Let's Understand why Narrative is important in investing and how to create a Thesis that can help you to hold a stock in spite of the market environments

Time for a thread with international and Indian examples, Please retweet so that everyone can benefit 🧵🧵🧵🧵

Time for a thread with international and Indian examples, Please retweet so that everyone can benefit 🧵🧵🧵🧵

The world we see and defined is given meaning by the words we choose to use. In short, the world is what we make of it. Something similar applies to creating a thesis before investing in a stock. Your thesis is what makes you hold a stock thick and through in spite of bull/bear

Example 1: Amazon- In May 1997, Amazon became a publically listed business. The target price set by analysts was $18 per share. It finished its first day at $23 per share. (So much for targets). In 1999, in the middle of the tech bubble. Same stock was trading at $100 per share.

Analysts were giving targets of $300 per share. However, after the collapse of the bubble many internet businesses went bust, but Amazon survived in spite of a 78% drop from 1999 highs. As we all know, Price changes perception. Same analysts started claiming it was massively

overpriced and claimed its days were "numbered". By the end of 2002, it was trading at 90times cash flow (so much for multiples to account for future)

This is where the beauty of narratives in a thesis play a part:

1)The Bears argued that the Amazon was a book retailer and should be seen as one. Thus, it was overvalued compared to Barnes&Nobles. Later they compared it with Walmart and concluded it was more expensive relatively

1)The Bears argued that the Amazon was a book retailer and should be seen as one. Thus, it was overvalued compared to Barnes&Nobles. Later they compared it with Walmart and concluded it was more expensive relatively

2) The Bulls saw something differently, they claimed that the company wasn't just a books retailer it was but had successfully diversified into DVDs, CDs,Computer softwares etc. They saw it as a comparable to Dell Computer. Both the businesses operated on negative

working capital i.e. they get money before from their customers before they even have to pay their suppliers. Mind you, dell was a 78 bagger between 1995-1999. Both were taking orders online and both didn't need to have a costly sales force.

This arguement shocked the bears. In reality this is how most of the thesis are formulated. There is a bullish side and there is a bearish side. Your thesis and conviction at the end depends upon the words that you use to describe a business and your ability to recalibrate

