Annex A provides an interesting summary of the history of these schemes, emphasising the expansion to contractor loans in about 2004 (previously said to be 2005/06).

25/33

25/33

https://twitter.com/keithmgordon/status/1427919604089769984

More acknowledgement of HMRC’s delays (particularly pre-2009)

26/33

26/33

And here we see why the position WAS NOT CLEAR after the 2011 changes.

27/33

27/33

Annex B deals with settlement terms

28/33

28/33

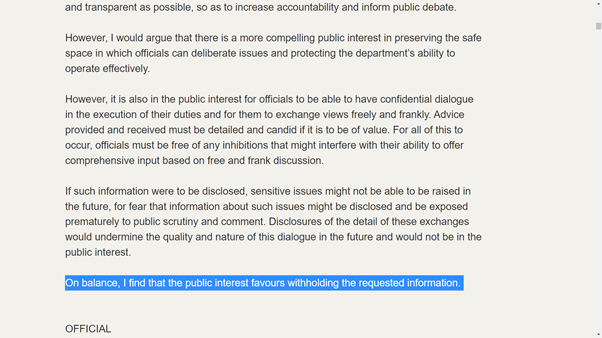

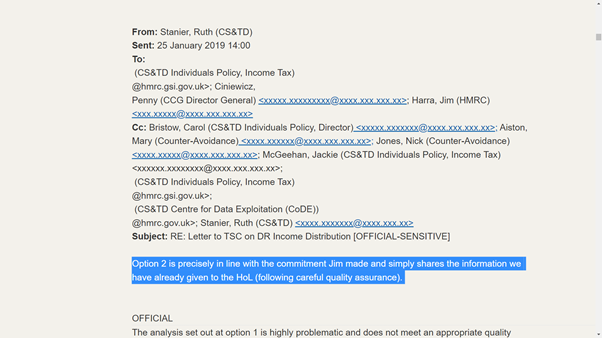

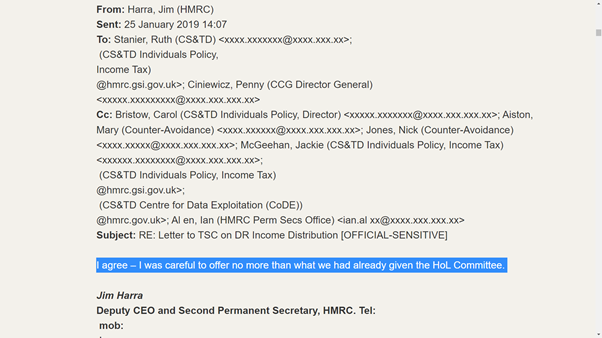

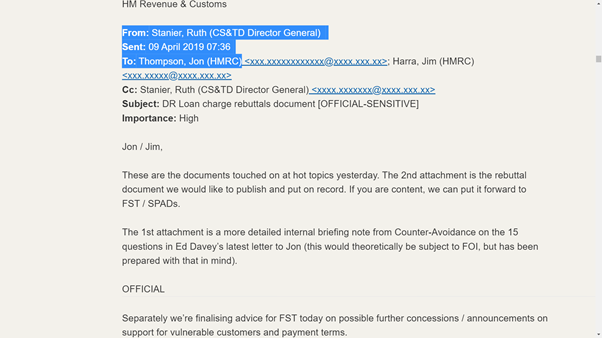

Annex C summarises how HMRC publicised their views.

A lack of any clear communication with the taxpayers involved until 2014 (when just 11000 taxpayers were written to).

29/33

A lack of any clear communication with the taxpayers involved until 2014 (when just 11000 taxpayers were written to).

29/33

Annex D on taxpayer safeguards

30/33

30/33

Annex D continued

31/33

31/33

Annex E shows that the majority of people affected are indeed contractors.

32/33

32/33

Annex F shows the pro-HMRC feedback gleaned from media outlets (rather than the criticism levelled against the loan charge policy).

33/33

33/33

• • •

Missing some Tweet in this thread? You can try to

force a refresh