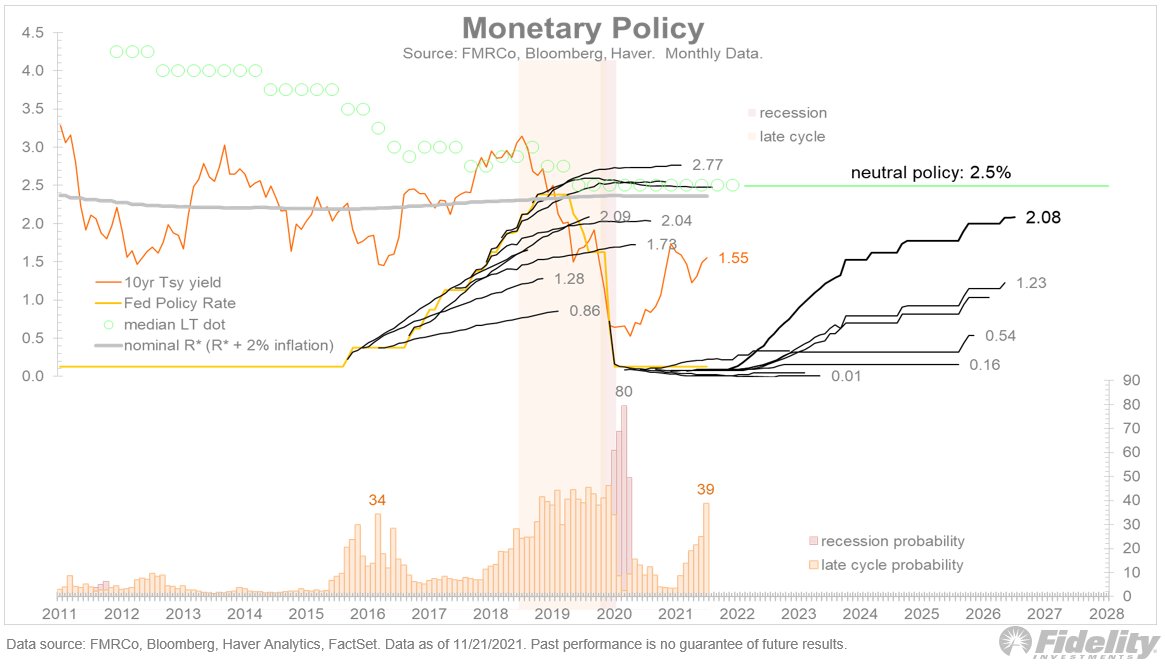

What would a persistently looser-than-neutral Fed policy mean for equities? With the exception of the 1970s, equities are an effective inflation hedge and should do OK. What about the big growers though? Take a look at this chart, and I'll explain. (THREAD)

As the chart above shows (h/t to Kevin Muir of The Macro Tourist), the relative performance of large growth to small value has a clear inverse correlation to long-term interest rates. /2

If you believe that the rates market is underestimating the degree of Fed tightening in the coming years (and that long rates will rise accordingly), then you should probably not own too many long duration large-cap growth stocks. /3

But if rates stay relatively low—at least compared to inflation—even the big growers (which have been leading the charge as of late) could hang in there. /END

• • •

Missing some Tweet in this thread? You can try to

force a refresh