A couple of times a year, I teach a course with @Robot_Wealth, aimed at retail or part-time traders who want to start taking the game more seriously.

robotwealth.com/trade-like-a-q…

Much of it I brainstormed out loud on Twitter.

Here's what's in the course, as a 🧵of 🧵s 👇👇👇

1/n

robotwealth.com/trade-like-a-q…

Much of it I brainstormed out loud on Twitter.

Here's what's in the course, as a 🧵of 🧵s 👇👇👇

1/n

First, trading successfully is really hard.

Traders often start off on the wrong foot because they don't take the problem seriously enough.

They think of the market as a big casino. They think of it as an easily exploitable game driven by fear, greed, and emotion.

2/n

Traders often start off on the wrong foot because they don't take the problem seriously enough.

They think of the market as a big casino. They think of it as an easily exploitable game driven by fear, greed, and emotion.

2/n

The reality is quite different. It's an efficient arbitrage and pricing machine.

So first, we start exploring this by asking:

"If trading were a winnable game, we should be able to lose at it on purpose. How would we lose money trading?"

3/n

So first, we start exploring this by asking:

"If trading were a winnable game, we should be able to lose at it on purpose. How would we lose money trading?"

https://twitter.com/therobotjames/status/1381387162730422272?s=20

3/n

We find that market games are ultra-competitive, which makes it hard to make money trading in the short term and the long term.

The same factors that make it hard to make money, make it hard to lose money consistently too - as long as you avoid a few dumb things.

4/n

The same factors that make it hard to make money, make it hard to lose money consistently too - as long as you avoid a few dumb things.

4/n

It's clear that you need a solid business plan.

And understanding that the "ruthless efficiency of the market" can be both a blessing and a curse is key.

So we build up a business plan to extract market returns by *minimizing competition and playing the easiest games*.

5/n

And understanding that the "ruthless efficiency of the market" can be both a blessing and a curse is key.

So we build up a business plan to extract market returns by *minimizing competition and playing the easiest games*.

5/n

First, we need at least one "stonkingly obvious edge" to build our trading upon.

Something we can have a high degree of confidence in.

And it should be as "win-win", uncompetitive and hard-to-screw-up as possible.

6/n

Something we can have a high degree of confidence in.

And it should be as "win-win", uncompetitive and hard-to-screw-up as possible.

6/n

Second, as long as we avoid the Mortal Sins of:

1. Trading too Big

2. Trading too Much

3. Trying to be a Hero

The market doesn't punish us that much for being wrong.

This creates a nice asymmetry we might be able to exploit and go after more competitive inefficiencies.

7/n

1. Trading too Big

2. Trading too Much

3. Trying to be a Hero

The market doesn't punish us that much for being wrong.

This creates a nice asymmetry we might be able to exploit and go after more competitive inefficiencies.

7/n

So we look to "Trade More Sh1t" and add strategies that exploit market inefficiencies.

We look at inefficiencies caused by large rebalance flows and misaligned trader objectives.

When we combine noisy edges together, the whole tends to be greater than the sum of the parts.

8/n

We look at inefficiencies caused by large rebalance flows and misaligned trader objectives.

When we combine noisy edges together, the whole tends to be greater than the sum of the parts.

8/n

Our business plan harnesses the first two effects from this thread:

It's a plan which is focused on *high probability outcomes.

We prioritize smart game selection over trading skill.

9/n

https://twitter.com/therobotjames/status/1359349194230693889?s=20

It's a plan which is focused on *high probability outcomes.

We prioritize smart game selection over trading skill.

9/n

With an overall plan in place - we start to build out the components.

And each component needs its own business case.

"I'm smart and hard-working" is not a business case.

You're not here to f--- spiders.

You need stuff that stacks up:

10/n

And each component needs its own business case.

"I'm smart and hard-working" is not a business case.

You're not here to f--- spiders.

You need stuff that stacks up:

https://twitter.com/therobotjames/status/1384361563558010882?s=20

10/n

So we look at successful trading approaches of the past.

And we find that the reason they tended to work was because one was being paid to:

1. do something useful

2. take on risk or unattractive work

3. do the job well.

Like any other business you might believe in.

11/n

And we find that the reason they tended to work was because one was being paid to:

1. do something useful

2. take on risk or unattractive work

3. do the job well.

Like any other business you might believe in.

11/n

We want trades where there's some obvious cause/effect.

We want "stonkingly obvious edges".

We'll look at Risk Premia Harvesting. Where we look to be rewarded for taking on risks others are keen to avoid.

12/n

We want "stonkingly obvious edges".

We'll look at Risk Premia Harvesting. Where we look to be rewarded for taking on risks others are keen to avoid.

