I dedicate this tweet to the Tesla haters who-- when confronted with the fact that U.S. legacy sales are in steady decline-- reply, "Sure, but you just don't get it, dummy: *their strategy* is to sell less vehicles!"

$GM $TSLA

investor.gm.com/static-files/c…

$GM $TSLA

investor.gm.com/static-files/c…

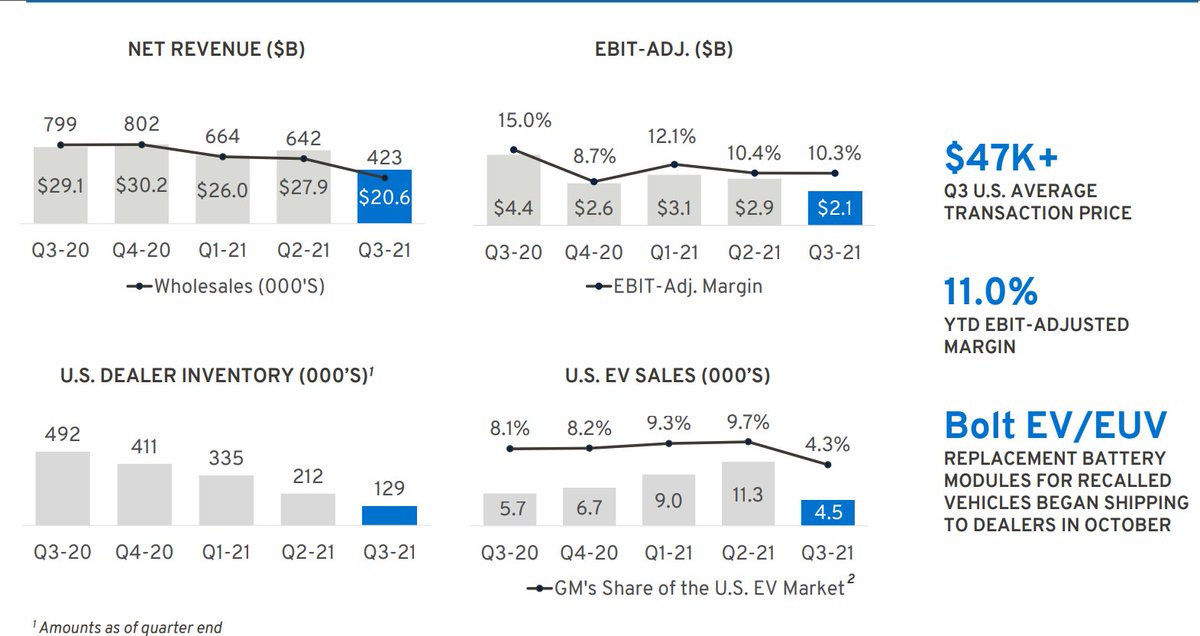

GM total revenue and EV market share have both fallen to their lowest level in 5 years:

