Last year, I argued that ESG was the most overhyped, and oversold concept in business (bit.ly/3lnozXw), and heard from people who felt I was missing its good points. After a year of searching, I still cannot find them.. bit.ly/3nwSP4N

Measuring goodness is difficult to do, which is why services disagree on ESG rankings/scores. It will not get easier over time, because we have different value systems. Your measure of "goodness" will not match mine. bit.ly/3nwSP4N

The evidence on ESG's effect on value is muddled. A stronger case can be made that companies should not be bad, (because they will face higher funding costs and failure risk) than that they should spend money to be good. bit.ly/3nwSP4N

If good firms have lower funding costs, arguing that investing in good companies will earn higher returns is internally contradictory, and incoherent, since the link between ESG & returns is more a reflection of pricing than it is of how ESG affects value. bit.ly/3nwSP4N

In the old model, companies focused on business, investment funds on returns, and shareholders chose how much, and who to give to, in society. In the ESG model, companies and fund managers make those choices instead. Not clear how or why society benefits.. bit.ly/3nwSP4N

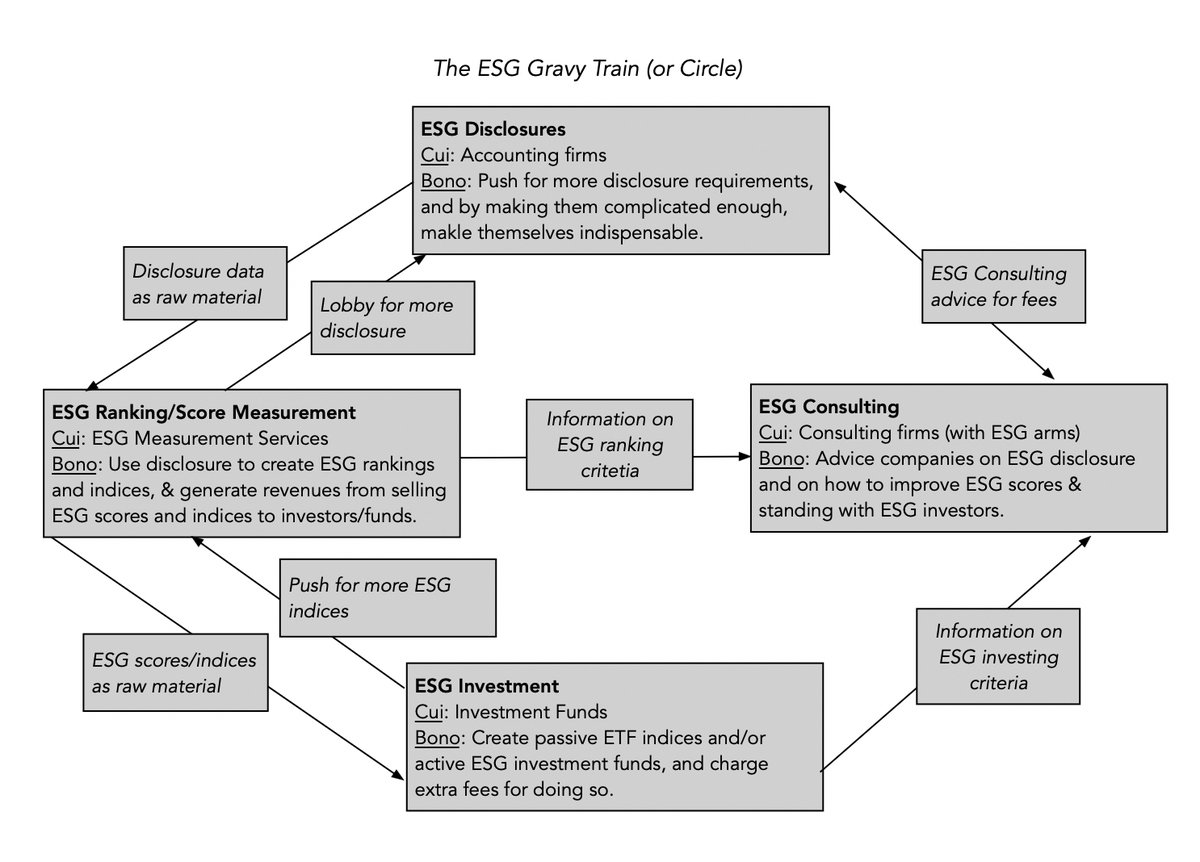

Why is ESG being sold so aggressively? Because accountants, measurement services, fund managers & consultants are on the ESG gravy train, with stockholders & taxpayers paying. Corporate CEOs are buying into ESG, because it makes them accountable to no one. bit.ly/3nwSP4N

Bring your moral code into your own business & investment decisions, but investing other people's money to advance what you view as "good" is hubris. Accept that being good is more likely to cost & inconvenience, than to help, you, and be okay with that. bit.ly/3nwSP4N

• • •

Missing some Tweet in this thread? You can try to

force a refresh