12/n

We find that assets that are sensitive to certain risks tend to be less attractive.

Risks such as:

- rising interest rates

- rising inflation

- credit risk

- lower economic growth

- political risk

make assets like stock indexes less attractive than less risky assets.

13/n

Risks such as:

- rising interest rates

- rising inflation

- credit risk

- lower economic growth

- political risk

make assets like stock indexes less attractive than less risky assets.

13/n

Cos losing money ain't fun.

So when we hold risky assets, we're actually doing something useful.

It's a win-win situation.

You - as person prepared to take the risk - expect to get paid in excess returns.

And the risk-averse person is happy to avoid the risk.

14/n

So when we hold risky assets, we're actually doing something useful.

It's a win-win situation.

You - as person prepared to take the risk - expect to get paid in excess returns.

And the risk-averse person is happy to avoid the risk.

14/n

Or "Stonks. They Go." Well, the index tends to. If you're patient enough.

And it tends to go up BECAUSE of their inherent risk.

So the job is to:

1. get exposed to the risks that pay

2. minimizing the ones that don't.

15/n

And it tends to go up BECAUSE of their inherent risk.

So the job is to:

1. get exposed to the risks that pay

2. minimizing the ones that don't.

15/n

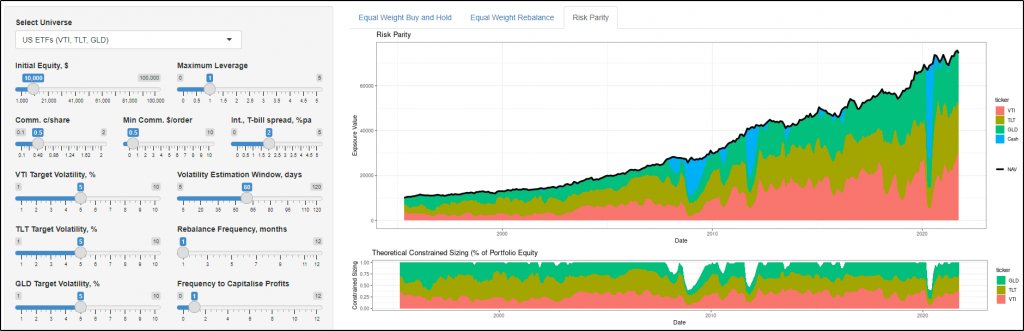

So we put together a simple 3 asset risk premia harvesting strategy, which dynamically manages the risks we're not paid for through:

- diversifying in 3 dissimilar assets

- dynamic sizing and rebalancing to target equal risk contribution.

16/n

- diversifying in 3 dissimilar assets

- dynamic sizing and rebalancing to target equal risk contribution.

16/n

And we discuss how not to screw up good edges by overcomplicating them.

17/n

https://twitter.com/therobotjames/status/1383954970341380100?s=20

17/n

Risk Premia Harvesting is "win-win". Nobody needs to lose out for you to harness excess returns. That's why we have high confidence in it.

Next, we can start looking at slightly more competitive games which exploit market inefficiencies.

18/n

Next, we can start looking at slightly more competitive games which exploit market inefficiencies.

18/n

Exploiting market inefficiencies is "win-lose", at least if you think about expected returns.

Your excess returns come from "buying from someone too cheap".

Or "selling to someone too expensive".

Someone loses out.

19/n

Your excess returns come from "buying from someone too cheap".

Or "selling to someone too expensive".

Someone loses out.

https://twitter.com/therobotjames/status/1387216598331650052?s=20

19/n

So these games are less stable but probably worth going after as long as you have more high probability ideas covered first

But where do we find opportunities?

And how do we get the opportunity to trade them - given there are more sophisticated players competing with us?

20/n

But where do we find opportunities?

And how do we get the opportunity to trade them - given there are more sophisticated players competing with us?

20/n

We discover we need two things to be true.

First - you need to find a time when a large group is willing or forced to trade at inopportune prices. You'll need to understand the constraints and incentives of the big "end users" in the market.

21/n

First - you need to find a time when a large group is willing or forced to trade at inopportune prices. You'll need to understand the constraints and incentives of the big "end users" in the market.

21/n

Second, you need inefficiencies that aren't fully "gobbled up" by other players.

Inefficiencies can "leak out" because they are:

- too big or random

- too small, too noisy, too capital intensive or too awkward to harness.

22/n

Inefficiencies can "leak out" because they are:

- too big or random

- too small, too noisy, too capital intensive or too awkward to harness.

22/n

This leads us to being able to identify inefficiencies YOU can exploit.

You'll learn how to make simple testable "elevator pitches" for these inefficiences.

