious what people enjoy reading the most

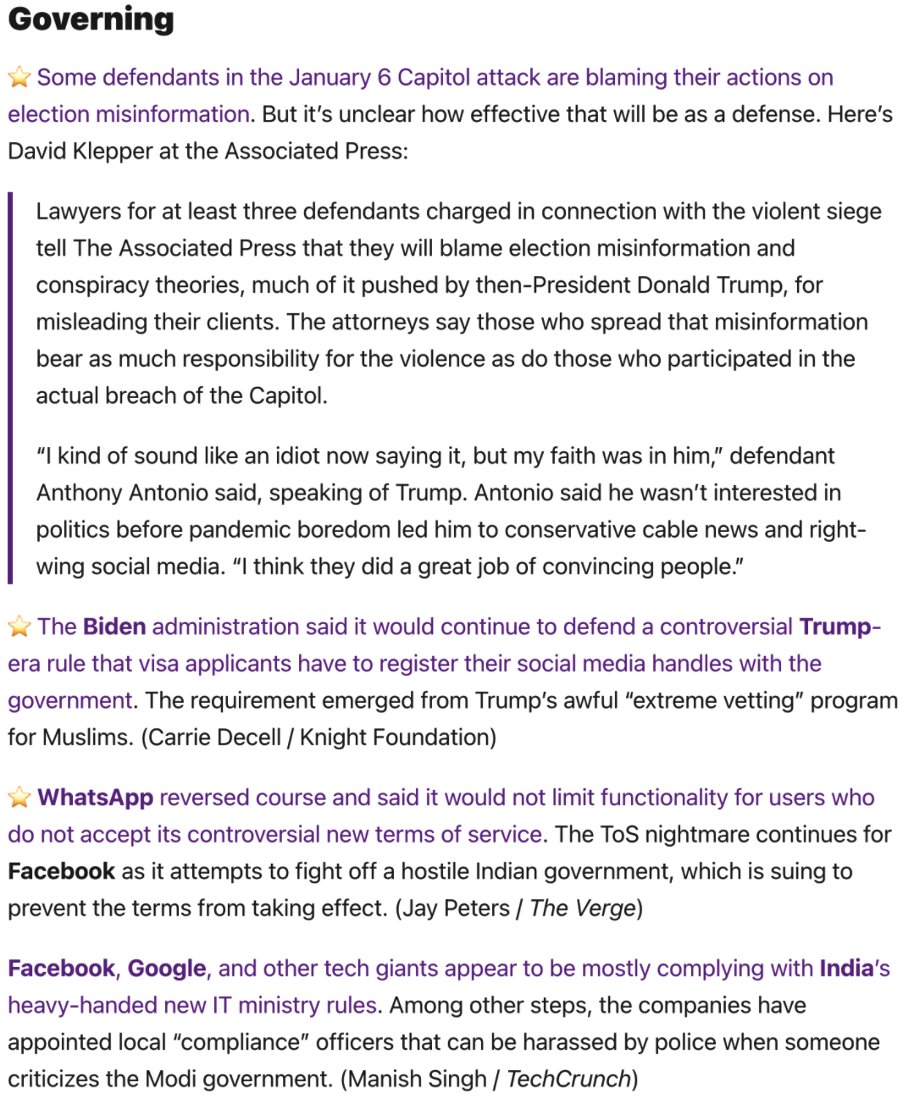

Platformer:

Long text with detailed descriptions that save you from clicking the link

Long text with detailed descriptions that save you from clicking the link

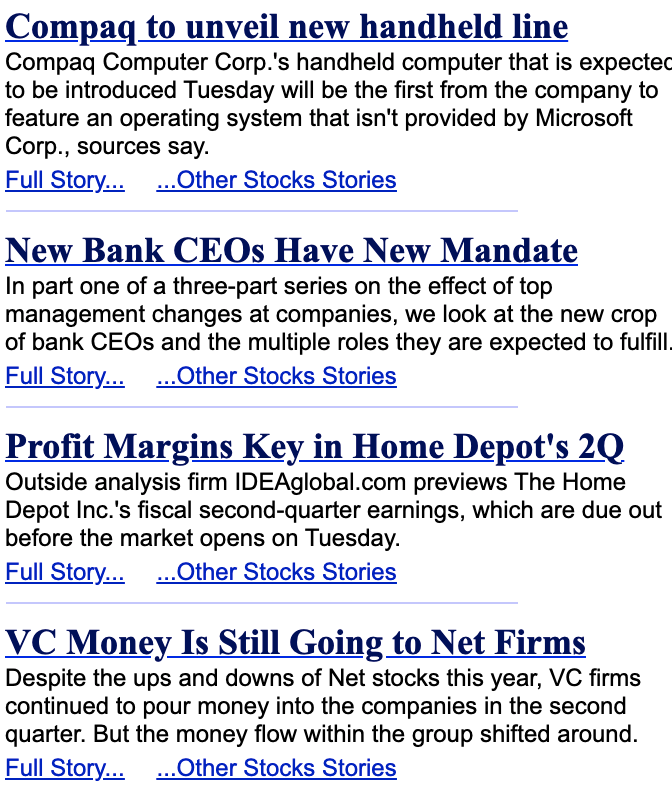

The Diff:

Top five or so articles, plenty of text to describe why they've been chosen

Top five or so articles, plenty of text to describe why they've been chosen

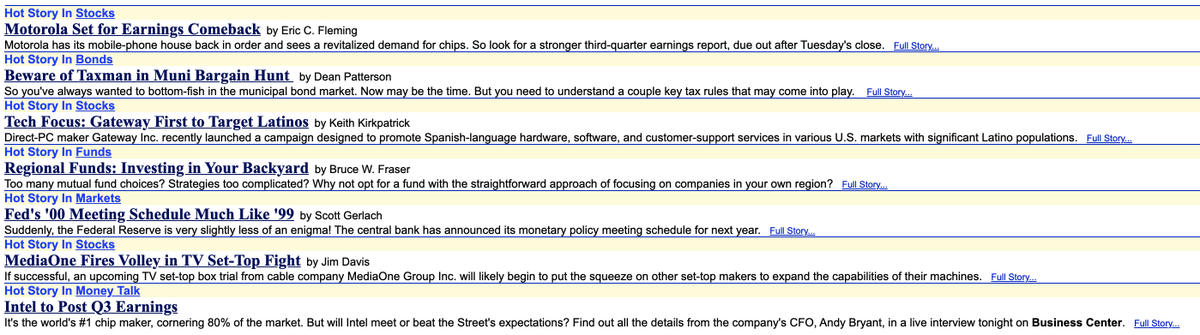

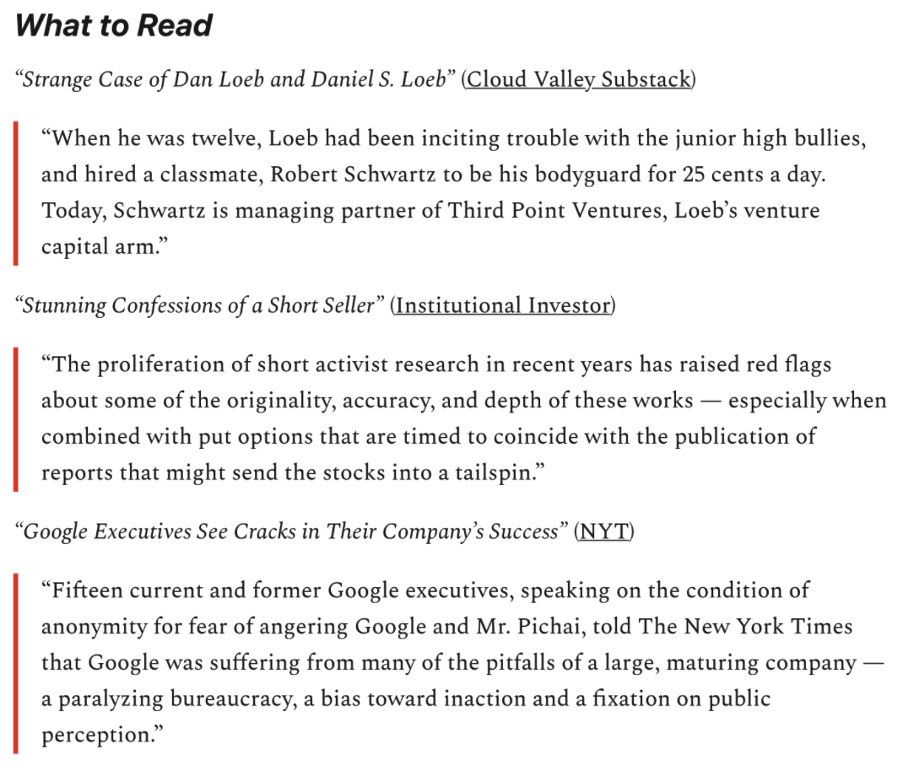

The Bear Cave:

Just a few articles with key quotes for each

Just a few articles with key quotes for each

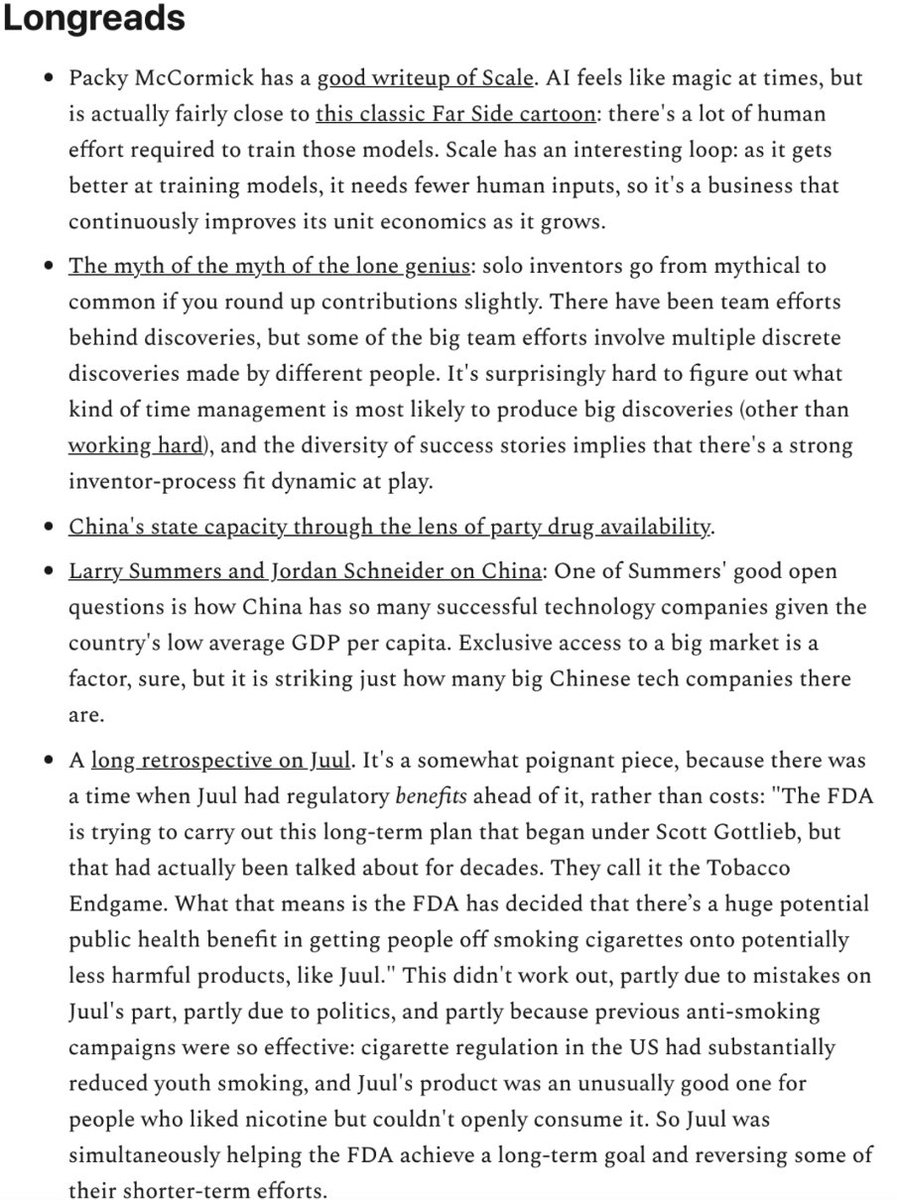

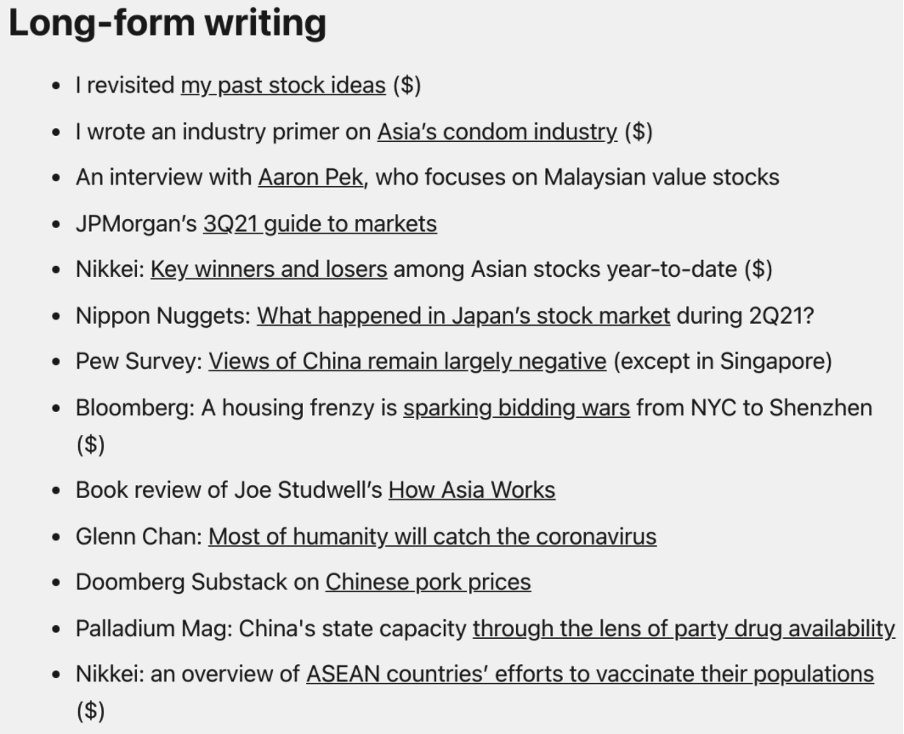

Asian Century Stocks (so far):

Quick bullet points, but many of them

Quick bullet points, but many of them

• • •

Missing some Tweet in this thread? You can try to

force a refresh