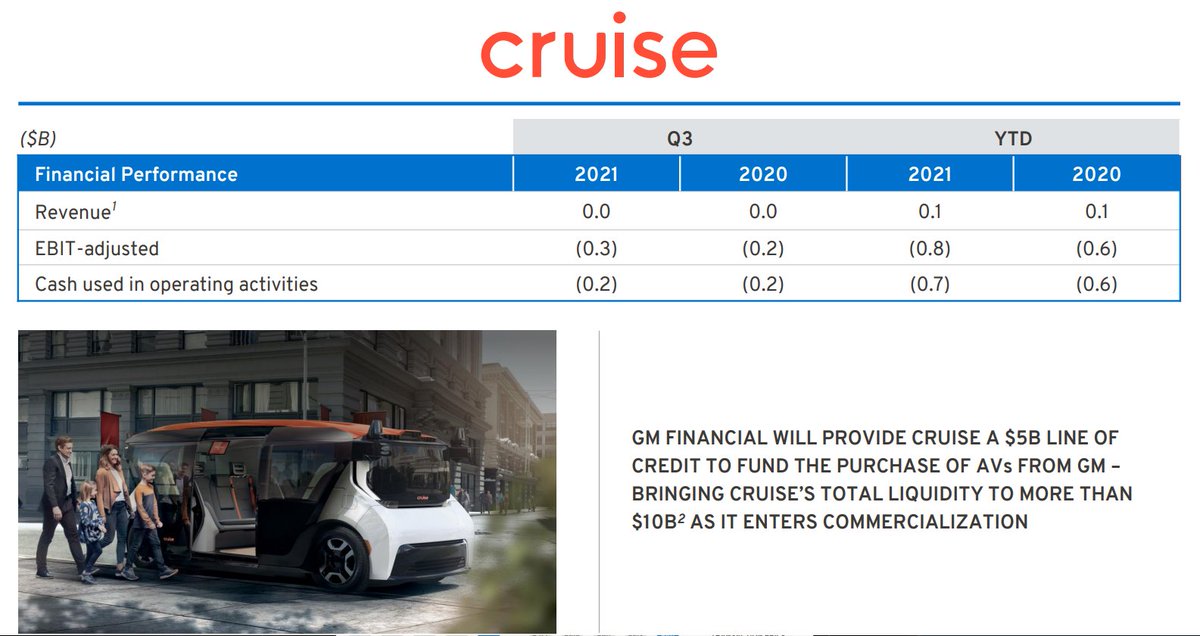

And Cruise is losing more money than ever and borrowing billions from GM Financial to purchase autonomous vehicles GM manufactures. 👀

