China’s Evergrande debt crisis is the focus of the moment but property on China’s economy is the story. For the first time since the housing welfare system became a proper market, China’s property is facing up to a decade or more of stagnation. 1/7

First up demography. China’s cohort of first time prime age homebuyers, aged 25-39 is going fall by 25% by 2040, from 327m to 247m. So properly firms already overbuilding are in deep doodoo 2/7

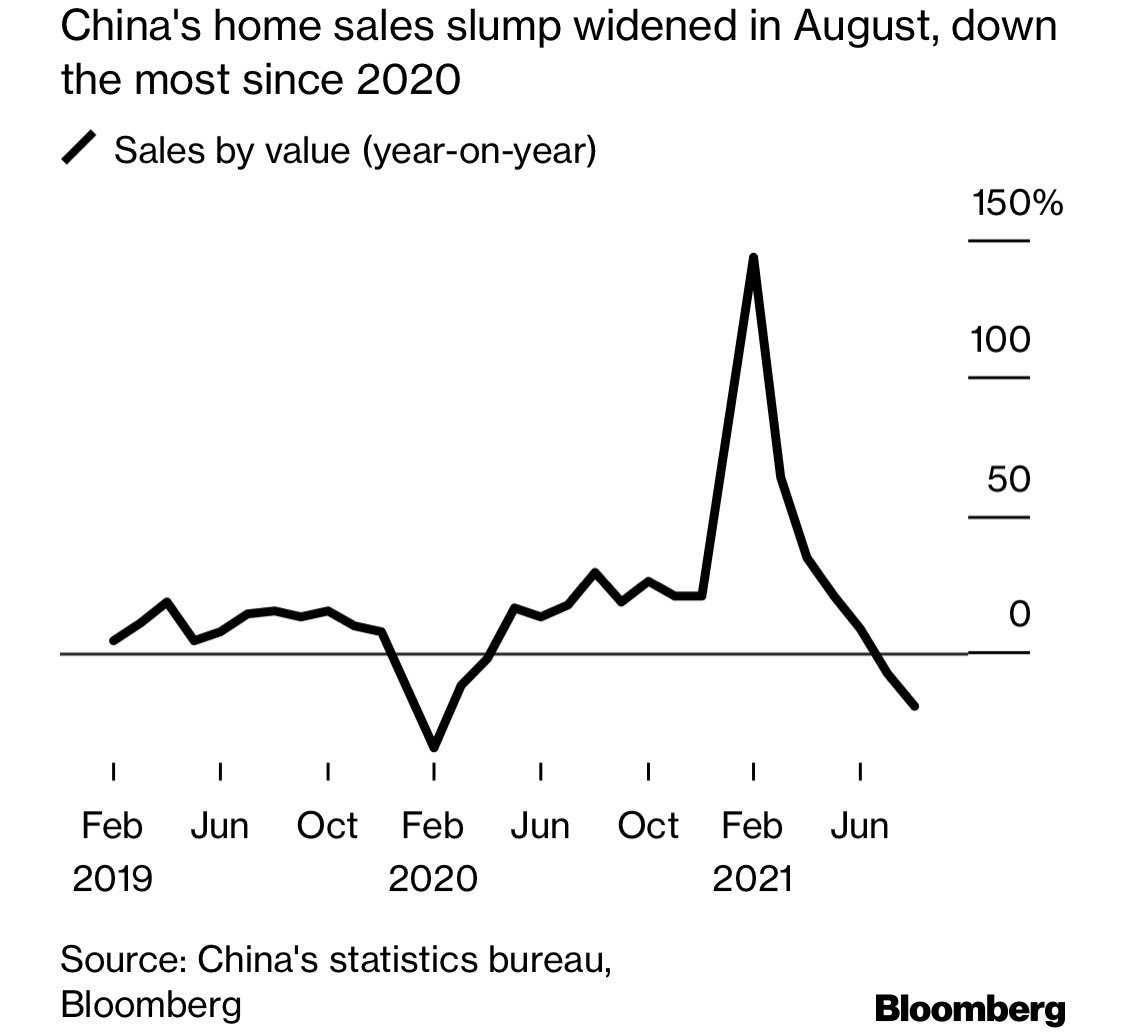

Next sales. These are now falling year on year by a lot. August/Sept together maybe down 30% year over year. And it could get worse as developers retrench, are forced to discount, manage too much inventory 3/7

Households are in no position to get more deeply involved if property transactions and wealth are on the turn. Household debt is now > $10 trn, having soared in recent years. Debt to disposable income is now 130% abd > USA. 4/7

