If we think in probabilities we conclude US stocks rarely crash or underperform for long periods. Most of the time, it's a good bet.

However, this might be one of those rare times just like 1929, 37, 68, 99 & 2007.

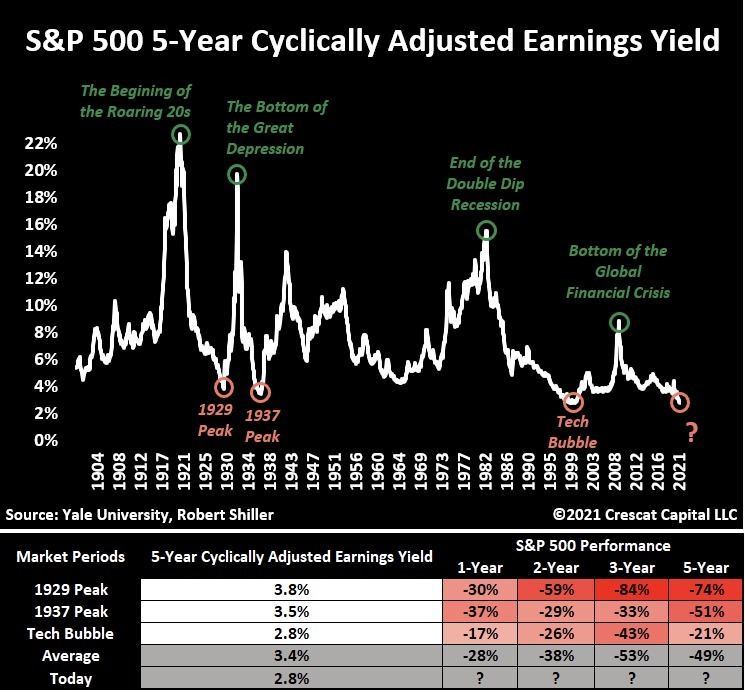

Is the probability in the bull's favor, by taking a bet here?

However, this might be one of those rare times just like 1929, 37, 68, 99 & 2007.

Is the probability in the bull's favor, by taking a bet here?

Clearly not. But the chart by @TaviCosta has some drawbacks.

1. made by an investor who is biased: favors gold over stocks for many years

2. situation looks risky but could get even worse, especially because it's in CB's interest

3. while I doubt it, could end up a non-event

1. made by an investor who is biased: favors gold over stocks for many years

2. situation looks risky but could get even worse, especially because it's in CB's interest

3. while I doubt it, could end up a non-event

How are we playing things at this stage?

Despite being extremely expensive by any historical metric, US stocks could continue to rally. I would never bet against them, that's a sucker's game.

Instead, we are focused on uncorrelated alternative assets & are also buying things...

Despite being extremely expensive by any historical metric, US stocks could continue to rally. I would never bet against them, that's a sucker's game.

Instead, we are focused on uncorrelated alternative assets & are also buying things...

...periodically where we see relative value.

E.g. if we are lucky to find a real estate deal with a meaningful discount (25%+ below market value) we will act on it.

If we notice quality businesses or sectors, with promising future growth, that crashed 50%+ we will act on it.

E.g. if we are lucky to find a real estate deal with a meaningful discount (25%+ below market value) we will act on it.

If we notice quality businesses or sectors, with promising future growth, that crashed 50%+ we will act on it.

Everything was down in March 2020, so we made a bet on small-cap value.

Small-cap Oil & Gas industry was very much disliked & depressed in October 2020, so we acted.

We now believe Chinese internet stocks, down 50%+, are offering relative value & have started acting on it.

Small-cap Oil & Gas industry was very much disliked & depressed in October 2020, so we acted.

We now believe Chinese internet stocks, down 50%+, are offering relative value & have started acting on it.

As mentioned, we're also pushing capital into attractive alternatives for a number of reasons.

E.g. litigation funding is uncorrelated to stock markets, economic cycles, interest rates, Fed's balance sheet, etc. Plus it has a natural liquidity event at settlement or trail.

E.g. litigation funding is uncorrelated to stock markets, economic cycles, interest rates, Fed's balance sheet, etc. Plus it has a natural liquidity event at settlement or trail.

Another e.g. we have made a private equity investment in country town pharmacies across the midlands of the UK, where the focus is buying distressed mom & pop shops for 5X EBITDA, consolidating them into a 30+ group & hopefully achieving an exit one day (no hurry) @ 9-10X EBITDA.

Internet disruption & e-commerce penetration is a non-event in the UK pharmacy game for a variety of reasons.

Furthermore, the aging population is a tailwind here. Not to mention, the industry is very, very resilient relative to the normal business cycle for obvious reasons.

Furthermore, the aging population is a tailwind here. Not to mention, the industry is very, very resilient relative to the normal business cycle for obvious reasons.

We are hoping we've learned the lessons of 1929, 1937, 1972, 1996 (in Asia), 1999 (in tech) & especially 2007 which gave me first-hand experience.

Meanwhile, the majority of investors are currently acting like Fed's balance sheet has given them amnesia.

Interesting times ahead!

Meanwhile, the majority of investors are currently acting like Fed's balance sheet has given them amnesia.

Interesting times ahead!

• • •

Missing some Tweet in this thread? You can try to

force a refresh