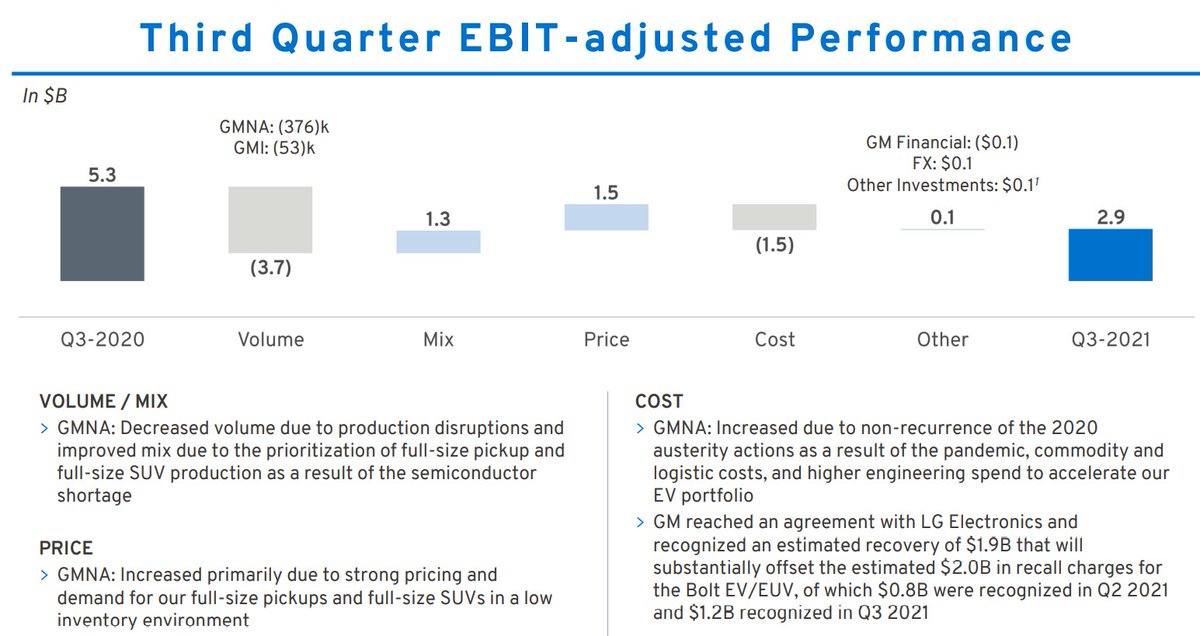

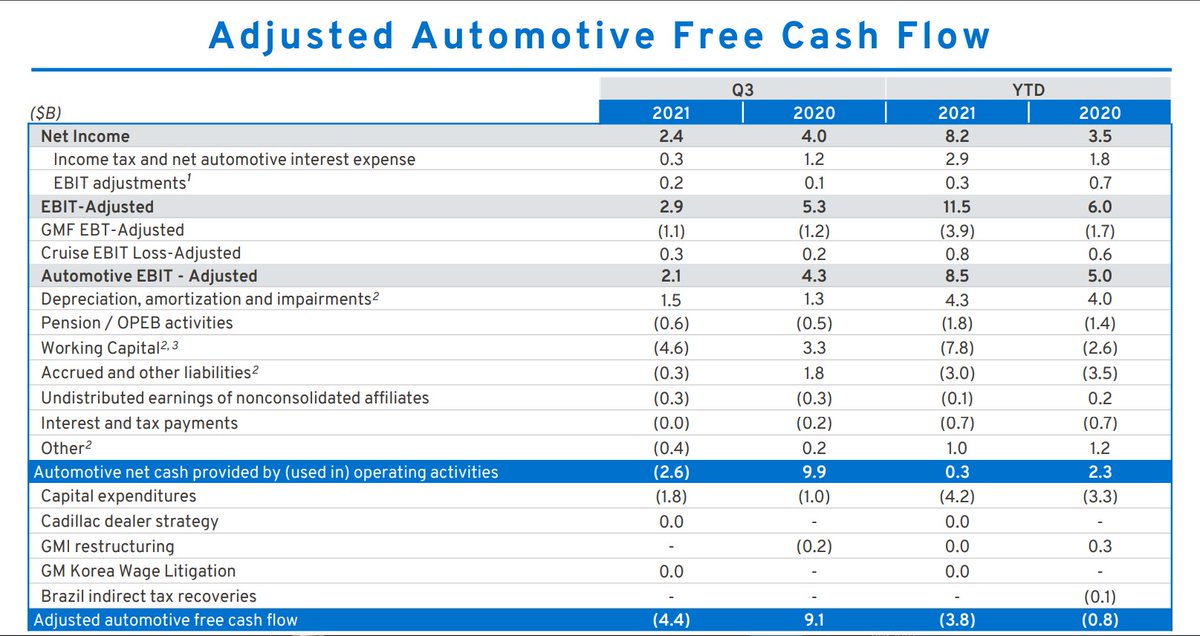

And GM's automotive free cash flow is negative again this year, so... 😬

Q3 2021 Earnings Comparison

$TSLA

$1.618B GAAP Earnings

241K deliveries

$ 6,703 GAAP Earnings per Delivery

$GM

$2.420B GAAP Earnings

1,311K deliveries (retail, excl. Joint Ventures)

$ 1,846 GAAP Earnings per Delivery

$TSLA

$1.618B GAAP Earnings

241K deliveries

$ 6,703 GAAP Earnings per Delivery

$GM

$2.420B GAAP Earnings

1,311K deliveries (retail, excl. Joint Ventures)

$ 1,846 GAAP Earnings per Delivery

I would edit the tweet above from “excl” to “incl”, if @Jack gave us an Edit button.

The units sold above *do* include Wuling Mini microcar sales in China.

If I exclude Wuling sales, it’s:

1,311K - 349K = 962K excl. Wuling

$2,420M / 962K = $2,516 per non-Wuling vehicle sold

The units sold above *do* include Wuling Mini microcar sales in China.

If I exclude Wuling sales, it’s:

1,311K - 349K = 962K excl. Wuling

$2,420M / 962K = $2,516 per non-Wuling vehicle sold

• • •

Missing some Tweet in this thread? You can try to

force a refresh