Local government land sales are fine a third year over year and these guys will be hurting given the significance of revenues. How can they carry on building, borrowing, and providing for common prosperity? They can’t. 5/7

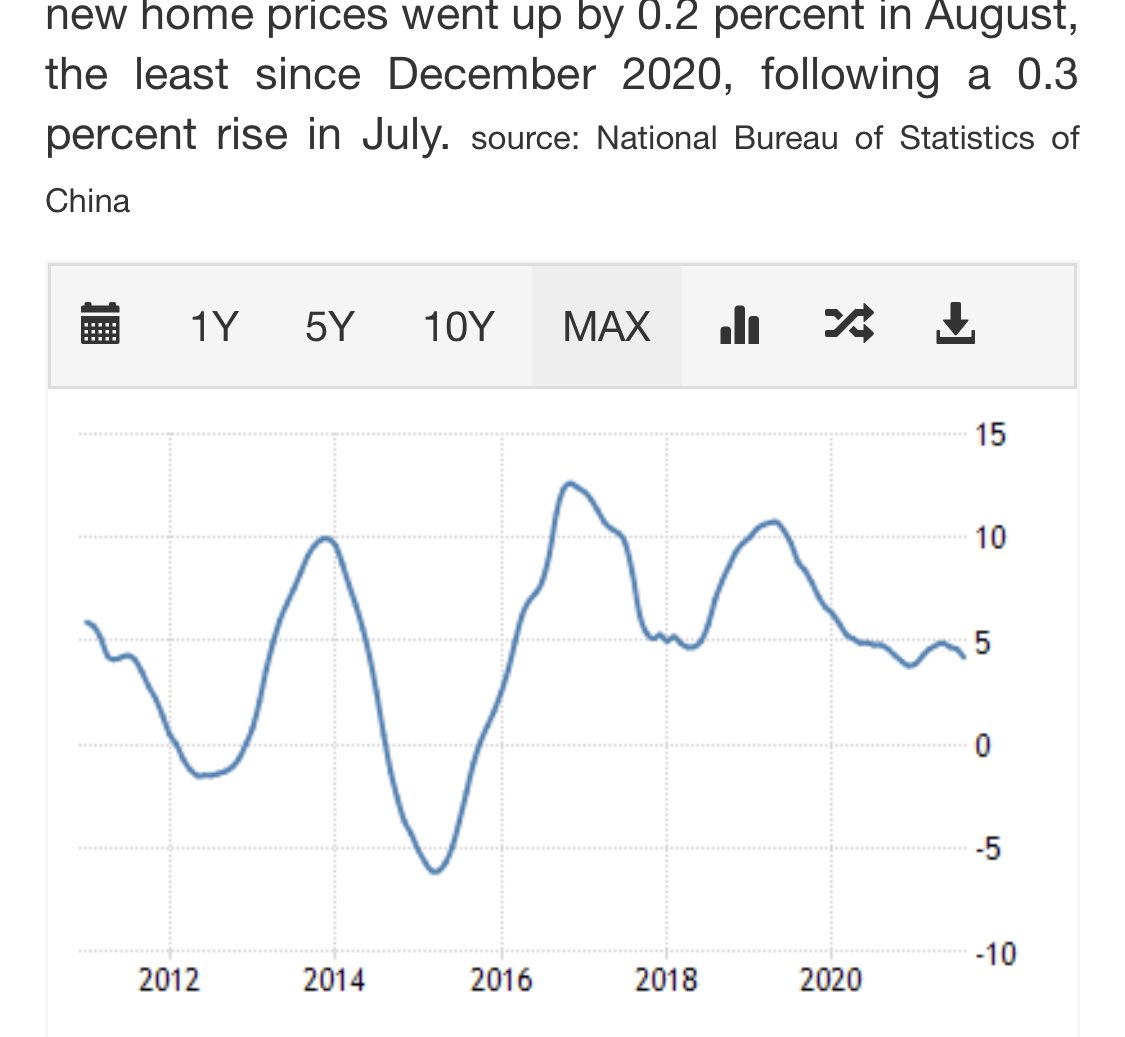

Finally prices. Hard to tell what’s going on but for 1st time, prices could fall over a protracted period. It’s tough to call the balance btw lower prices and lower volumes, but both are likely. 6/7

All in all, we need to brace for years of a more stagnant property market with unequivocally negative consequences for growth. Perhaps 2%, maybe even recession ‘with Chinese characteristics’. It’s a slippery path for China at home, and abroad. Ends

• • •

Missing some Tweet in this thread? You can try to

force a refresh