Re $SPOT, I see a very favourable alignment between the longer-term attractive risk-reward profile and a near-term attractive setup.

These alignments don't happen very often but are what I look for in order to size up conviction in a position.

These alignments don't happen very often but are what I look for in order to size up conviction in a position.

I think the setup for $SPOT here is stand-out attractive. I'll outline why in this pretty long thread.

I posted a few brief thoughts post their Q2 21 results here:

I posted a few brief thoughts post their Q2 21 results here:

https://twitter.com/anthonyc3004/status/1422945079786881024?s=20

Before I get to the long-term bull thesis I'll highlight the near-term setup as it's the most timely element of this thread.

MAUs are clearly a near-term focus after their 2nd consecutive miss in Q2 (the rest of the result was good) and any evidence of stabilisation here in upcoming Q3 result will be very helpful from a narrative perspective.

Sensor Tower data shows a very significant recent improvement, which bodes well for this datapoint in Q3. Management made it clear that they have turned back on marketing spend which was off during a Covid-impacted Q2, especially in India.

They look to have guided conservatively & I see very good probability of a decent MAU beat in Q3.

The key narrative inflection that I see over the next 18 months is on the margin side, with advertising revenues (predominantly podcasting ad revs) demonstrating their high degree of scalability & driving gross margins higher.

This is important as the stock is considered uninvestable by many and is penalised heavily by others, understandably so, for being at the mercy of & downstream to the major music labels and unable to escape the poor economics it has locked itself into re having to pay away 65%…

…of its revenues to the labels. The most recent quarter gave an inkling of the scalability of ad revenues, with gross margin for ad revenues improving from -11% in Q2 2020 to +12% in Q2 2021 on a 200% organic growth in podcasting revenues.

These tools have only just been built/ acquired; the new Spotify Audience Network advertising marketplace allows advertisers to publish across Spotify-owned podcasts, 3rd party podcasts, podcasts on other platforms (via Megaphone) and ad-supported music and Streaming Ad…

…Insertion that allows ads to be dynamically inserted into the content similarly to YouTube.

The audience for podcasting is growing very strongly, and advertisers are following audiences - the company have consistently highlighted lack of supply & not demand as the constraint on ad revenues.

$SPOT recently launched their first global marketing campaign aimed at advertisers (I see these ads everywhere on my Twitter feed), highlighting what an engaged audience they have on their platform.

Margin expansion from podcasting ad revenues is a key positive driver for the stock over the next couple of years and the entry point here in the low $200s is very attractive, with the stock having de-rated from 6x EV/sales in February this year to 3.4x EV/sales now...

...offering a more than 20% IRR on my conservative forecasts for the next several years.

Quick run-through of longer-term bullish thesis:

a) Music listening continues to fragment away from the major labels as streaming becomes more mainstream globally.

a) Music listening continues to fragment away from the major labels as streaming becomes more mainstream globally.

b) Developed markets music streaming is only 30% of music consumption, can trend to 70% over time giving huge secular tailwind for Spotify as the number 1 global player.

