1/ $IAC/ $ANGI 2Q’21 Update

I always enjoy reading IAC shareholder letter and this was no exception. Q&A, however, gets a bit too lengthy and repetitive.

Here are my notes.

I always enjoy reading IAC shareholder letter and this was no exception. Q&A, however, gets a bit too lengthy and repetitive.

Here are my notes.

2/ ANGI

“They say home improvement projects usually take twice as long and cost twice as much relative to expectations going in, and one of our goals at Angi is to prove that axiom false. Ironically, delivering that proof appears to be, well, taking us longer and costing us more"

“They say home improvement projects usually take twice as long and cost twice as much relative to expectations going in, and one of our goals at Angi is to prove that axiom false. Ironically, delivering that proof appears to be, well, taking us longer and costing us more"

3/ “Exercising options creates the most attention, but creating options builds the most value.”

This was classic.

This was classic.

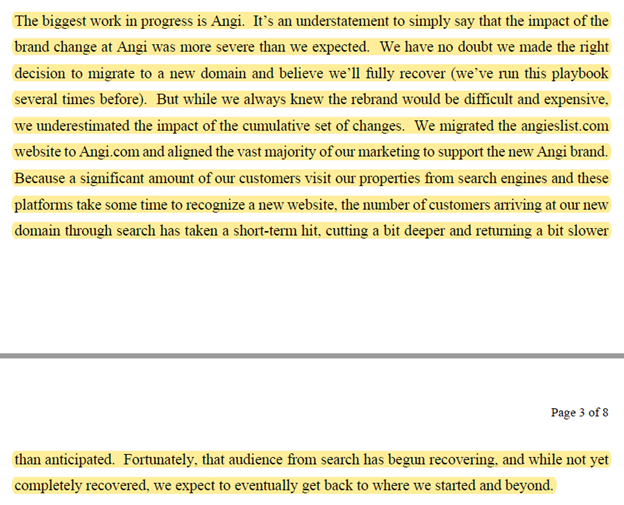

4/ While the brand change led to more severe impact than expected, management believes this was indeed the right strategy. They shared more data in Q&A and explained why HomeAdvisor brand was just too generic.

5/ “A more conservative approach might have staged some of these changes over time, but we are plowing

ahead with all at once under the belief that we know and like our destination, so let’s not waste time getting there.”

ahead with all at once under the belief that we know and like our destination, so let’s not waste time getting there.”

6/ “Building a brand takes time and capital as does building a disruptive start up, which we’re doing in Angi Services. We will likely operate the business in and around breakeven for the balance of 2021 at least”

7/ “If other shareholders lose patience during this phase for Angi, we at IAC are happy to own more through continued share repurchases at Angi.”

Love how IAC communicates with the shareholders.

Love how IAC communicates with the shareholders.

8/ Angi services have three components: retail business, book now, and managed services.

Angi payments +70% QoQ, now $3 mn/week

Financing tripled, although on low volume.

Also bought a roofing business to increase supply.

Angi payments +70% QoQ, now $3 mn/week

Financing tripled, although on low volume.

Also bought a roofing business to increase supply.

9/ Lots of things to be excited about, but the fact remains Angi has been a perennial “work-in-progress” for a long time.

It’s a very difficult business, but do believe it remains a very convex bet.

It’s a very difficult business, but do believe it remains a very convex bet.

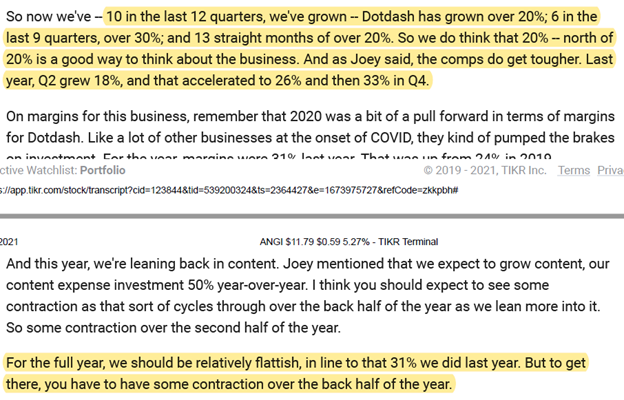

10/ Dotdash

Four big segments: finance, health, lifestyle, and beauty (smaller than the other three which are roughly equivalent in size)

“our content investment's up 50% year-over-year this year, and I hope to continue to grow that faster than revenue for a while.”

Four big segments: finance, health, lifestyle, and beauty (smaller than the other three which are roughly equivalent in size)

“our content investment's up 50% year-over-year this year, and I hope to continue to grow that faster than revenue for a while.”

11/ “From 2019 to 2021, the top 25 advertisers, those same 25 names are spending 139% in 2021 of what they were spending in 2019 and I think 123% or something like that of what they were spending in 2020.”

12/ IAC is pitching Dotdash from the data privacy angle.

Dotdash has indeed a great advertising product, but I’m sorry Joey, I think advertisers are the last group in the world who would find data privacy pitch compelling.

Dotdash has indeed a great advertising product, but I’m sorry Joey, I think advertisers are the last group in the world who would find data privacy pitch compelling.

13/ Great growth momentum for Dotdash in the last 3 years, but “tough comps” now.

14/ Care

Enterprise segment continues to be the shining light whereas consumer segment still faces headwinds.

Enterprise segment continues to be the shining light whereas consumer segment still faces headwinds.

15/ Care is not about just child care, but senior care is also big part of it which enjoys demographic tailwind.

16/ “When mobile apps became a thing that we launched an incubator very early which was entirely focused on building mobile apps. And that's where Tinder came out of.”

New incubator’s focus on blockchain, but the first 2 biz on incubation have nothing to do with blockchain

New incubator’s focus on blockchain, but the first 2 biz on incubation have nothing to do with blockchain

17/ “we’re building options everywhere. The process is rarely easy or fast, but one of the most important elements of an option’s value is duration, and the structure of IAC allows us to take the time to build to win.”

• • •

Missing some Tweet in this thread? You can try to

force a refresh