These are simple statements of:

- why the inefficiency exists

- why you think YOU can exploit it.

23/n

You'll learn how to make simple testable "elevator pitches" for these inefficiences.

These are simple statements of:

- why the inefficiency exists

- why you think YOU can exploit it.

23/n

A 5-year-old should buy your elevator pitch and understand why you might expect to get paid for doing that thing.

24/n

https://twitter.com/therobotjames/status/1372731067635953664?s=20

24/n

Your pitch will include:

1. What would cause the inefficiency

2. Why it wouldn't be fully "gobbled up" by others who are quicker or better informed

3. How you might harness it, on average.

25/n

1. What would cause the inefficiency

2. Why it wouldn't be fully "gobbled up" by others who are quicker or better informed

3. How you might harness it, on average.

25/n

If doing this sounds intimidating, it's probably because it is. At least a little.

You probably aren't used to thinking like this. And don't trust your instincts yet.

But through a lot of discussions and examples, I'll make sure you get it.

26/n

You probably aren't used to thinking like this. And don't trust your instincts yet.

But through a lot of discussions and examples, I'll make sure you get it.

https://twitter.com/therobotjames/status/1372754958940917770?s=20

26/n

Now you have a compelling pitch, what next?

Well... sometimes if it's compelling enough - or you don't have enough data - that's enough.

But, ideally, you want to see clear evidence of the effect in past data.

So we look at very simple data analysis techniques in Excel

27/n

Well... sometimes if it's compelling enough - or you don't have enough data - that's enough.

But, ideally, you want to see clear evidence of the effect in past data.

So we look at very simple data analysis techniques in Excel

27/n

You'll learn a process for finding exploitable edges based on:

1. an understanding of market structure and trader behavior

2. simple data analysis

No more shall you be stuck in the "Backtest Cycle of Doom", trying random stuff and hoping it works

28/n

1. an understanding of market structure and trader behavior

2. simple data analysis

No more shall you be stuck in the "Backtest Cycle of Doom", trying random stuff and hoping it works

https://twitter.com/therobotjames/status/1382420222502604803?s=20

28/n

Next, we'll learn how to design simple systematic trading strategies to exploit the inefficiencies we have found.

We want the simplest, most robust set of rules to exploit the effect.

Every time you add a rule, you are adding a way for you to mess up a good edge.

29/n

We want the simplest, most robust set of rules to exploit the effect.

Every time you add a rule, you are adding a way for you to mess up a good edge.

29/n

Systematic trading is not a thing of great precision.

We identify a noisy edge that we think we can exploit noisily, on average. Then we swing the bat at it as often as we can.

Rocket surgery, it ain't.

So we look to exploit these effects in the simplest way possible.

30/n

We identify a noisy edge that we think we can exploit noisily, on average. Then we swing the bat at it as often as we can.

Rocket surgery, it ain't.

So we look to exploit these effects in the simplest way possible.

30/n

We'll show you how we designed three simple trading strategies to trade flow-based market inefficiencies.

When you combine the strategies, the whole can be greater than the sum of their parts.

31/n

When you combine the strategies, the whole can be greater than the sum of their parts.

31/n

Then we discuss the gritty realities of trading.

Even when we know we have a positive edge, our experience of trading is dominated by variance.

32/n

Even when we know we have a positive edge, our experience of trading is dominated by variance.

https://twitter.com/therobotjames/status/1373783753059831809?s=20

32/n

When we trade competitive market inefficiencies, we add the uncertainty of never really knowing if we have an edge.

We discuss how to deal with this uncertainty - most practically and emotionally.

33/n

We discuss how to deal with this uncertainty - most practically and emotionally.

https://twitter.com/therobotjames/status/1372412020230787074

33/n

Practically, you'll learn it is crucial to understand the effect you are harnessing.

You'll set up simple analytics to track the drivers of those effects. This helps you not to be dependent on noisy decaying P&L to know when to adapt or pull a strategy.

34/n

You'll set up simple analytics to track the drivers of those effects. This helps you not to be dependent on noisy decaying P&L to know when to adapt or pull a strategy.

34/n

Emotionally, you'll explore random data and simulations to start to "feel the randomness in your bones".

You don't want to be "Fooled by Randomness" into making rash decisions.

35/n

You don't want to be "Fooled by Randomness" into making rash decisions.

35/n

By this point, you should have:

1. a good understanding of what inefficiencies you can exploit look like

2. a good process for finding them and exploiting them

3. realistic expectations of the experience of trading a systematic strategy.

36/n

1. a good understanding of what inefficiencies you can exploit look like

2. a good process for finding them and exploiting them

3. realistic expectations of the experience of trading a systematic strategy.

