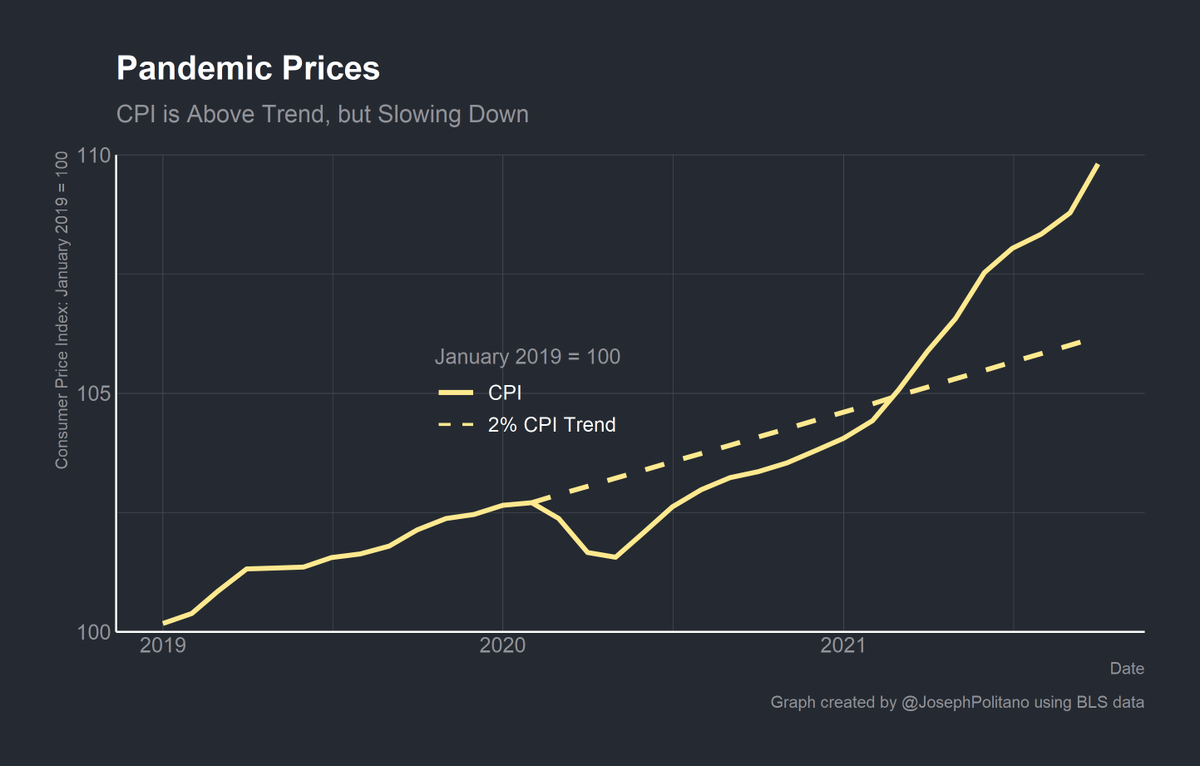

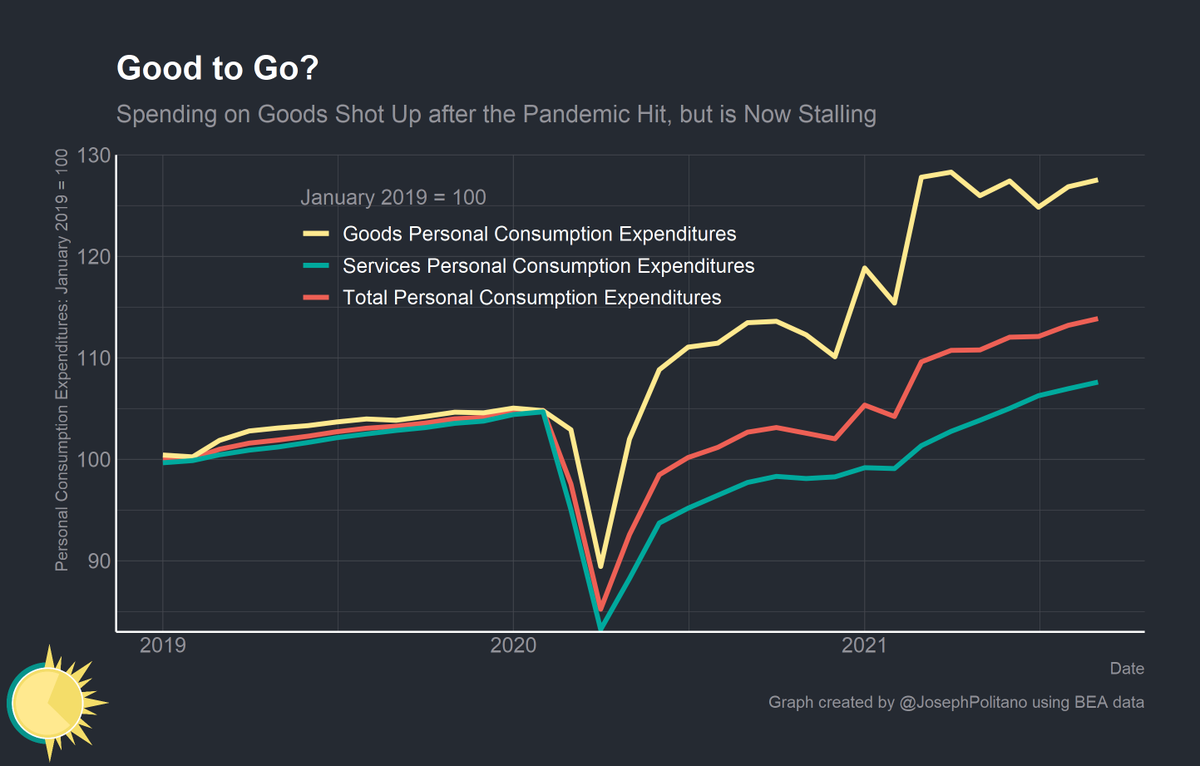

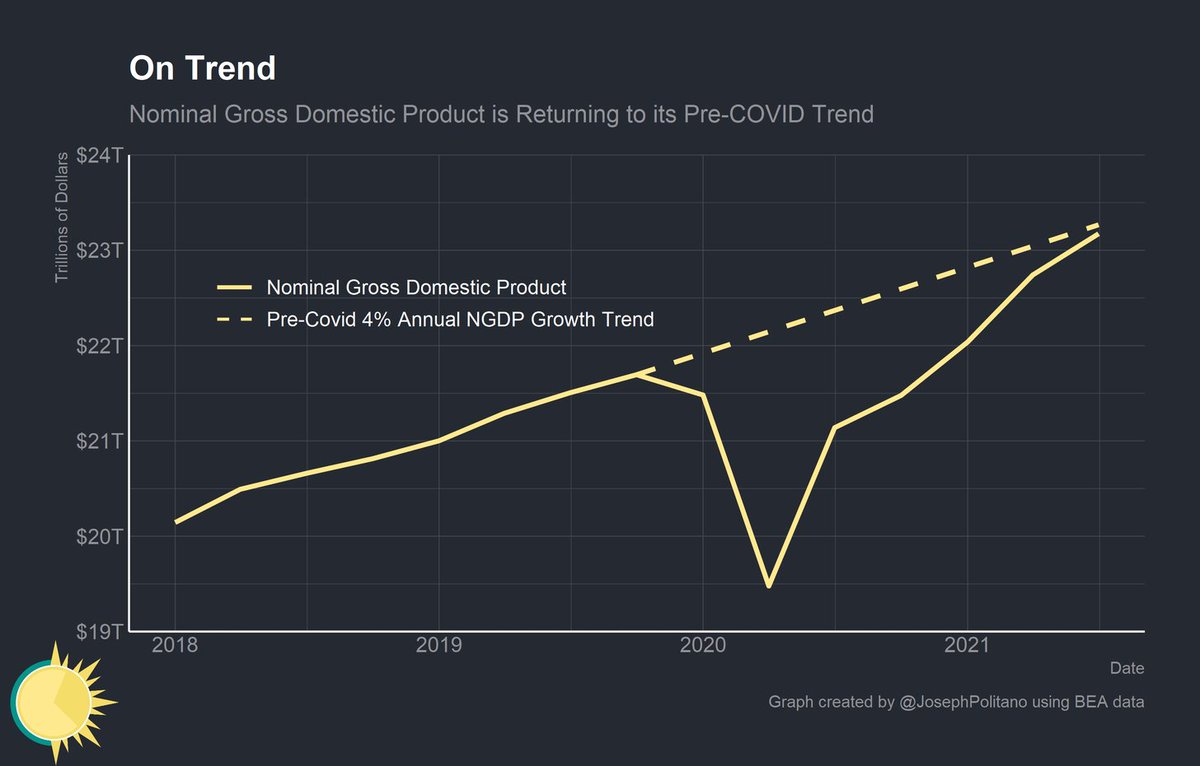

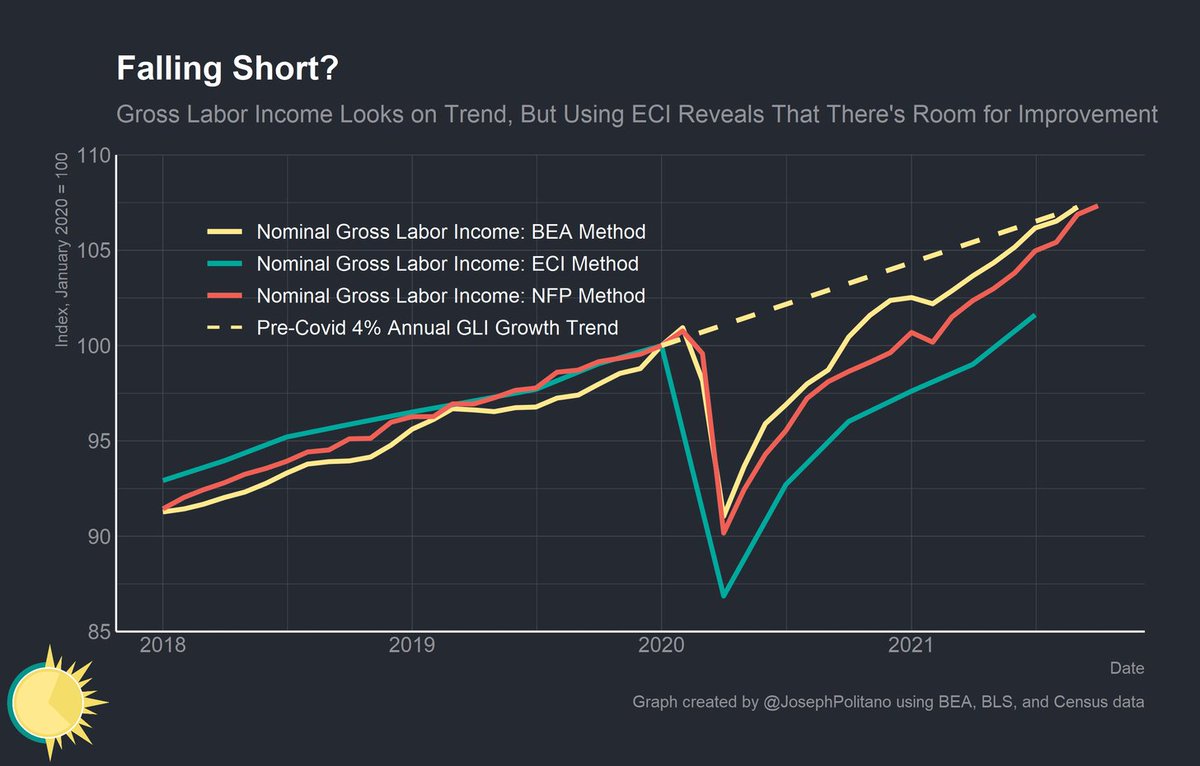

I really want to push back on both this construction of the market estimate of r* and its conclusions.

You can't use long term bond yields as evidence of the "natural rate of interest" as these yields are implicitly based on expectations of future short term policy rates.

You can't use long term bond yields as evidence of the "natural rate of interest" as these yields are implicitly based on expectations of future short term policy rates.

https://twitter.com/R_Perli/status/1457730333940633616

