1/ Some thoughts on $SPOT after reflecting on Q2 21 results.

Summary thoughts:

I think the MAU miss has had a disproportionately negative impact on the share price, as it was the second quarter in a row of MAU coming in below expectations.

Summary thoughts:

I think the MAU miss has had a disproportionately negative impact on the share price, as it was the second quarter in a row of MAU coming in below expectations.

2/ The 22% yoy growth in MAUs they did achieve given some self-inflicted email signup issues and an emerging market Covid impact whereby they fully pulled back from marketing spend in India which impacted signups is by no means a terrible outcome.

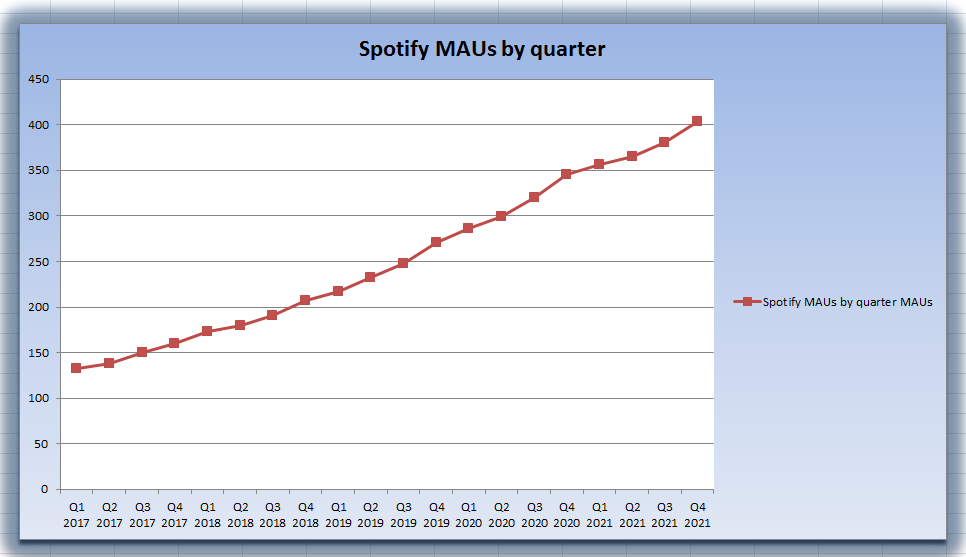

3/ This chart shows MAUs quarterly since Q1 2017 (Q3 and Q4 2021 numbers are mid-point of co guidance). There does not look to be anything sinister going on with this trend:

4/ I think a key data point that the company puts across is that engagement amongst $SPOT users continues to run at 2-3x that of competing platforms.

5/ That is a very powerful testament to the value of the platform to its users and ultimately leads to monetisation, via both advertising as well as subscription pricing power.

6/ The power of a focused company against competitors that offer music as a tiny afterthought vs their main business should not be underestimated as $SPOT continues to roll out innovations at a much faster pace than its peers.

7/ We have worked with the disclosed numbers and they support the company's explanation that it was EM that caused the MAU miss not North America, contrary to the argument of the Redburn analyst.

8/ This is helpful, supporting the company's assertion that they did not see any erosion in gross adds or churn in regions where they took price.

9/ I think the growth in the ad-supported business was a huge positive and can be the key narrative driver for the shares over the next 12-24 months as it enables the company to escape the gross margin trap of having to pay away 65% of its music revenues to the major labels.

10/ I also think the company's positive commentary regarding MAU outlook into the back half of the year combined with what looks like very conservative guidance (for 18.7% and 17% yoy MAU growth in Q3 and Q4 2021 respectively) sets the company up well for beats going forward.…

11/ …With the shares 40% off their recent highs I think they look standout risk-reward in here.

12/ Some more detail:

• Taking a step back, I think it's important to remember that $SPOT beat on every metric in Q2 2021 apart from MAUs. It beat on premium subscriber count, it beat on ARPU and it massively beat on ad-supported revenues.

• Taking a step back, I think it's important to remember that $SPOT beat on every metric in Q2 2021 apart from MAUs. It beat on premium subscriber count, it beat on ARPU and it massively beat on ad-supported revenues.

13/ • I think the huge growth in ad-supported revenues (up 110% yoy) and the massive gross margin expansion seen there was the key positive from the quarter and can be a big narrative and hence share price driver over the next 12-24 months.

14/ Ad-supported gross margin went from -12% in Q2 2020 to +11% in Q2 2021 which to me shows the scalability and drop-through potential of podcast advertising as it continues to grow.

Podcast ad revenues grew 700%, or 200% on an organic basis.

Podcast ad revenues grew 700%, or 200% on an organic basis.

15/ We know that podcast listening continues to grow and still has plenty of room to grow.

The company have explicitly said that lack of ad inventory (supply) is their constraining factor, not demand.

The company have explicitly said that lack of ad inventory (supply) is their constraining factor, not demand.

16/ Given advertising follows audience, this lack of supply will continue to be addressed as advertisers get better and more experienced with the format. CPMs are high as it is a very targeted form of advertising with an extremely engaged audience.

17/ The margins of podcast advertising should be very high indeed and thus very important both from a financial perspective given the company's low gross margins but also from a narrative perspective as the key way in which the company can escape the margin trap of its…

18/ …business model, having to pay away 65% of its music revenues to the major labels.

19/ • The MAU miss being ascribed to Covid vs their comment last quarter that Covid pulled forward some 2020 demand again adds uncertainty to how exactly Covid has and is affecting their business. Redburn analyst has tried to make the case that it's the US to blame.

20/ Our work supports management view that the miss came from emerging markets, not from the US which has run at these MAU growth levels for several quarters now.

21/ Management explicitly said that they did not see gross adds or churn pressure in those regions where they took price.

They explicitly blamed the Indian MAU miss on them consciously pulling back on marketing due to Covid flare-up over there.

They explicitly blamed the Indian MAU miss on them consciously pulling back on marketing due to Covid flare-up over there.

22/ They are leaning back into marketing spend here and are confident in MAU outlook for H2.

• The actual trajectory of MAUs per quarter going back to Q1 2017 is shown in the chart below.

• The actual trajectory of MAUs per quarter going back to Q1 2017 is shown in the chart below.

23/ It is not a chart that I think should raise any significant level of concern regarding something untoward happening to the business:

The Q3 2021 and Q4 2021 figures in the chart below are the mid-points of their guidance.

The Q3 2021 and Q4 2021 figures in the chart below are the mid-points of their guidance.

24/ They added 9m MAUs in Q2 which was 22% yoy growth, down from 24% last quarter and down from 27% in Q4 2020.

25/ Given their commentary about positive outlook for H2 MAUs and them ramping marketing spend back up, I think their MAU guidance for 18.7% yoy growth in Q3 2021 and 17% yoy growth in Q4 2021 is conservative and they have set themselves up to beat.

26/ This combined with the momentum in their advertising business as well as the share price 40% off its highs sets the shares up very well in here. I think the risk-reward is very attractive and timely in here. Thanks for reading. END.

• • •

Missing some Tweet in this thread? You can try to

force a refresh