36/n

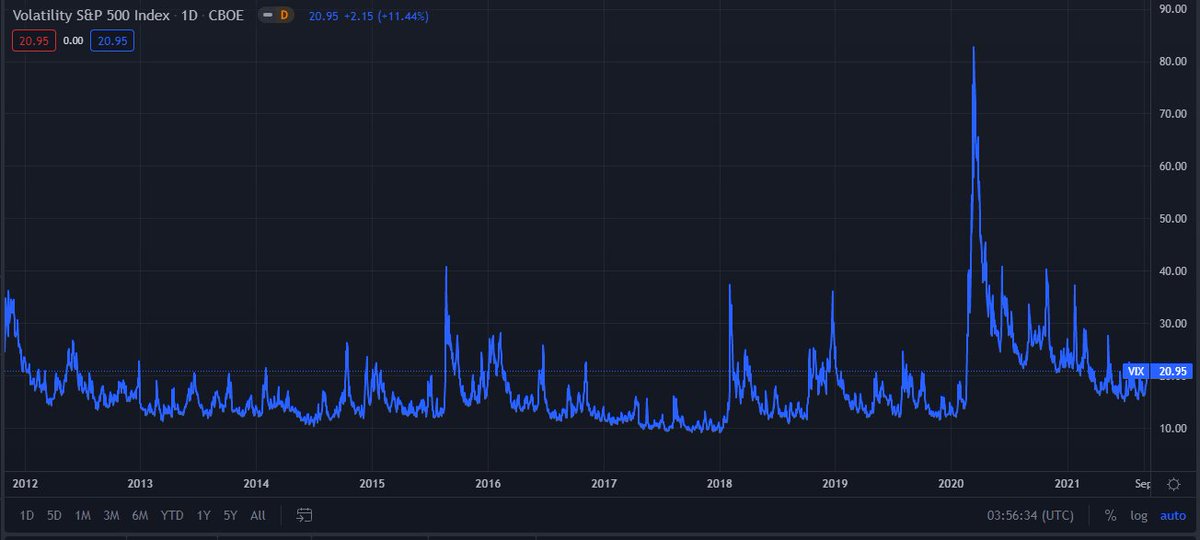

Next, we'll look at time-varying variance risk premia harvesting strategy, based on the concepts in this thread on VIX and VIX futures:

37/n

https://twitter.com/therobotjames/status/1437922467801034754?s=20

37/n

And we'll create a systematic VIX carry strategy, based on the concepts discussed here:

38/n

https://twitter.com/therobotjames/status/1439808225382047747?s=20

38/n

Now, with a bunch of different systematic strategies, what do you do?

You'll learn a sensible, quantitative approach to putting them together, including:

- a system for thinking about portfolio construction, both practically and emotionally

39/n

You'll learn a sensible, quantitative approach to putting them together, including:

- a system for thinking about portfolio construction, both practically and emotionally

39/n

- how to set portfolio management objectives

- how to set strategy-level volatility targets

- how to size strategies in a portfolio

- how to track and adjust strategy contributions

- what to do when things get weird

- how to chill out and "Trade More S**t"

40/n

- how to set strategy-level volatility targets

- how to size strategies in a portfolio

- how to track and adjust strategy contributions

- what to do when things get weird

- how to chill out and "Trade More S**t"

40/n

This time around, I've also added a new module on Cryptocurrency trading.

We look at the market and discuss the process for weighing up the decision on whether to enter a new market.

41/n

We look at the market and discuss the process for weighing up the decision on whether to enter a new market.

https://twitter.com/therobotjames/status/1389394682426236931?s=20

41/n

At any point, there are many other things you could be spending your time on.

And it’s important to choose activities that are expected to have a good payoff.

You must be especially aware of this when you are considering entering a new market.

42/n

And it’s important to choose activities that are expected to have a good payoff.

You must be especially aware of this when you are considering entering a new market.

42/n

We'll take you through the process we went through before deciding to enter the crypto market, building up a business case by:

- Finding out what other traders are doing

- Reading published research

- Doing simple quant analysis

- Doing some trading.

43/n

- Finding out what other traders are doing

- Reading published research

- Doing simple quant analysis

- Doing some trading.

43/n

And we'll outline some simple high-probability trading strategies harnessing basis and momentum effects.

All that in 5 weeks.

And most important of all, we'll leave you with the confidence that There Will Always Be More Trades.

robotwealth.com/trade-like-a-q…

44/44

All that in 5 weeks.

And most important of all, we'll leave you with the confidence that There Will Always Be More Trades.

robotwealth.com/trade-like-a-q…

44/44

• • •

Missing some Tweet in this thread? You can try to

force a refresh