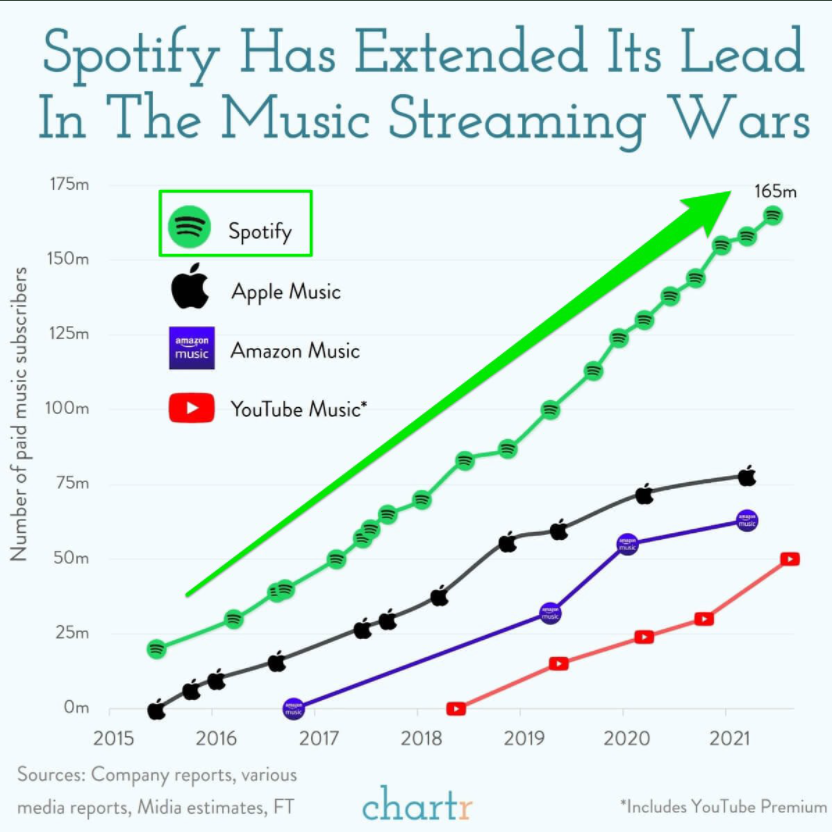

c) Up against large very deep-pocketed peers, $SPOT continues gaining share; its narrow focus vs their diversified focus driving a much more rapid pace of innovation based on customer wants and needs (chart below does not include $SPOT's 200m+ ad-supported customers).

d) Labels importance in the value chain decreases over time as tools continuously improve for artists' self-serve music publishing and social media enables mass awareness without label help.

This combined with $SPOT continuing to gain share hugely improves their negotiating power over time.

In the medium term, $SPOT will benefit from labels shifting more of their marketing budget onto the platform to drive market share & as Spotify are able to explicitly demonstrate favourable ROIs vs the lack of transparency of much of the labels' traditional marketing efforts.

e) $SPOT consistently talk about their engagement being 2-3x higher than that of their competitors. This is a key differentiator and enables monetisation over time, via pricing power of subscriptions and via advertising revenues.

f) Podcasting ad revenues are hugely scalable and not factored properly at all into long-term consensus. 2025 consensus has advertising growing from 12% of total company revenue to 17% in 2025 while only contributing 12% of company gross profit in 2025.

This is just very wrong - the music advertising revenues should scale to 30% gross margin while the podcasting advertising revenues will be very scalable as seen with other digital advertising businesses and hence much higher gross margin.

Right now, podcast ad revs are nascent at around 2% of total company revenues (17% of ad revenues) and are not GM positive but moving sharply in the right direction.The company has confirmed the incremental ad dollar from a podcast is much more accretive than that from music.

Podcast margins will increase materially over time, with continued content investment the offsetting factor.

Some key bear pushbacks:

a) Music is a commodity with no differentiation between platforms.

a) Music is a commodity with no differentiation between platforms.

I see the much higher level of engagement on $SPOT vs peers as clear evidence that this is not true - differentation comes from personalisation, interface & product improvement cadence, all of which have a network effect element as Spotify accumulate more user data.

b) Spotify cannot exist without the content from the big labels. This is true but the converse is also becoming more and more true as Spotify continues to gain share and cement its clear number 1 position in the only meaningful growing revenue stream for the labels.

While I do see the long-term picture as skewed in favour of Spotify vs the labels (and absolutely see the merit in shorting $WMG against $SPOT long) my bull case for Spotify does not rely on the economics meaningfully changing in the streamers/ labels relationship.

c) Competitively, $SPOT are losing out to YouTube Music. The YouTube Music stats out there are misleading as they include free trials in the end number but not the start number. Adjusting for this, YouTube Music is not taking share from $SPOT.

d) #NFTs/ Web 3.0 as risk to a centralised rent-taker like $SPOT. This is something I keep an eye on and a fast-moving space I enjoy learning about.

It is clearly very early stages and Daniel Ek is very much aware of the opportunity and risk from the crypto eco-system and I'd consider him well-placed to take advantage of the many opportunities here as the wide-ranging capabilities of non-fungible tokens for artists become…

…more clear. The benefit of a forward-looking founder CEO is obvious here vs a more mercenary style of CEO.

Summary: $SPOT shares offer very attractive risk-reward in here (shares are at $220 at time of writing) with a confluence of attractive near-term, medium-term and long-term setups. Thanks for reading, END.

• • •

Missing some Tweet in this thread? You can try to

force a refresh