If long term bond yields partially reflect expected future short term rates, we would see expectations of excessively tight monetary policy reflected in this estimate of r*.

Indeed, that's what we saw during the 2013 taper tantrum and right now with Japanese Government Bonds.

Indeed, that's what we saw during the 2013 taper tantrum and right now with Japanese Government Bonds.

I'm not a big fan of r* conceptually, as I elaborate on here. Monetary policy is almost always a set of choices, and constructing a reliable measurement of "natural" interest rates is extremely hard.

apricitas.substack.com/p/the-fault-in…

apricitas.substack.com/p/the-fault-in…

If good r* estimates exist, however, they cannot be gleaned through looking at bond yield data. Long term interest rates are as much a function of Fed policy decisions as short term interest rates.

apricitas.substack.com/p/the-yield-cu…

apricitas.substack.com/p/the-yield-cu…

All this to say, if there is a gap between short term and long term interest rates it is not a measurement of how "off course" current Federal Reserve policy is, as some people in the comments suggested.

You should go follow @R_Perli now if you aren't already. I have learned a lot from him, and I know he already understands this stuff.

I just wanted to chime in with some context as the chart was causing confusion in the comments.

I just wanted to chime in with some context as the chart was causing confusion in the comments.

• • •

Missing some Tweet in this thread? You can try to

force a refresh