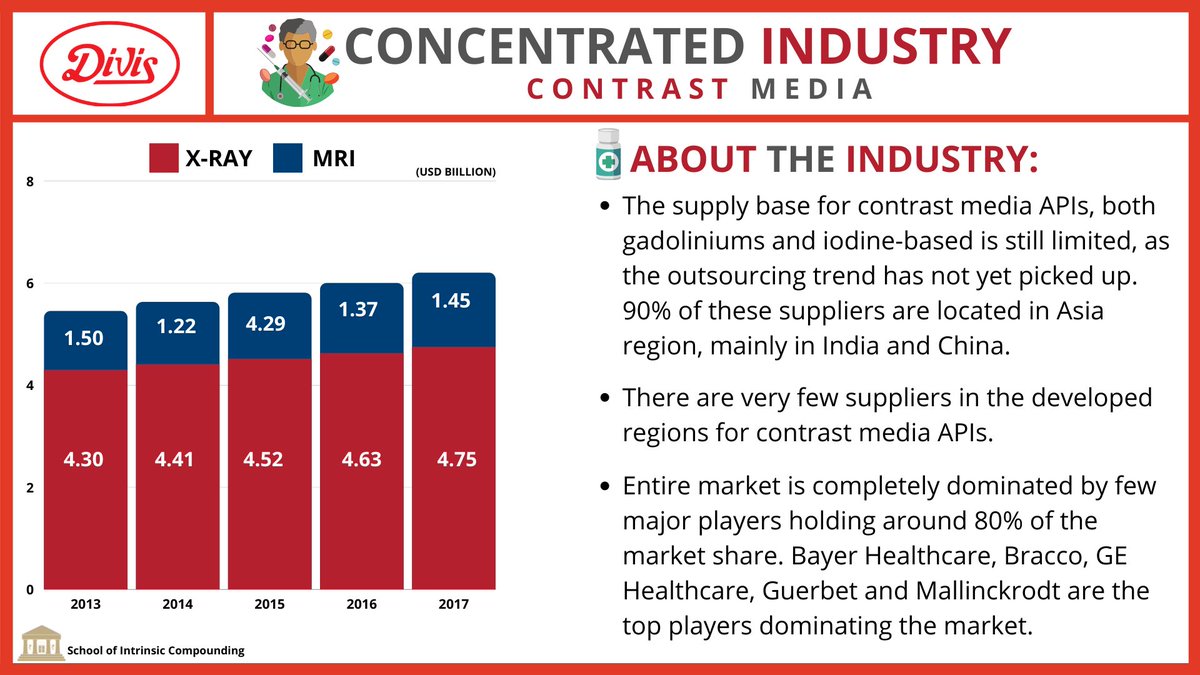

as data comes through. Some of the narrative which is commonly used by investors, is the journey of a company from a commodity business to a high value added business. Lets look at some Indian examples🇮🇳🇮🇳

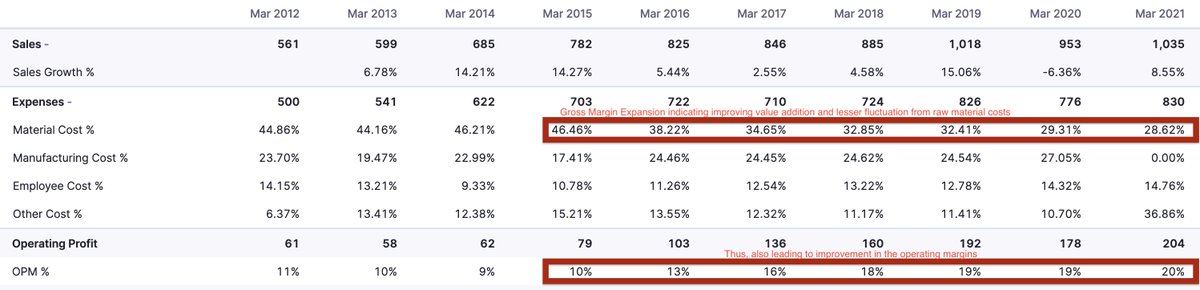

Example 1: Garware Technical Fibres:

For those who have been betting on the business for last 5-6 years. The thesis has always been very clear, that it is shedding the tag of a commodity business and adding products which are higher margin in nature. How to identify this?

For those who have been betting on the business for last 5-6 years. The thesis has always been very clear, that it is shedding the tag of a commodity business and adding products which are higher margin in nature. How to identify this?

Just read the credit rating and keep readjusting your thesis based on the data i.e. the financial numbers a compay reports. 2015 credit rating

Same line has been repeated in the 2016,2017,2018,2019,2020&2021 credit rating. Just look at the margin expansion that has taken place in the business, thereby effectively the thesis playing out. Journey from a commodity to value added

Example 2: Betting on shallow cyclical businesses when they are in a downturn. Balkrishna Industries is a dominant business that operates in Off the Highway tyres business. This is a busniess that gets more than 50% of its revenue from Agri tyres, agriculture is again

a cyclical activity. Which leads to fluctuation in the topline. In the downyears, Brokerages forget the 101 of cyclicality, they come out with sell reports that are often 50% of the market price (remember one which gave a TP of Rs400 lol)

However, the business remains dominant. Smart investors who are bullish either hold or add given they know the cyclicality of the business and others with a shorter horizon often enter at the time of pain. But the lesson remains, the words with which you describe a business

1000% play a part in whether you will be able to hold or add or whether you will end up selling whenever market corrects. Thesis backed up earnings growth and the ability to change ones mind is absolutely lethal for an investor who knows what he/she is doing.

The ability to detach from the crowd and re-assessing the beautiful symphony between your story of a business and the data that comes is what matters. Most won't do this, but for those who do. Sooner or later you will get lucky😁

The thread is inspired by the book Investing the Last Liberal Art by Robert G.Hagstorm

The reason why words, investing philosophy, and narrative is important when many of the great investors like @unseenvalue @SamitVartak @virajmehta16 @a_basumallick use it to describe their process

• • •

Missing some Tweet in this thread? You can try to

force a refresh